“What is the best Delta to use when selling covered call options?” I get this question frequently from the educated core of members from our BCI community. Delta is one of the five option Greeks which are mathematical means of quantifying the risk inherent in our option positions. Delta is one of, what I consider, the “big 3”, with Vega and Theta being the other two. When responding to this question, I realized that my response was similar to a strategy I use when deciding when I should leave my house to get to the airport, a determination I have been making quite frequently as I have been speaking about option-selling almost every month in different cities throughout the US. First, I will provide the three definitions of Delta and then present my airport strategy.

Delta defined from three perspectives

- Delta is the amount an option price will change for every $1.00 change in share price.

- Delta is the equivalent number of shares represented by the options position.

- Delta is the percentage likelihood that, upon expiration, the option will expire in-the-money or (stated differently) with intrinsic value.

Many consider Delta the most significant of the option Greeks because option buyers depend on Delta to overcome the negative impact of Theta (time value erosion) in order to generate option profits. This would relate to the first of the three definitions. The second definition is important for those who are measuring overall portfolio risk as many wealth managers seek to approximate “Delta-neutral” portfolios. We, however, are option sellers so we consider the third definition which will determine the chance of exercise…the higher the Delta, the greater the chance of exercise unless we implement one of our exit strategies.

We also know that high-Delta options have an intrinsic value component as these strikes, by definition, are in-the-money. Intrinsic value offers greater protection to the downside but will eliminate the opportunity for additional profits from share appreciation as opposed to low-Delta options (out-of-the-money). These last two paragraphs represent the information we need to know and understand before making option decisions based on Delta. By now, you’re probably wondering what all this has to do with an “airport strategy”

Alan’s Airport Formula

This is all about working backwards, the same way we would determine option Delta decisions. When Linda and I are heading to the airport for a seminar in another city, we decide the night before when we should set our alarm clock. We start with our ultimate goal…be on the plane for an 11 AM takeoff, for example. Start with our end goal and then work backwards. Let’s see now:

- We like to get to the airport 2 hours before the flight leaves

- It takes 30 minutes to get from the airport parking lot to the terminal

- It takes 45 minutes to get to the airport parking lot

- We need one hour to shower and dress and load suit cases into our car

That’s 4 hours and 15 minutes which means we set the alarm clock at 6:45 AM for an 11 AM flight. That’s the best time to achieve our ultimate goal to be on the plane for an 11 AM takeoff. We worked backwards.

Practical application of selecting our option Delta using the “Airport Formula”

The key takeaway here is that our ultimate goal will vary based on several factors and so one particular Delta will not benefit us in all circumstances. Here are the factors to consider as they relate to Delta:

- What is our overall market assessment?

- What do the chart technicals tell us?

- What is our personal risk tolerance…high, low, somewhere in between?

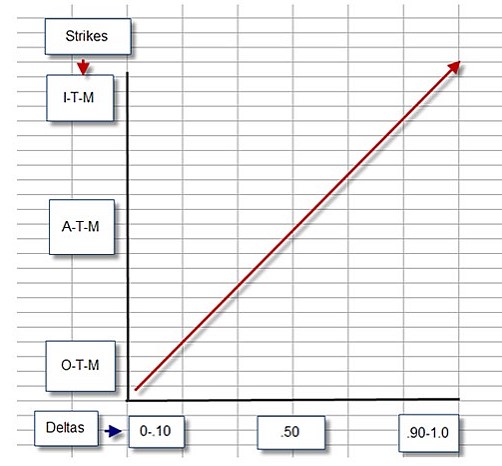

Once we have made these determinations we make a portfolio assessment ranging from bullish to neutral to bearish. The more bullish we are, the lower Deltas would prevail. The more bearish we are, the higher Deltas would be more appropriate. We do not start with a specific Delta, but rather work backwards to be sure we achieve our goal of getting on that plane on time or setting our portfolio up based on current information. Generally, we look to near-the-money strikes that meet our initial monthly goals (2-4% in my case) so Deltas would range from 40 – 60 as a guideline. If bullish, we would move the range lower and, if bearish, we would favor a higher range. The chart below highlights a graphic representation of Delta (not the airline!) as it relates to the moneyness of the strike:

Delta and the Moneyness of Strikes

Delta and the Moneyness of Strikes

Discussion

Next live events

- Dallas Texas: October 5, 2017

- Palm Beach Gardens Florida: October 10, 2017: Information to follow

Market tone

Global stocks declined this week as tensions between North Korea and the United States intensified. Oil prices decreased modestly, as West Texas Intermediate crude declined to $48.20 a barrel from $49 a week ago. Volatility, as measured by the Chicago Board Options Exchange Volatility Index (VIX), rose to 15.51 from 9.90 last Friday. This week’s economic and international news of importance:

- Donald Trump warned North Korea that its continued threats, if carried out, would be met with overwhelming force

- North Korea announced it was planning to target the waters surrounding the US territory of Guam with four missiles. Trump responded by noting US military plans are now “locked and loaded”

- Earlier this week intelligence assessments became public revealing that North Korea has likely acquired the technological capability to miniaturize a nuclear warhead, making it deliverable by missile

- Tensions have risen further in the wake of additional United Nations sanctions against North Korea that were unanimously agreed upon by the UN Security Council. The sanctions aim to cut North Korean exports by one-third and ban exports of coal, iron ore and seafood

- The Consumer Price Index rose just 0.1% in July after not rising at all in June, the fifth straight month of below-forecast inflation figures. Futures markets forecast just a 40% chance of another rate hike before the end of this year.

- The newly created Constituent Assembly this week declared itself supreme over all other branches of Venezuela’s government. A growing list of governments, including the US and the European Union have declared the assembly illegitimate

- Jacob Zuma, the embattled president of South Africa faced the fourth no-confidence motion of his presidency on Tuesday

- As of 9 August, 447 of S&P 500 Index companies have reported earnings for the second quarter. Earnings for the index are expected to rise 11.9% compared with the same quarter a year ago, and 9.2% when stripping out energy companies

- Revenues are seen up 5.1% versus Q2 2016, 4.1% ex-energy

For the week, the S&P 500 moved down by 1.43% for a year-to-date return of 9.05%

THE WEEK AHEAD

Mon, August 14th

- Japan: Q2 Gross domestic product

- China: Retail sales, industrial production

- Eurozone: Industrial production

Tue, August 15th

- United Kingdom: Consumer price index

- United States: Retail sales

Wed, August 16th

- Eurozone: Q2 Gross domestic product

- US Housing starts and building permits

Thu, August 17th

- UK: Retail sales

- Eurozone: CPI, trade, ECB minutes

- US Industrial production

- Canada: CPI

Summary

IBD: Uptrend under pressure

GMI: 3/6- Buy signal since market close of July 13, 2017

BCI: I am currently moving to a defensive posture as the September contracts approach, favoring in-the-money strikes 2-to-1. This position may change depending on the geo-political events that surface in the upcoming week.

WHAT THE BROAD MARKET INDICATORS (S&P 500 AND VIX) ARE TELLING US

The 6-month charts point to a mixed outlook. In the past six months, the S&P 500 was up 5% while the VIX (15.51) moved up by 40%.

Much success to all,

Alan and the BCI team

Alan,

perfect comparison and great humor.

The alarm clock (smartphone) makes you sleep well.

Working backwards, with the BCI methodolohy is easy :

A) Market assessment comes from you every week, and suits me well.

B) Chart technicals and fundamentals come from Barry’s Weekly Stock Screen for selecting the underlaying stocks.

C) My risk tollerance is obviously close to yours (2%-4%)

So, no need to worry about the Greeks (the EU shall rescue them)

Roni

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 08/11/17.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are in Earnings Season, be sure to read Alan’s article,

“Constructing Your Covered Call Portfolio During Earnings Season”. You can

access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Premium Members note, a new Blue Hour webinar has been uploaded to the Premium Member website..

Best,

Barry (barry@thebluecollarinvestor.com) and The BCI Team

Alan,

Thanks for another educational article. Between the other 2 of the “big 3” vega and theta, how to rank their significance to covered call writing?

Thanks,

Marsha

Marsha,

Understanding and integrating the concepts of the “Greeks” (not the EU version Roni!) are important. It is not necessary to look up the specific stats but rather to recognize how they impact our trading positions. Both Theta and Vega are important. From a capital preservation perspective, Vega will measure the risk in our positions as it relates to implied volatility. Theta will guide us in when to enter our positions and how and when to use our position management techniques. Maximizing and integrating our education in a time-efficient manner will elevate our success to the highest levels.

Alan

Marsha,

Delta is an estimate of the probability of the option expiring ITM and its value is affected by implied volatility which varies during the life of the option. It has some usefulness if you are using it to set up you CC based on probability of assignment. IMO, a CC is a basic transactional event where you try to find a premium that provides a balance between sufficient reward as well as adequate downside protection. Other than delta, IMO, the Greeks have little usefulness for a covered call position. How fast theta decay is or how much IV changes are just statistical calculations. The main concerns are covering the short call when it reaches a desired level of decay and defending the stock if it starts heading south. Don’t make things more complex than they need to be. The Greeks are for more complex positions.

Spin

Alan,

How true the airport analogy.. We have all been there. There are perils on the way though. you have to watch out for the bumps in the road as you try to get to the airport.

… Like forgetting to stay on time per your original schedule as you try to squeeze other things in at the last minute. That plane will take off on time, with or without you.

… Like not getting emotions get in the way of what you were planning and preventing you from getting there. You have made your decisions on what you going to do. Stick to it.

… Like adding new goals at the last minute (creeping intelligence) which will insure you never get there.

… And don’t forget to fill up your gas tank the day before – no time for that un-planned fill up. Do your research and planning beforehand so you can efficiently and successfully implement your goals.

Mario

A good Sunday evening all….

I did a fair amount of hobby market reading this weekend. I am not a huge Contrarian but I have a streak of it in me. So I like to see articles on mainstream financial sites taking a Chicken Little stance saying “the sky is falling” sell everything :).

I did not read much of that which suggests to me the selling is not over. Many Technicians point to oversold metrics and predict bounces this week. I hope they are right.

If so I will over write Index holdings ATM for Sept and buy ITM put spreads in energy, banks and bio for Sept expiry. I’m not covering my GLD or TLT. I’ll let them sink or swim without water wings for the new month :). – Jay

Hi Alan,

I have a question regarding premium of a covered call. Is there a good reason why we shouldn’t go for the highest premium (strike price very close to the current stock price)? I understand we would like to get the stock price appreciation when the price goes up but if we want to use those same stocks to write calls again we have to buy them back at the higher prices therefore we would not be gaining anything from the stock price appreciation. I probably missing something here.

Thanks for your time

Phil

Phil,

There are 2 perspectives here:

1- Looking for the highest premiums in general is a common mistake made by covered call writers. Stocks that generate the highest option premiums are securities with high implied volatility…market anticipation of large price swings in either direction. This means more risk for us. Since covered call writing is a conservative option strategy geared to investors who have cash-generation and capital preservation in mind, highest premium stocks are not appropriate as they accomplish only one of those goals.

2- Once we have decided on a stock, the at-the-money strike will generate the highest initial time-value premiums but allow us no upside potential from share appreciation or downside protection of the initial time value profit (there is always a breakeven for all strikes).

In bull markets and with stocks with strong chart technicals, it will benefit us in the long run to use out-of-the-money strikes where we have an opportunity to generate profit both from option premium and share appreciation to the strike.

In bear and volatile market environments, it will benefit us in the long run to use in-the-money strikes where the intrinsic value component of the option premium serves as additional downside protection where intrinsic value protects time value.

The flexibility of strike price selection will absolutely elevate our portfolio returns.

Alan

Alan,

Thank you so much for the quick reply. I’m very new to this so I’m a little behind on everything. Let’s use some actual numbers so I can get my point across.

I currently own some shares of EXAS. Current price is $38.66/share. For Sept 15th call, I can sell option at strike price of $39, $40, or $41. I used your awesome spreadsheet to put together a table for my evaluation.

My question is why should I not go for the 39 Strike and get a 5% ROO? I understand that if they stock price go up to let’s say $42/share I’ll miss out on the upside. If the price is $42 the buyer will exercise their option. Now I’m faced with 2 options, do I want to keep using EXAS for next month cover call or buy something else? If I want to stick with EXAS I have to buy them at $42/share so that means the realized upside is not there even if I were to sell the option at 41 Strike? The way I’m looking at this is if the stock is a great warrior that I want to use over and over I don’t see why we should not go for the strike with the highest premium.

Thanks for reading my question. Have a great day!

Phil

Phil,

Our covered call positions have 2 legs, the long stock and the short call. In neutral to bull market environments we have opportunities to generate cash from both legs. We must take advantage of these situations. For those who play blackjack, you know that if you stand with 11 and the dealer shows a 6, we must take advantage by doubling down.

In bull markets we must use out-of-the-money strikes to create the opportunities for 2 income streams in the same contract month with the same stock and investment.

I shaded in the far right column of your spreadsheet to highlight the upside potential we must take advantage of in certain market conditions. The potential can be quantified by adding the ROO column and the upside column.

The 5% return is fabulous but had we sold the $41 call in a bull market environment and share price moved up by $2.34 or more by expiration, our return would have been 8.6%, 72% higher.

We must take advantage of all situations that will enhance the level of our trading success.

Alan

Alan,

Regarding Phil and EXAS:

Please clarify, In a bull market, would you go for the higher risk 41 call? I can understand picking the $40 call (middle one) since the current price is already almost 3/4 up the 39-40 Strike. Is that being too greedy and possible increasing the risk unnecesarily.

Also, you did not mention it, but because the Gains are so high for this stock, isn’t the Volatility indicated possibly exclude this stock position if this stock was in your current run list?

I see Phil indicates that he currently owns the stock and is overwriting it. If his cost basis is low, the he probably can take the risk with selling an option no matter what the volatility or high Gain % noted.

Mario

Mario,

As always, you bring out several important points so let me explain my response.

EXAS is a stock that would not pass the rigorous BCI screens from a fundamental perspective. Technically it is strong but currently would not make our list.

That said, we are starting from the perspective that the stock is in our portfolio and now considering which strike to select. Phil’s question relates to why ever select an option with a lower initial return than the at-the-money strike. My response addressed that question in a general manner.

Regarding volatility: Appropriate implied volatility varies from investor-to-investor. For me, I look to options with initial returns for near-the-money 1-month returns of 2-4%…1-2% in my mother’s portfolio. For others, higher or lower may be appropriate.

The implied volatility for EXAS for these strikes is probably in the 40-50% range bringing it to the upper range for my personal risk-tolerance. Had I owned this stock, I would consider going with the deeper out-of-the-money strikes if the overall market was extremely bullish and chart technicals were bullish and confirming.

Let me re-state that this is not a stock I would hold in my portfolio at this time based on weak fundamentals. In general, deeper out-of-the-money strikes are considered in certain bull market environments.

Alan

Phil,

Investors seeking growth buy stocks and hold them for price appreciation. Investors seeking increased income sell covered calls. Strike price selection is based on your outlook for the stock as well as your risk tolerance and reward objective.

An out-of-the-money CC is bullish and offers higher potential reward but less risk protection.

An at-the-money CC is neutral to mildly bullish and offers a balance of both. .

An in-the-money CC is a defensive position that offers a lower potential reward but provides more risk protection.

IMO, if the stock powers up well beyond the strike price that you sold and is assigned, let it go and find another position that present a similar opportunity to make the maximum amount of profit. If the stock is near the strike price at expiration and you still feel that it has potential to generate income, roll the current short call out to next month for an additional credit. Use a combo spread order to maximize your credit.

Spin

Alan,

Aug was may first month trading a small cash account. I have 5 positions in a $20K account. As of this email, four out of five positions are ITM (BEAT @$34, TER @ $33, Team @ $35, and UCTT @ $22.50 only ENTG OTM). My plan is to rely on the BCI watch list for monthly stock selection. So analyzing exit strategies seems a little confusing, because none of these positions are on the current running list. My questions is: Do you consider roll out and or up on positions that are ITM but not on the watch list or recently removed? (I know I made a mistake with BEAT. It was not in the gold highlighted section so I did not realize it had earnings in the current month. I got lucky. It was hard to allocated with only $20k.)

Thank you,

Jesse

Jesse,

You will find that during week’s like last week, when the market was down significantly, many of the eligible stocks get bounced from our list for technical analysis reasons. Recovery from that perspective may be right around the corner…like today, for example.

The screenshot below shows the technicals that turned back positive today (red arrows). We have until Friday to decide whether to roll these options. If borderline, we can roll out to an in-the-money strike. If a more bullish picture develops, we can roll out and up. If the technical picture looks negative, allow assignment and move on to a stronger security.

It looks like you’re off to an excellent start.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG

Alan

Jesse,

An experiment I encourage you to try with a $20K account is put it all in QQQ in a paper account and over write one contract a month near the money covering about $14K of it. Let the rest run.

You may be surprised how much easier that is and how much better you do than trying to pick a handful of stocks each month that could run all over the yard. – Jay

Unwound my 3 positions in UCTT after the stock rose 5.12% today, 8/14/17.

Covered call sold on 7/31/17. Down to 20% Rule on 8/4 when I closed the option leg On Friday my position gain was -0.526%. 3:50pm Monday +4.26%. That’s good enough for me while I am ahead.

All other stocks in my portfolio were .mostly up 1-1.5%.

Mario

Mario

You bought UCTT at an earlier date then Mario? I recall UCTT was offering reasonable premium at the start of the contract period, but I didn’t like the fact that it had just bounded up from 19 to circa 25.

Still a good result.

Justin

Justin,

I opened the Covered call on UCTT on 7/31. The stock then proceeded to cave and finally recovered on Monday with a Gap Up.

Guess I made a good decision. UCTT finished down on Tuesday.

Regarding my portfolio and Expiration Friday coming up:

** Last Friday I had 12 positions OTM and 1 position close to strike Pin OTM.

** As of end of day Tuesday, I now have 8 positions ITM in 4 stocks (EDU, PYPL, QQQ) that need my attention on Friday if market continues positive.

The rest of the week will be interesting.

Mario

Mario,

Good luck with those – last night was a bit TOO interesting for my taste 🙂 My own little portfolio of cc’s was showing a maximum profit of 2.7% after two hours of trading on Thursday, but by the end it had fallen to 1.7% (calculations done using Total Paid – Premium rec’d.) A fall such as Thursday’s has invariably been followed by a snap-back the following day – hopefully recent history will repeat in Friday’s trading.

Justin

ALAN,

I am having a hard time analyzing the roll out or up on BEAT. I think it may be due to its quick run up in the share price has created such a wide spread between the bid/ask. Would you mind sharing how you would analyze this position?

BEAT purchased 100 shares for $33.63 sold Aug 34 @ $1.67. Current share price $36.60. Current Bid/Ask on the Aug 34 is $2.30/$3.70??? The roll out to Sept 34 Bid/Ask is $2.90/$3.70 with only 45 open Int. ??? Roll up to a Sept 37 Bid/Ask is a more normal $1.20/$1.55. What am I missing?

It appears to me that I should just let this trade expire because the buy back premium on the Aug 34 is out of whack. Is this right based on today’s market for BEAT? I know that it is a bit early to execute a roll out/up strategy. I am just trying to practice this move so I am better equipped for Thursday or Friday. Any help would be a great benefit for me.

Thank you,

Jesse

Jesse,

I agree that it’s too early to execute a rolling exit strategy but let’s assume that it’s Thursday or Friday with today’s stats. As of 12:25 PM on Tuesday, the spread for the 8/$34 call is $2.30 – $3.10; the spread for the 9/$34 call is $3 – $3.40 and the spread for the 9/$37 call is $1.30 – $1.55. Let’s use the following stats to enter into the “What Now” tab of the Ellman Calculator:

8/$34: BTC at $2.90

9/$34: STO at $3.10

9/37: STO at $1.40

The screenshot of the spreadsheet below shows the following:

Rolling out produces a 1-month return of 0.59% (yellow) with 7.2% downside protection of that profit.

Rolling out and up produces a 1-month return of 3.38% and 4.41% (brown rows) with upside if share price moves up to the now out-of-the-money strike.

If today was Friday, we have 3 choices: allow assignment, roll out and roll out-and-up. For me, I would eliminate rolling out because it doesn’t meet my time value return goals (2-4%) and consider the first and third choices. Let’s see how things play out by Thursday or Friday.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG

Alan

Alan and Jesse,

*** You are doing pretty good with your BEAT trade even before Friday’s Expiration Date. You have 6.07% Gain (4.97% (1.67 STO / 33.63 PurPrice) and 1.1% (34/33.63) upside to 34 Strike). 33.63 is your OTM cost basis of the original sale. Breakeven point is 31.96 (33.63 PurPrice – 1.67 STO)

*** Interesting that when you use 2.90 for Closing the 34 Strike option, the Intrinsic value is 2.60 (33.60 Last price – 34) and Time Value is 0.30 (2.90 – 2.60). The represents a loss of 0.9% (0.3 / 33.63 Cost Basis) or net gain of 5.17% in your present position if you unwind your trade now. So waiting to late Friday to take action on this trade is wise to take advantage of the lower time decay value. You will easily pick up 0.5% or more in Gain.

*** As Alan analyzed, the Roll Out Up to 37 gives you a Gain of 3.38% plus an additional 1.1 upside for a total of 4.4%. The Breakeven point is 33.46 (33.63-1.67+2.9-1.40).

*** Another option for Expiration Friday is to Roll up to 36 instead of 37, which give you downside protection and lowers your Breakeven point further compared to the 37 Strike case.

The Sept 36 Call is today 8/15 is 1.70/2.10 Bid Ask. Assuming a fill at 1.90 then using 34 as you basis for comparison, the Roll up to 36 numbers are: -1.9 (BTC at 34) + 2.0 (Share Appreciation 36-34) + 1.90 (STO at 36) = 1.0.

Gain for roll up to 36 is 2.9% (1.0 / 34) . Downside Protection for roll up is 1.6% (36.60 Last Price / 36 Strike). BreakEven point is 32.96 (33.63-1.67+2.90-1.9). This BEP point is another 0.5 lower than the 37 Strike case.

*** Using the Ellman Elite Calculator to verify the above results, I entered the following to Roll Up and Out to an ITM 36 strike:

BEAT:

8/18 Aug BTC Strike 34 2.90 (No change)

9/15 Sep STO Strike 34 3.10 (No change)

9/15 Sep STO Strike 36 1.90 (New Strike)

The results (see attached image) show the 2.9% gain for both columns, with and without upside potential, verifying the Elite Calculator can handle this special case of a Roll up to an ITM strike.

So your choices are (using for all cases Last Price 36.60 and Cost Basis 36.63):

A. Unwind today: 5.17% gain (lose 0.9%, lose stock)

B. Let Call be assigned on Friday: 6.07% (lose stock)

C. Roll Out to 34: 6.66%, (Adds 0.59%,Downside 7.1%) BEP 31.76

D. Roll Out Up to 36: 9.04% (Adds 2.97%, Downside 1.6%) BEP 32.96

E. Roll Out Up to 37: Gain 9.34% (Adds 3.26%), plus upside Potential of 1.1% for Net Total Gain 10.44%, BEP 33.46

On the safe side, I like the 9.64% for (D). (D) and (E) both have great Breakeven points.

Good luck!

Mario G.

I am doing quite well with my CC trading, however I am still struggling in my decision making process when it comes to stocks that have declined beyond what I received in option premium, and the option expired worthless.

I could roll down, but that would mean locking in a loss. I could sell the stock – if it no longer meets the BCI criteria – but I would take a loss. I could hold the stock and see if it comes up a bit, or are there times when one will just have a percentage of losing trades in one’s portfolio and we need to move on?

Andrew,

We all hate taking a loss but that’s part of trading. If we hold 20 positions in a month and 12 are winners and 4 are losers and 4 are breakevens while mitigating losses and enhancing gains with our exit strategy arsenal…we’ve had a heck of a month.

Re-read the exit strategy chapters of my books or watch the DVDs and study the examples as when best to roll down or look to “hit a double” or sell the stock.

Not all positions will be winners but in normal market conditions most will be.

Glad to hear of your recent success.

Keep up the good work.

Alan

Premium members:

This week’s 8-page report of top-performing ETFs and analysis of ALL Select Sector Components has been uploaded to your premium site.

Also, check out our new ETF VIDEO USER GUIDE recently published on your member site.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

TAL EDUCATION (TAL) Stock split:

On 8/16, TAL split 6-for-1. This means for every 1 share owned, we now own 6 shares (100 = 600 shares). Share price is cut to 1/6 of its previous value so its really just an accounting procedure allowing retail investors the opportunity to purchase shares at a lower price in 100 share increments. This will effect the strike prices of our short calls. Here is a link describing those changes:

file:///C:/Users/alan/Downloads/41633.pdf

Thanks to Kevin for bringing this to our attention.

Alan