After executing our covered call writing trades, we immediately prepare for position management opportunities…exit strategies. One of these strategies in our arsenal is the Mid Contract Unwind exit strategy. This is used when share value appreciates dramatically resulting in a time value cost-to-close of near zero. In other words, the option originally sold will be trading near parity (intrinsic value only). Having maxed the original trade, closing at a cost of near zero will allow us to use the cash from the sale of the stock to generate a second income stream in the same contract month with a covered call position using a different underlying security. The better our timing with these exit strategies the greater our level of success.

Real life example: Harley Davidson Inc. (HOG)

On July 1, 2016, HOG rallied nearly $9.00 per share on reports of a potential buyout. Here is a look at the gap-up in price that day:

HOG Gap-UP on July 1, 2016

With the stock now trading at $54.25, the $45.00 call option was deep in-the-money and trading near parity. The cost to close at this time was $9.50 which consisted of $9.25 of intrinsic value and $0.25 of time value. The practical cost-to-close is $25.00 per contract plus small trading commissions. We get to this $25.00 figure by deducting the increase in share value buying back the option produces. Prior to closing the short option position, our shares can be worth no more than $45.00 per share, our contract obligation. After buying back the option our shares are now worth market value or $54.25. It we can then take the cash generated by selling the stock to generate a second income stream in the same month with the same cash we have made greater than a maximum profit for the month.

Why act immediately when the opportunity arises?

There are two reasons why we should react reasonably quickly when these opportunities arise:

1- Share price can decline resulting in a higher cost-to-close.

2- Theta is reducing the time values of the second option positions as expiration approaches.

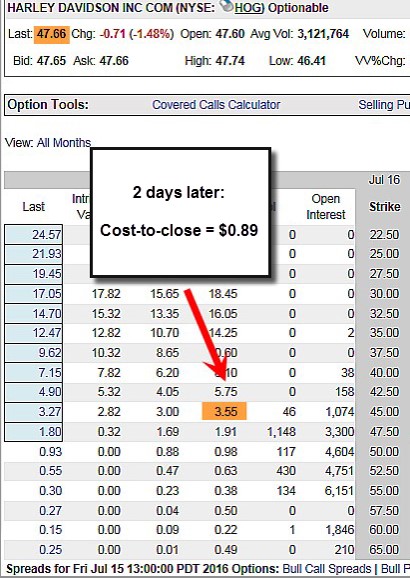

Two days later

HOG experienced some negative news about the buyout resulting in several analyst downgrades causing share value to decline from $54.00 to $47.66. With the $45.00 not nearly as deep in the money at this point in time, the time value cost to close moved up to $0.89 ($3.55 – $2.66), more than triple the amount had we acted sooner:

Options Chain for HOG After Price Decline

The time value cost-to-close is now $0.89 ($3.55 – $2.66) about 3 1/2 times more than it was two days prior to the price decline. We also find ourselves with two days less time value to generate with our second income-generating position as Theta is eroding option premiums.

Discussion

There is more to position management than executing these exit strategies. The timing of the management trades plays a vital role in our success as well as the time value of our option premiums can change as a result of Delta (change in share price) and Theta (passing of calendar days) as demonstrated in this real-life example.

Blue Hour webinars

1- The recording of Blue Hour webinar #3 discussing long-term investing is now available to all active premium members on the member site (left side, scroll down under 10% discount link). The first 2 Blue Hour webinars are also available in that same area.

2- Blue Hour webinar #4 is one you don’t want to miss. I will discuss the “Poor Man’s Covered Call”, a topic many of you have been inquiring about. The strategy uses LEAPS options instead of actual stocks as the underlying security. There will be a lot of new information presented found nowhere else. Look for the event date to be in late January or early February.

Blue Hour Webinars on the Member Site

Upcoming live events

1- February 27, 2017

Marriott Marquis Hotel, NYC

1:30 PM ET

Exhibit hall Booth 208 (February 26th – 28th) … come say hi to the BCI team

2- March 21st and 22nd, 2017

Two live Florida events (Fort Lauderdale and Delray Beach)

Information to follow

Market tone

Global stocks edged up slightly after the Federal Open Market Committee’s decision this week to raise the key federal funds target rate by 25 basis points to a range of 0.50% to 0.75%. While the move was expected, markets needed to also digest the FOMC’s statement that it would target three rate hikes in 2017, which was more than expected. The 10-year US Treasury bond yield continued to climb upwards after the FOMC announcement, reaching as high as 2.58% this week, its highest level since September 2014. This week’s reports and international news of importance:

- This week’s FOMC decision to raise the federal funds rate by 25 basis points comes one year after its last hike

- This week’s hike came amid increasing enthusiasm in equity markets, as investors continued to move from defensive positions into riskier segments of the market

- Equity market volatility is much lower and credit and liquidity conditions are also stronger now versus a year ago

- President-elect Donald Trump this week announced his intention to nominate Exxon Mobil chief executive Rex W. Tillerson as secretary of state. The choice of Tillerson’s was criticized by senators on both sides of the aisle, who object his business dealings with Russia and its president, Vladimir Putin

- Trump also announced that former Texas governor Rick Perry is his choice for energy secretary

- The US dollar continued to strengthen this week versus most major currencies

- The Japanese yen has declined 11% since the US presidential election, while the Mexican peso has fallen 10%. China’s yuan has also weakened

- Japan surpassed China as the largest holder of US government bonds this week. China’s government has been selling foreign currency reserves in an effort to protect the yuan

- The US NFIB small-business optimism index rose by 3.5 points in November to 98.4, beating consensus estimates and rising above its 42-year average

THE WEEK AHEAD

- Eurozone wage figures are released on Monday, December 19th

- Japanese trade data and unemployment figures are released on Monday, December 19th

- The Bank of Japan meets to decide monetary policy on Tuesday, December 20th

- Eurozone consumer confidence figures are released on Wednesday, December 21st

- The United States announces estimates for Q3 GDP on Thursday, December 22nd

THE WEEK AHEAD

For the week, the S&P 500 declined by 0.07% for a year-to-date return of +10.47%.

Summary

IBD: Market in confirmed uptrend

GMI: 6/6- Buy signal since market close of November 10, 2016

BCI: I am currently fully invested and have an equal number of in-the-money and out-of-the-money strikes. Love the market direction but still feel that a cautious approach is justified.

WHAT THE BROAD MARKET INDICATORS (S&P 500 AND VIX) ARE TELLING US

The 6-month charts point to a bullish outlook. In the past six months, the S&P 500 was up 9% while the VIX (12.20) declined by 36%.

_____________________________________________________

Wishing you the best in investing and a wonderful holiday season,

Alan (alan@thebluecollarinvestor.com) and the BCI team

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 12/16/16.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Some of our subscribers have asked if we could increase the size of the font. Since we have designed the original report to get the most out of the standard “portrait” mode, we couldn’t increase the font size. Instead we have we have added two additional sections to the report this week. We have copied the first two sections…Market Overview and Weekly Stock Screen…presented them in “landscape’ mode and increased the page size by 125%.

Best,

Barry and The Blue Collar Investor Team

Hey Barry,

Since we are always asking you for the next enhancement I guess I will throw my request on the pile :)!

Since I write mostly monthly covered calls and cash secured puts I was wondering how much trouble it would be to run the Blue Chip report monthly instead of quarterly?

I realize those stocks do not move as much, which makes them great candidates for our strategies, but running it the weekend after regular monthly expiry – like today as an example – might keep it more fresh and timely for those of us who use it.

Thanks, for any consideration. – Jay

Hi Jay,

Good suggestion.

Half of my positions were called away yesterday :-), and I’m 50% in cash.

Now I must plan my next trades for the Jan 20 contracts.

We have an extra week this time, which I like, but I am kind of worried because last yearend plus Jan 2016 correction set me back almost 40%.

Alan is bullish but cautious, and I will follow his lead.

Oil is up, Russia is taking care of Siria, the election is over, the market seems to like Trump’s plans, and the Fed watch is over.

But…..

Please tell me what you think about the next 5 weeks.

Cheers – Roni

Hey Roni,

I am bullish about the next 5 weeks.

I am watching like a hawk for down days to buy things. Then after they run up a few days i sell covered calls on an up tick for loss protection.

I do not support Trump. I question everything from his capacity to his competence. But he won and the market loves it. So I must respect and listen to that.

Be long through the weeks ahead. – Jay

Thanks Jay, will do.

Roni

Jay and Roni,

I have asked my team to produce and upload the 1st quarter, 2017 Blue Chip Report a week earlier than originally scheduled. Look for the report to be available on the member site (“resources/downloads” section) today or tomorrow. I will discuss with my team over the holidays and New Years the possibility of adding additional Blue Chip Reports as part of the current premium member benefits program.

Thanks for the suggestion.

Alan

Alan,

Thank you for your always prompt reply and feedback. I thought you and Barry adding the Blue Chip report was a great idea.

Those stocks are a nice medium ground between the often higher volatility trending stocks on the main list and the ETF’s. – Jay

Thank you Alan,

your hard work is highly appreciated.

Roni

In the example, would you have tried to get a cheaper price than 3.55 to buy back the option? What price would you ask for?

Thanks,

Danny

Danny,

Absolutely. I showed the published “ask” or worst case scenario. In this case, the spread is $0.55 ($3.00 – $3.55) with 1074 contracts of open interest so (if I were closing) I would definitely leverage the “Show or Fill Rule” to generate a lower cost-to-close price. The midpoint of the spread is $3.275 so I would place a limit order to buy-to-close at $3.30 – $3.35. $20/contract is better in our pockets than those of the market-makers!

For more detailed information on how to negotiate better prices with the market-makers see pages:

1- 225 – 227 of the Complete Encyclopedia…Classic version

2- 122 – 124 of the Complete Encyclopedia Volume 2.

Alan

Alan,

Covered calls are not in my arsenal at this time but always wondered about them. I mainly swing trade and sell cash secured puts. I’ve had some success, and since i do

better selling the puts i’m thinking of using more of that strategy going forward. Got to thinking why not adding covered calls along with selling the puts, which brings me to you.

Few questions please-

How many etf’s do you list monthly ?

There is a service out there that uses a strategy of buying stock, then buying an in the money put for protection, going out min. 90 days, usually more. They then use other strategy’s to bring in income to try and eventually have a risk free trade on. Natch if position rises handsomely in price one could garner all the upside, seems nice in a bull mkt. They also profess that that strategy is better than selling covered calls. Could you comment on their thoughts please.

That’s it for now, thanks for listening.

Enjoy the holiday’s,

Thanks

Mike

Mike,

My responses:

1- Our ETF Reports generally have between 20 – 25 eligible candidates. In an extreme bear market environment it could go as low as 15 but that is quite rare.

2- A- There is no such thing as a risk-free trade unless you are buying Treasuries etc….beware.

B- The strategy entails buying protective puts which generally are out-of-the-money. In-the-money protective puts are more likely to get exercised and cost more. They may be appropriate in strong bull markets but then there is less of a need for downside protection.

C- “Other strategies” to bring in income sounds like selling covered calls. This is known as the “collar strategy” which does cap the upside.

D- “Better” than covered call writing is too vague to comment on. There are so many strategies we can benefit from and the most appropriate for us depends on our goals, personal risk tolerance and trading style. I have been using covered call writing as my main strategy in the stock portion of my portfolio for decades. For me, it is the best income-producing strategy by far. It may not be the best strategy for an investor with a different trading style and different goals.

E- If you have interest in this proposed strategy, you can “paper-trade” with a hypothetical account for a few months and then you will have clarity on the pros and cons and this investment approach.

Alan

MY FRIEND THAT I TAUGHT HOW TO SELL OPTIONS AND WATCH YOUR VIDEOS HAS MADE $20,000 IN THE LAST 3 MONTHS ON $80,OOO INVESTMENT.

IN THE PROCESS OF TEACHING HIM, MY WIFE LISTENED AND PICKED UP SOME OF THE LINGO AND NOW IS ON MY BACK ABOUT TRYING TO DO COLLAR PLAYS FOR OPTIONS.

I DON’T WANT TO BUY ANYTHING AND I AM HAPPY SELLING CALLS AND PUTS. AS I UNDERSTAND IT THIS IS A PLAY TO PROTECT THE DOWNSIDE OF A LONG POSITION.

IS THIS A PLAY IN OPTIONS WHEN YOU DON’T OWN A LONG POSITION TO PLAY A SPREAD TO MAKE MONEY?

SEEMS RISKY TO ME IF YOU GUESS THE WRONG BRACKET FOR YOUR SPREAD. YES, NO, COMPLICATED?

IF YOU DON’T HAVE TIME TO ANSWER THIS COULD YOU DIRECT ME TO AN ANSWER SO I CAN CONVINCE HER TO STOP NAGGING ME ABOUT SOMETHING THAT IS MORE DANGEROUS THEN WHAT I AM DOING WITH MY LIMITED FUNDS OF $6500.

THANKS,

MARK

Mark,

There is a strategy related to covered call writing that meets the criteria your wife is interested in. It is called the “Poor

Man’s Covered Call” or “long call diagonal debit spread”. Instead of buying the underlying stock or ETF, a LEAPS (long-term) option is purchased and then short-term call options are sold against this long position. Here is a link to an article I published on this topic:

https://www.thebluecollarinvestor.com/poor-mans-covered-call-practical-application/

I will be hosting a webinar on the PMCC in late January/early February and also publishing an E-Book on the topic.

There are pros and cons to this type of trading but my personal preference still resides with traddional covered call writing and selling cash-secured puts.

Alan

Alan,

I read an option article that said we should only sell options because time decay results in 90% of all options expiring worthless. Is this the reason you like covered call writing or put selling?

Thanks,

Rose

Hi Rose,

I am one of the regulars here. Welcome to our group!

Alan answers everyone’s questions. But since he is the proprietor and walks a tight rope about giving advice I would like to share my thoughts regarding your question subject to his correction.

Speaking only for me I sell options for portfolio protection and monthly income. The percentage of options that expire worthless is interesting but not important, in my opinion, since they are trading instruments few hold for term unless you sell them to waste away as I do.

If you are new to selling options you have found the right place to learn among friends! – Jay

Rose,

Like Jay, I sell options to generate monthly cash flow. Most members of the BCI community are conservative investors with capital preservation a key priority. By selling options, we are lowering our cost basis and improving the chances of a successful investment.

Option buyers have the opportunity for greater upside but do have Theta (time value erosion) working against them. They are “swimming against the current” Personal risk tolerance and strategy goals play a major role on which side of the trade we land.

You mentioned a myth that has been “out there” for decades…90% of options expire worthless. This is not true. What is true is that about 10% of options are exercised. According to the Chicago Board Options Exchange, 55-60% of options are closed and 30-35% of options actually expire worthless. Welcome to our BCI community.

Alan

PREMIUM MEMBERS: NEW BLUE CHIP REPORT

The 1st quarter, 2017 Blue Chip report has been uploaded to your member site on the right side in the “resources/downloads” section as shown in the screenshot below which shows the top part of the member site.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG

Alan

Thanks Alan, if we ever again get that seemingly extinct event formerly known as a correction these will be good stocks to sell OTM cash secured puts on at support :)! – Jay

Site Maintenance tomorrow:

We will be switching over to a larger server to accommodate our growing membership tomorrow and don’t anticipate a significant disruption of service. However, if you come to the site and it isn’t active, expect service to resume shortly thereafter.

Thanks,

Alan

Alan,

Would you mind please detailing the math on how you calculated a practical cost to close of $25.00 per contract? Thanks.

Richie,

When the trade was initially structured, the $45.00 call was sold which means that we have a contract obligation to sell at $45.00. Our shares cannot be worth more than $45.00 as long as the short call is in place. When we buy back the option for $9.50, our shares our now worth market value or $54.25, a credit of $9.25. Of the $9.50 we pay to close, only $0.25 ($25.00 per contract) is time value or the practical cost-to-close.

Alan

Thanks Alan.