This article will highlight one of the many ways we can establish a monthly covered call writing portfolio during bullish market conditions. We will utilize a hypothetical portfolio of $100k and use 5 different securities, 3 stocks and 2 exchange-traded funds (ETFs).

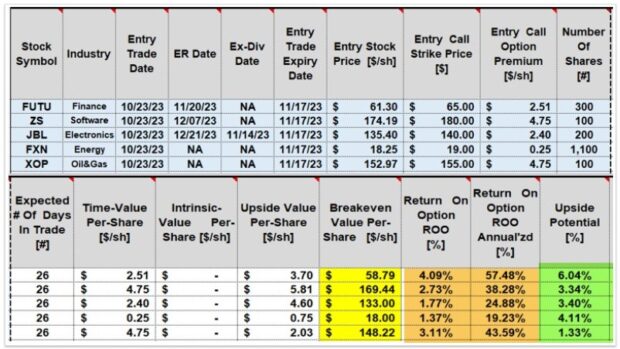

Premium Stock Report for the November 2023 contracts (10/23/2023 – 11/17/2023)

- FUTU, ZS and JBL are eligible securities in 3different industry segments.

- No earnings reports are due prior to expiration of the November 2023 contracts.

- All have adequate option liquidity (open interest- OI).

ETF (Exchange-traded funds) Report for the November 2023 contracts (10/23/2023 – 11/17/2023)

- FXN and XOP are the 2 top-performing ETFs the week prior to the start of the November 2023 contracts.

- Both securities have out-performed the S&P 500 over both the 1-month and 3-month time frames.

- Both he stock and ETF reports are included in our BCI premium membership.

Cash allocation spreadsheet

- The final portfolio setup spreadsheet displays the # of shares to buy and contracts to sell, while allocating a similar amount of cash to each position.

- There will be a cash balance of $1739.00 for potential exit strategy opportunities.

Initial portfolio and trade calculations using The BCI Trade Management Calculator

- Initial time-value returns range from 1.37% to 4.09% for the 5 positions (brown cells).

- Annualized initial returns range from 19.23% to 57.48% for the 26-day trades (brown cells).

- These are initial returns. Final returns can be higher or lower.

- Since all strikes used were out-of-the-money (OTM), upside potential ranged from 1% to 6.04% (green cells).

Discussion

Setting up a high-quality covered call writing portfolio, involves several considerations. Here are some:

- Stock and ETF selection based on sound fundamental, technical and common-sense principles.

- Adequate security diversification.

- Adequate cash allocation.

- Strike selection based on overall market assessment, personal risk-tolerance and chart technical parameters.

There are many other ways to establish our portfolios for each contract cycle. This article provided an example which utilized many of the critical principles we can employ to ensure the highest possible returns. Keep in mind, this publication did not address position management, the 3rd required skillset needed to achieve the highest possible returns.

Click here for a related video.

Stock Investing for Students: A Plan to Get Rich Slowly and Retire Young

This is Alan’s financial literacy book (not option-related), currently used in 4 universities in the US.

Self-investing starting at a young age can ensure a successful financial future and an early and comfortable retirement. So why is nobody doing this? The answer includes such factors as the social pressures facing our youth, certain pre-conceived ideas regarding our ability to successfully self-invest and the education or lack thereof needed to motivate our youth to undertake such a long-term project. The purpose of this book is to change that way of thinking and create a goal and a user-friendly methodology that will facilitate a plan which will allow you to retire financially secure at a relatively young age.

Click here for more information and purchase link.

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to share some of these testimonials in our blog articles. We will never use a last name unless given permission:

(From Courtney after explaining the BCI PMCC trade initialization formula):

Hi Alan,

It finally clicked. This is what happened to me in December with SMH and X. They both accelerated rapidly and I’m going to close them out. I really like the PMCC method, since I have a smaller account but was a little foggy with calculating my [possible total profit available.

Thank you again for your guidance and support!

Courtney

Upcoming events

1. Las Vegas Money Show & Stock Traders Live In-Person Event

February 22 & 23, 2024

Paris Hotel

Thursday, February 22, 2024, at 4:55 pm – 5:25 pm PST

The PCP (put-call-put or “wheel”) Strategy

Friday, February 23, 2024, at 12:00 pm – 12:45 pm PST

Covered Call Writing: A Streamlined Approach

2. Mad Hedge Investor Summit

Tuesday March 12, 2024

11 AM ET – 12 PM ET

Free registration link to follow.

Covered Call Writing Dividend Stocks to Create a 3-Income Strategy

Covered call writing is a low-risk option-selling strategy that generates weekly or monthly cash-flow. By mastering the skill of strike price selection and adding dividend distributions, a potential 3-income strategy can be crafted with a goal of beating the market on a consistent basis.

Topics covered in this webinar include:

- Strategy analysis

- Option basics

- What is covered call writing?

- Dividend distribution

- Stock selection

- Option selection

- Trade management

Real-life examples will be highlighted with Dow 30 stocks using option-chains and calculation spreadsheets.

Attendees will have the opportunity to participate in written chat box Q&A during the entire webinar.

A deeply discounted comprehensive package of educational products and tools will be offered in the final minutes of the webinar.

3. Long Island Stock Traders Meetup Group (private investment club- Part II)

Thursday March 14, 2024

7:30 PM ET – 9 PM ET

Club members only

4. BCI-Only Webinar

Thursday April 11, 2024

8 PM ET – 9:30 PM ET

Topic, description and free registration information to follow.

All questions related to covered call writing and cash-secured puts will be answered in real time after the webinar presentation.

5. Stock Traders Expo- live event in Orlando Florida

October 17 -20

Details to follow.

Hi Alan,

Hope you don’t mind me asking a question which has been bugging me for several days now. I can’t get to the answer no matter how hard I try.

It is simply a matter of how to calculate the Final Net Option % Return for the Mid-Contract Unwind Exit Strategy detailed on page 32 of your Exit Strategies for Covered Call Writing and Selling Cash-Secured Puts book.

I believe I understand how the Final Net Option % Return works for other Covered Call strategies, but the Mid-Contract seems to follow a different logic and I just can’t figure it out – very annoyed with myself!

It may be that it is because this is an ITM call – but not sure. I have read your notes on the Trade Management calculator but am no wiser.

My calculation is – ($4.80) Final Net Option Loss divided by ($96.87 Stock Price + $9.70 Option BTC) = 4.50%. According to the book the answer is 4.96%.

On a secondary point, is there any advantage in using ‘order flow’ software when trading options? This seems to give a better indication where prices are heading but is it really too short a time period for options? Would welcome your views.

My last foray using the BCI system was cut short by illness a couple of years ago. Am looking forward to getting back into it.

Regards,

David

David,

Welcome back, glad your recovered from your medical challenges.

Let’s resolve this calculation:

In this trade, 100 shares of NUE were purchased at $96.87 and the $95.00 ITM call was sold for $4.90. As the stock price accelerated to $104.28, the call was bought back at $9.70, and the shares were sold.

Your dilemma is on the option side, so let’s focus on that:

Net option debit = $4.80 ($9.70 – $4.90)

Cost basis = $96.87 (cost of shares)

$4.80/$96.87 = 4.96%

As far as order flow software to determine our trades, I would focus on these items instead:

1. Quality and liquidity of the underlying securities.

2. Liquidity of option premiums.

3. Premiums meeting our pre-stated initial time-value returns.

These will guide us to setting up our trades. From there, we move to position management mode, and you’re off to a great start with the book you are reading.

Alan

Dear Alan good morning,

I already watch couple of times the video attached to your email (4. How to Use the BCI Premium Reports: NEW UPDATED VIDEO) and I have a question:

Since I have a margin account my buying power is much higher than the “Net Liquidation Value”, definition used by Interactive Brokers to point out how much money is in my account.

My question is:

may I use part of this “buying power” to setup my portfolio?

For example with an account of 50,000 USD and buying power 100,000 USD may I setup a portfolio of 70,000 USD?

I hope to have been clear with my question since English is not my mother language 😊😊 .

Have a nice day

Mauro

Mauro,

You’re English is perfect!

I have never been a fan of margin accounts for retail investors. Trading on margin may be appropriate for a small group of sophisticated, experienced, well-funded retail investors.

You can use margin to purchase additional shares and then write calls against them. So, the answer is yes, it’s allowed in margin accounts.

Since we are “borrowing” money from our brokers to purchase these additional shares, we must factor in the interest rate we are paying, when calculating our final returns.

Alan

Jim,

On the Blue Chip (Dow 30) report, how do you determine which stocks to select? Top 1 month performers?

Thanks a lot.

Jim

Jim,

1-monthg price performance certainly is important, but not our only consideration. Here are some other factors contained in these reports that assist in guiding us to craft our portfolios:

1. Implied volatility: As an example, CRM has an IV triple that of the S&P 500. Does that align with our personal risk tolerance? Maybe yes, and maybe no. It varies from 1 investor to the next. No right or wrong here.

2. Does the earnings report date fall within the contract we are considering? If yes, avoid. Weekly options can be quite helpful in circumventing ER dates.

3. Price-per-share: As an example, if we have $30k available to purchase 1 more security, it couldn’t be MSFT which is trading > $400.00 per-share.

4. Also available to us is 3-month price performance. All eligible securities in our Blue Chip reports have out-performed the S&P in both 1- and 3-month timeframes, but we can analyze the 3-month timeframes as well.

Our goal is to provide our members with as much relevant data to assist in making high-quality investment decisions.

Alan

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 02/16/24.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them on The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

https://www.youtube.com/user/BlueCollarInvestor

Reminder: Premium Member’s pricing is locked into your current rate and will never see a rate increase as long as the membership remains active.

Best,

Barry and The Blue Collar Investor Team

Good morning Alan,

I’ve been meaning to ask about how to work with the stocks that ‘passed previous weeks’ and failed current week.

They wouldn’t be my first choice for new purchases, but what to do with these if I had some of them when the options expired.

Would you sell for the next option period or sell calls on them, but ITM?

Thanks,

Audrey

Audrey,

Stocks in the “pink” cells which failed the current week’s requirements, are beginning to show breakdowns of the technical parameters. Can this turn around the following week? Yes, but it is a red flag.

If we decide to keep these securities for the upcoming contract cycle (weekly or monthly), I agree, that ITM call strikes would be appropriate and reasonable defensive approaches to both generate cash flow and give us additional downside protection.

Alan

Good morning Alan.

I wanted to run something by you. I took an options course a few months ago. The guy is a big fan of covered calls. He said he writes calls weekly, and every Friday, he buys back the call to close out the position. Then he writes a new covered call for the upcoming week.

He said his investing goal was income from the covered calls, but he acknowledged that it can be costly to close them out if they are in the money. He argued that this still made sense because the increase in the value of the underlying shares was often greater than the cost to close the position.

After taking that course and reading your book, I’ve been doing some covered calls. It’s gone pretty well, but I’m having a hard time wrapping my head around the notion of closing out every position every week when you could just let the call get assigned and open a new position on Monday morning.

Does this make any sense to you?

Thanks.

Pete

Pete,

Here are some points to clarify this scenario:

1. If a covered call strike is expiring ITM, we can close the call on Friday (as presented to you) and re-open on Monday. The rationale for this approach is to avoid weekend risk of the shares declining in value (if we retain them) and then can be re-purchased on Monday at a lower cost-basis. The cost-to-close (CTC) will be the small time-value component of the CTC premium.

2. We can also allow exercise of the option and sell the shares at the strike price and avoid the small time-value CTC debit and re-purchase the shares on Monday (your suggestion). This will save us the small time-value CTC and benefit us if share price declines when the market opens on Monday but hurt us if share price opens higher.

3. My preference would be to “roll” the option. Buy-to-close on Friday before 4 PM ET and STO the next cycle’s same or higher strike. This will cost a small debit in time-value but ensure that our cost-basis remains the same for a security that performed well the current contract cycle and we want to retain for the next.

4. The rise in share value (from the strike to current market value) will not be greater than the cost-to-close. It will mirror the intrinsic-value component of the CTC premium, but we will not be” compensated” for the time-value CTC. Here’s an example:

Buy shares at $48.00.

STO the $50.00 call.

On expiration Friday, shares are trading at $55.00.

CTC is $5.10 ($5.00 intrinsic-value + $0.10 time-value)

When we close the $50.00 call, shares move up in value from $50.00 (our original contract obligation to sell) to $55.00 (current market value), a gain of $5.00. However, we paid $5.10 to close. The CTC will always be slightly greater than share appreciation at the time of the close.

Alan

Hi Alan

I hope you are well. For what it’s worth, I am spreading the word on your good work. My family members are now reading your books.

I have a dumb question. Say I bought stock XYZ a while ago at say $90 and the stock is now trading at $93. I write a covered call at $92.5 for $1.86. Would my cost basis be considered $90 or $92.5?

If $90, then I assume my one-month return would be (1.86-0.5)/90 = 1.5%. Is that correct?

Thank you!

Dave

Dave,

In our BCI community, there is no such thing as a “dumb” question. We’ve all asked the same questions early on.

That said, let’s break this down trade (see the screenshot below):

Since the stock is trading at $93.00 at the time of trade entry, that is our cost-basis … $93.00. This is the price of the stock we enter into our spreadsheet. It doesn’t matter what price XYZ traded at in the past.

Now, the $92.50 strike is in-the-money (ITM) so there will be some minor downside protection of the time-value profit (from $93.00 to $92.50). Our Trade Management Calculator (TMC) will deduct the $0.50 of intrinsic-value (amount the strike is lower than current market value) to decrease the cost-basis from $93.00 to $92.50.

The $1.86 in premium breaks down as follows:

$1.36 in time-value (initial profit) + $0.50 in intrinsic-value (not profit). The spreadsheet calculates initial profit (23 days in trade) to 1.47%, 23.33% annualized, based on a 23-day trade.

The downside protection of that initial profit is $0.50/$93.00 = 0.54%

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Alan

Hi Alan,

Wow! I’m glad I asked! I was off on both counts! I assumed that my original purchase price was the cost basis, not the price at the time of the trade.

As usual, thank you so much! So helpful!

Dave

Premium members:

This week’s 4-page report of top-performing ETFs has been uploaded to your premium site. The Select Sector SPDR section is now crafted to align with our streamlined (CEO) approach to covered call writing. The report also lists Top-performing ETFs with Weekly options, mid-week market tone as well as the implied volatility of all eligible candidates.

Premium member video link:

https://youtu.be/EXMO-KwZuJs

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

Alan,

I have a question.

The trading platform I use is TD TOS.

I started the day with about $108.5K in one account.

I bought stock and sold options. Option sales amounted to about $3265. The TMC says the ROO is $2632(the difference from the sales amount is the intrinsic value).

But the total account in TOS does not go up.

By the end of the day, the shares were down about $500 so the account ended the day at $108K.

But if the loss on the shares didn’t account for the income , what happened to the income from the options?

The reason I’m asking is I had this idea that the income form the shares is usable instantly. Not so?

Regards,

John

John,

This is related to broker accounting procedures (see screenshot below).

Let’s start with this: The cash from the sale of the options is in the cash account and available for trading within a day or immediately, depending on the broker.

However, in the “activity” section of our broker platform, the sold options are listed with a bracket or negative sign, since these are short positions. Once the options expire worthless, are closed or are exercised, those brackets or negative sign will disappear and we will see a true, realized portfolio net worth.

When we buy shares, the activity section will reflect a positive #, indicating a long position.

These are common accounting practices for most brokers and confusing, initially, until the rationale is understood.

Bottom line: The cash from option sales is, in fact, in our cash accounts and available for trading, but the activity section of our statements will reflect long & short positions.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Alan