Covered call writers, historically, have ignored exit strategies as part of their investment approach. Certainly, not in the BCI community but most everywhere else. As we become aware of the major financial benefits of mastering the position management skill, we must be mindful of the possibility of over-management. Eating a slice of pizza is enjoyable, eating a whole pie can be painful. In this column we will evaluate the frequency with which we should roll down when one of our securities is declining in value. My thanks to Alan P., one of our premium members, for inspiring this article.

Alan’s trade

- 8/16/2016: Buy NVDA at $63.18

- 8/16/2016: Sell the 9/9/2016 $62.50 call at $2.00, a 2.1% initial return with 1.1% of downside protection of that option profit

NVDA Calculations for Initial Returns using The Ellman Calculator

- 8/17/2016: Market downturn and NVDA trading at $61.15 (near breakeven)

- 8/17/2016: Option premium at $1.08, 54% of original sale price and not close to our 20% guideline

For a free copy of the Basic Ellman Calculator click here.

We’re at breakeven…why not roll down every time we reach breakeven?

On initial glance, it may appear too good to be true that every time we reach breakeven, we can roll down and generate option credits and continue to pile up premium profits. Intuitively, we all know that nothing is too good to be true when it comes to investing in the long-term and that there are no free lunches. If there were, I’d want to meet the folks who are constantly taking the other side of our 100% winning trades and thank them…they don’t exist except maybe in the fantasy world of those 3 AM infomercials (don’t get me started!). Our initial takeaway is that we know rolling down will allow us to generate option credits and that this is an invaluable exit strategy in our arsenal.

BCI guidelines for rolling down: 20%/10% guidelines

- We buy back the option in the first half of the contract when option value reaches 20% or less of the original premium generated and 10% or less in the latter part of a contract

- Rolling down is generally reserved for the latter half of a contract

Disadvantages of constant rolling down when breakeven is reached

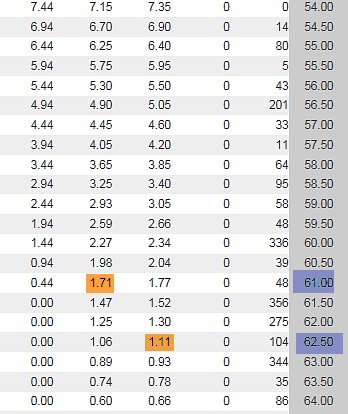

This is where understanding the trade execution process and the option Greeks (factors that influence option premium) will put cash into our pockets. Let’s have a look at the options chain on 8/17/2016 when option value is at 54%, NOT 20%, and the initial trade is near breakeven ($61.15):

NVDA-Options Chain for Rolling Down

The option chain clearly shows the advantage of rolling down from the $62.50 strike to the $61.00 strike, an option credit of $0.60 ($1.71 – $1.11) representing an additional 1%, 3-week return. Now, let’s dig a little deeper using our knowledge of trade executions and the option Greeks to identify the risks in rolling down in these scenarios.

Paying the difference in the bid-ask spread multiple times

We always buy at the ask (higher price) and sell at the bid (lower price). The difference is pocketed by the market-makers and paid for by us. We must temper and be selective as to how frequently and when we pay the spread to these market-makers.

Multiple commissions add up

We should be using online discount brokers to minimize trading commissions but we certainly should not be that kind to our brokers to initiate trades that do not benefit us.

***Locking in greater stock loss every time we roll down

Selling the original call meant that the shares could be worth no more than $62.50 during the contract. By rolling down, shares can be worth no more than $61.00. We cannot ignore the stock side of our trades. If share price rises, we will have to pay for share appreciation in the form of option intrinsic value to capture that rebound. Had we not rolled down, that recovery would be realized.

Theta effect

Every time we roll down and contract time passes, Theta is eroding option premium time value thereby decreasing opportunities to mitigate losses. This is why I generally reserve rolling down to the latter part of a contract.

Discussion

Rolling down is a key exit strategy in our arsenal but, like all strategies, it has its pros and cons. No free lunches and nothing is too good to be true….it wouldn’t be fair to those on the other side of our trades. But we can certainly be better and smarter than most! Understanding the positives and negatives will guide us to a management approach that will allow us to maximize our investment returns.

For more detailed information on rolling down:

Complete Encyclopedia for Covered Call Writing-Classic: Pages 256 – 259

Complete Encyclopedia for Covered Call Writing- Volume 2: Pages 253 – 254 and 304 – 307

New file in premium member area

“Strike Price Selection Guidelines” has been uploaded to the “resource/downloads” section (right side) of your member site. This will assist our members in determining which strike price to select based on market assessment, chart technicals and personal risk tolerance.

Upcoming live events

1- February 27 and 28th, 2017

Marriott Marquis Hotel, NYC

1:30 PM ET (Monday)

1:45 ET (Tuesday)

Exhibit Hall Booth 208 (February 26th – 28th) … come say hi to the BCI team

2- March 21st and 22nd, 2017

Two live Florida events (Fort Lauderdale -22nd and Delray Beach- 21st)

3- April 12, 2017

Income Generation Webinar for The Options Industry Council

![]()

4- JUST ADDED

AAII National Investor Conference

American Association of Individual Investors

November 3rd – November 5th, 2017

Market tone

Global stocks ticked up this week supported by continued improvement in manufacturing and solid US employment figures. West Texas Intermediate crude rose to $54.10 per barrel from $53.10 on increased tensions between the United States and Iran following an Iranian missile test. Volatility, as measured by the Chicago Board Options Exchange Volatility Index (VIX), rose to 10.97 from 10.8 last week. This week’s reports and international news of importance:

- The January employment report showed a 227,000 rise in payrolls

- This was muted by a downward revision from 204,000 to 164,000 in November

- Wages rose only 2.5% year over year in January, compared with 2.9% in December

- The unemployment rate ticked up to 4.8% in January from 4.7% in December, though the labor participation rate rose to 62.9% from 62.7% a month

- The United Kingdom’s parliament voted overwhelmingly in favor of advancing a bill to begin the Brexit negotiation process. Prime Minister Theresa May has set a 31 March deadline for invoking Article 50

- While the US Federal Reserve left monetary policy unchanged at its first meeting of 2017, the Federal Open Market Committee noted improved measures of consumer and business confidence of late. The market has been reducing rate hike expectations in recent weeks. Just less than two 25-basis-point hikes are expected in 2017, down from expectations of three shortly after the Fed raised rates in December

- President Donald Trump scolded major trading partners for manipulating their currencies. China, Japan and Germany were all named, resulting in currency market volatility

- Based on preliminary Q4 gross domestic product figures, the eurozone grew 1.7% in 2016, compared with 1.6% for the US. That’s the first time the eurozone has grown faster than the US since 2008. Eurozone joblessness fell to a seven-year low in 2016, while consumer prices rose 1.8% versus a year ago, reflecting rebounding oil prices

- Purchasing managers’ indices showed continued improvement in global manufacturing. The United States, the United Kingdom, Japan, China and the eurozone all reported solid manufacturing sentiment in January, though service-sector sentiment slowed mildly

- President Trump is expected to sign an executive order on Friday that establishes a framework for scaling back the Dodd-Frank financial reform law enacted in the wake of the global financial crisis

THE WEEK AHEAD

MONDAY, February 6th

- None scheduled

TUESDAY, February 7th

- Foreign trade deficit Dec

- Consumer credit

WEDNESDAY, FEB. 8th

- None scheduled

THURSDAY, FEB. 9th

- Weekly jobless claims

- Wholesale inventories

FRIDAY, FEB. 10th

- Consumer sentiment index

- Federal budget

For the week, the S&P 500 was up by 0.12% for a year-to-date return of 2.61%.

Summary

IBD: Market in confirmed uptrend

GMI: 6/6- Buy signal since market close of November 10, 2016

BCI: I am currently fully invested and have an equal number of in-the-money and out-of-the-money strikes. Despite all the bullish signals, I have a neutral to slightly bearish overall market assessment due to concerns about the new administration’s economic policies and their potential negative impact on our stock market. Although more clarity is needed, I choose to take a defensive posture at this point in time.

WHAT THE BROAD MARKET INDICATORS (S&P 500 AND VIX) ARE TELLING US

The 6-month charts point to a neutral to slightly bullish outlook. In the past six months, the S&P 500 was up 6% while the VIX (10.97) declined by 15%.

_____________________________________________________

Wishing you the best in investing,

Alan (alan@thebluecollarinvestor.com) and the BCI team

Alan;

I’ve never understood how BUYING TO CLOSE a CC works.

I sold a CC to open one DIS.

When time comes to exit this position and I buy to close it, or roll the CC, since I do not have a CUSIP number as when buying bonds, how does the market know it is buying to close MY DIS covered call?

If there are 1000 or more calls active, is the transaction tied to my name or my Scottrade account?

Thanks for the enlightenment.

Jim

Jim,

When we sell a covered call option, we do not sell it to a specific person but rather it goes into a pool of options bought and sold. The “Options Clearing Corporation” (OCC) matches up buyers and sellers. When we buy-to-close, the same procedure is in order and our new sell order is matched up with a new buyer. Check out this article I published in 2014:

https://www.thebluecollarinvestor.com/options-clearing-corporation-guaranteeing-our-options-trades/

Alan

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 02/03/17.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are in Earnings Season, be sure to read Alan’s article,

“Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The BCI Team

Alan;

I’m watching my DIS call daily and documenting it on paper as mid contract is coming up on 2/6.

Is there a BEST time of day to look at the activity?

My gut feeling says after the market closes.

Should my position go crazy one way or the other during the trading day – are you able to set up some type of alert to warn you?

Thanks

Jim

Jim,

After entering a trade, we can set up an immediate buy-to-close at 20% and change to 10% mid-contract. Example: STO at $2…then set up a BTC at $0.40 and change to $0.20 mid-contract. This way it’s automatic. I initiate my trades between 11AM and 3 PM ET to avoid early and late computerized trading. These are also the best times to check our positions. AMC is a good second check.

Alan

Alan,

I have been watching your videos and checking out your website, I really appreciate the honest manner you present information. I am considering a premium membership as I’m new to CC writing. I understand the 3 important keys to finding good trades and being successful are 1. Stock selection 2. Strike selection 3. Position/trade management. I am considering starting out with the poor mans covered call first to get my feet wet. I would appreciate any feedback/insight you could provide on my potential trade idea outlined below. I am not looking for trade recommendation rather to see if my analysis is correct.

Thank-you in advance for your time and consideration to respond. Tony

Requirements

Cost/Proceeds $990.00

Option Requirement $0.00

Total Requirements $990.00

Estimated Commission $6.00

Entered Trade

Symbol Price Cost

Buy 2 VOD Jan19 20 Call $5.30 $1,060.00

Sell -2 VOD MarWk2 25.5 Call $0.35 ($70.00)

Greeks / NBBO

Symbol Bid Ask IV Delta Gamma Vega Theta

VOD Jan19

20 Call 5.10 5.35 42.73 129.65 6.04 21.35 -0.69

VOD MarWk2

25.5 Call 0.29 0.36 28.00 -54.37 -32.68 -4.81 2.08

Net 75.28 -26.64 16.54 1.39

NBBO 4.74 5.06

Tony,

Before I respond, let me respectfully offer that there are many moving parts to this strategy that must be considered before risking our hard-earned money. It’s so much more than simply replacing a stock with LEAPS. Let’s assume all aspects of the strategy have been mastered….

Yes, this is a trade that meets are initial structuring formula requirements:

(Difference between strikes + initial short call premium) > Cost of LEAP

In this case:

[($25.50 – $20.00) + $0.35] > $5.30

$5.85 > $5.30

Assuming all 3 skill set requirements have been mastered, this is a trade that meets our initial structuring requirements.

Alan

RF has a premium of .76 for the $14 call is now $14.69. There are 12 days left for Feb. options. Due to there being only $7 of time value shouldn’t I roll out for more premium? I originally made $76, $44 time value.

Thanks,

Nehemiah

Nehemiah,

This is a mid-contract unwind opportunity rather than a rolling opportunity. This scenario fits our requirement for the time value cost to close to approach “0”. It is currently 0.5% ($0.07/$14.00). If we can generate more than 1 1/2% prior to contract expiration, I would consider the MCU strategy. See the exit strategy chapters in both versions of the “Complete Encyclopedia” for details on how to generate a 2nd income stream in the same month with the same cash using this strategy.

Alan

Subject: Adding 3% guideline for Calls

Alan,

Ref1: CSPuts book Page 137 (3% guideline below strike price sold)) (Underlying price under-performing the market – close position by buying back)

Ref2: Classic Encyclopedia Page 252 2nd (A) and 3rd (B) paragraphs) – (A) Week4 -Feel necessity to sell the underlying stock – buy back; (B) Any Time of cycle – If any time during the cycle feel stock is in danger or dropping dramatically, buy back and sell the stock

.*****

Paralleling the CSPuts threshold, why not add a 3% below the strike mathematical threshold as well to the Call guidelines to trigger a review. I know the 20%-10% premium rules are there to consider a possible Hit double situation or a review of the stock tone and technicals at that time but the stock could also dropping dramatically in value as well. I know in Week 4 of 4 week contract you ignore the 10% rule. So an overall guideline might be helpful as well.

Just thinking about Delta parallels, on an $100 stock with a 3% ROO, 3% is $3. Assuming delta is around 0.5 or thereabouts, the $3 drop in price of the underlying would only represent a 1.5 drop in Premium so the 20% rule would not be crossed.

Regards,

Mario G.

Mario,

The first action I took when I read your question was to print it and mark it for a future blog article or Ask Alan video. Excellent question.

The reason I did not include a similar 3% guideline for calls has to do with the nature of strike selection for each strategy. For calls, we already own the stock and ITM, ATM and OTM strikes are in play based on system criteria. For put-selling when using the BCI methodology we are using predominantly OTM puts and prefer not to take possession of the underlyings except when we sell puts in lieu of setting limit orders.

This means that the 3% guideline may be useful when selling ITM calls but usually not applicable when selling OTM calls. As an example, let’s use ANET currently trading about $95.00 (close to your $100.00 example). Let’s say we sold an OTM $100.00 call for $2.40 to generate an initial return of 2.5% (See image below). Now this is a trade that many BCIers would consider. However, if there was a 3% guideline in place, we would never enter the trade because the share price is already more than 3% below the call strike.

When setting guidelines I try to use statistics that have near universal application.

Thanks for an excellent question.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Alan

Alan;

Several of your lessons mention earning income twice in one month on the same stock. I’m not able to put my finger on a video that specifically applies to my CC option.

I wrote a on DIS at $113 strike (and mistake time! is coming with Earnings announced in 2 hours!) With a 113 strike, I’m not truly sweating bullets, but it does enforce your EARNINGS REPORTING philosophy! The predictions are for a negative reporting today.

When my BTC price is within the 20%/10% price range, it looks like I could roll out and up to a 3/17/17 expire date with a $115 call and maintain the 1/2% monthly profit you like when Portfolio Overwriting. (Basic calculator shows a .6% ROO)

Am I thinking through this move correctly?

Thanks, and I promise to listen closer…

Jim

Jim,

There are two different issues to address (you already addressed the earnings report rule…good for you to recognize the risk).

1- 2 incomes in 1-month…here’s a link to an article I published in 2012:

https://www.thebluecollarinvestor.com/hitting-a-double-a-bullish-early-contract-exit-strategy/

There is a lot more detailed information on this topic in the exit strategy chapters of both versions of the “Complete Encyclopedia”

2- Since it appears that DIS will open on Wednesday well below the $113 strike, there is no need to roll out and up. Check to see if the 10% guideline is met and, if so, closing the short call is the favored action in the BCI methodology.

Alan

Alan,

Thanks you for the Blue Hour on Poor Man’s Covered Calls. I missed it live but it is great you have it on our Premium page for anytime view. It caused a number of light bubs to click on for me.

As you know I have been around options trading for a while. But I never studied or considered LEAPS. Now I know enough to wet my appetite!

I do not know the product well enough to buy it until I see it in action. So tomorrow I am going to “buy” a $100K LEAP replacement portfolio in my paper account with 5 positions: 40% SPY, 30% QQQ and 10% each in IWM, TLT and GLD.

I will “buy” the Jan 2019 calls as close to 1.00 Delta as I can so that the LEAP portfolio mirrors the price movement of the ETF. I will “control” far more shares than I would if I put the same $100K to work in the same % on the same 5 buying them outright. Trade off being I have no equity, only an option.

I am not going to over write the paper portfolio yet. I know how that works. I just want to see it’s volatility versus the market and what draw downs look like on bad days or during pullbacks – assuming we have some in this up trending market :)!

Thanks again for sparking several ideas on possible uses for LEAPS. – Jay

Jay,

Please share with our BCI community the results of your paper-trading experiences.

I know this will be interesting and a valuable learning experience for many of us in the BCI community.

Alan

Thanks Alan, will do.

My virtual account attached to my Options House IRA account is not as sophisticated as I thought it was. It does not process orders in the same way the real account does.

So after some huff and fuss I just bought some SPY LEAPS at the market at the $120 strike which is the highest of the 1.00 delta strikes. I would never pay market with real money. I always split the bid ask with the broker. So I will factor that in as I watch the position. I control just over twice the number of shares I would have had I bought them out right. Intuitively I am expecting leveraged % results in both directions.

We shall see….- Jay

Running list stocks in the news: MKSI

MKS Instruments, a semiconductor manufacturer, recently beat consensus estimates by $0.05 per share. It was the 16th consecutive “earnings beat”…very impressive. As a result estimates have been rising as has the stock price.

Our Premium Stock report shows MKSI in the “Chips” industry which has a ranking of “A”, a Scouter Rating of “7”, a beta of 1.45, a % dividend yield of 1.00, the next projected earnings report date of 5/4/17, adequate open interest for near-the-money strikes, no Weeklys available and the last ex-date was 11/23/16. The stock has been on our premium member watch list for the past 5 weeks.

The blue arrows in the screenshot below, point out the bullish technical indicators in the current price chart.

Have a look to see if this equity deserves a spot in your portfolio.

CLICK ON IMAGE TO ENLARGE & USE BACK ARROW TO RETURN TO BLOG.

Alan

Alan,

What is the best way to handle this.

I own two positions in THO (200 shares, 100 shares) . Both with Strikes at 100.

Earning Report 3/6 – So I can’t use it for next cycle.

Last Price is 108.64. Deep In the Money

Last Premium Option price 6.19.

Last Option Trade: 6.19 Bid / Ask 6.3 – 9.0

Intrinsic 8.64.

Last Option trade 6.19.

Intrinsic 8.64, Time Value = Premium – Intrinsic = 6.19-8.64 = -2.45 or essentially 0 since it cannot be negative.

I can use the Invested money in a new position since in the middle of Week 3 of 4. I can either possibly Sell Covered call options for the remaining portion of this cycle for the next cycle Expiration Friday 3/17.

Position 1 has a Gain of $617.00 ROO% 3.1% (200 Sh)

Position 2 has a Gain of $265.00 ROO% 2.65% (100 Sh)

I think I can afford to give the Money Maker ($0.09 / contract) to unwind the position.

I placed two Buy-Write Sell orders (executes BTC and Sell of shares in one step) for credit limit price or 99.01 and am waiting to see if it is filled. Still waiting.

If it does not fill, I will just accept assignment in 10 days on 2/17/17 Expiration Friday, (ER 3/6/17)

My strategy correct? Should I consider reducing further my credit limit?

Regards,

Mario G.

Mario,

I cannot give specific financial advice in this venue but I’m happy to share with you my thinking in similar scenarios:

You have maximized your trade profit and have a significant amount of downside protection to protect that profit. Congratulations for that.

When a decision comes down to closing and re-investing the capital for the remainder of the current contract or allowing assignment we calculate the time value cost-to-close. For premium members who have access to the Elite version of the Ellman Calculator, the “Unwind Now” tab can be used for this calculation. If the cost-to-close is such that we can generate a return of at least 1% greater than to actual cost to close, it is worth closing. Some investors may set a higher or lower parameter but that is mine. For example, if the cost to close is 0.5% and we can generate a 1.5% initial profit in a new position, it is worth considering.

In this case, the strike is $8.64 in-the-money. This means, the cost-to-close will be $8.64 + a time value component. If the b-a spread is $6.30 – $9.00, the cost-to-close will be between $8.64 and $9.00. Let’s use worst case scenario and say $9.00. This means the time value cost-to-close is $0.36 0r 0.36% My threshold would be 1.36% or higher for initial time value return on a new position or I would allow assignment and congratulate myself on an outstanding trade.

Alan