Selling covered call and cash-secured put options are used to generate cash flow. Our knowledge of these options can also be applied to mitigating losses after a stock we own declines in value. This article highlights how options can be used to reduce losses in “stock only” portfolios. Although this article was scheduled to be published several months from now, I thought it appropriate to move it to the front of the queue given the recent decline in the stock market.

When to consider the stock repair strategy

- Shares were purchased at a price significantly higher than current market value

- Breakeven is an acceptable target

- Not willing to add additional cash to the position

- Not willing to add any additional downside risk

How to structure the stock repair strategy

- Let’s say we buy 100 shares of BCI at $60.00 and a few weeks later the stock is trading at $50.00

- Buy 1 x $50.00 call for $4.00 (buy 1 at-the-money call)

- Sell 2 x $55.00 calls for $2.00 (sell 2 out-of-the-money calls between current market value and original share purchase price)

- Net option credit or debit should be near $0.00, in this case it is $0.00

Possible outcomes

Stock price continues to fall below $50.00

Both options expire out-of-the-money and worthless. Since the options did not cost us anything, the option strategy had no impact on the outcome either way and we continue to lose on the stock side. Our position continues to have more risk but no additional risk due to the option positions.

Stock price stays at $50.00

Similar to the above scenario, the options expire worthless and the option positions had no impact on the ultimate outcome.

Stock price moves up to the $55.00 strike

There is a $5.00 loss on the stock side ($60.00 – $55.00) and the $50.00 long call has an intrinsic value of +$5.00, resulting in a breakeven outcome. Notice that by initiating the stock repair strategy, we are lowering our breakeven from $60.00 to $55.00.

Stock prices rises to $60.00 at expiration

The long call $50.00 is worth $10.00 and the 2 short calls have a net debit of $10.00 (-$5.00 x 2) for a total value of zero. Since the stock was purchased and currently is worth $60.00, we find ourselves also at a breakeven situation. This will remain the case no matter how high share price moves so we are giving up upside profits.

Option chain example using American Express (NYSE:AXP)

Stock Repair Strategy: AXP Option Chain

If AXP was purchased at $79.00 but is currently trading at $75.00, we would look to buy an at-the-money $75.00 and fund it with 2 out-of-the-money short calls. In this scenario, we would buy the $75.00 call for $2.45 and sell 2 $77.50 calls for $2.44 ($1.22 x 2).

Advantages of the stock repair strategy

- Creates an opportunity to recover losses by lowering our breakeven

- Does not require additional cash as would doubling down (dollar-cost-average down by buying more shares at a lower price)

- No additional downside risk

Disadvantages of the stock repair strategy

- Downside risk remains unchanged; continued share decline results in additional loss

- Upside is now capped

- As with all positions, management may be required

Discussion

Our knowledge of call and put options can be applied to other strategies. The stock repair strategy involves buying 1 at-the-money call option which is funded by selling 2 out-of-the-money call options. This will then lower our breakeven, facilitating opportunities to recover unrealized share price losses.

***The BCI team will be producing a full webinar regarding this strategy for premium members and will also be creating a Stock Repair Calculator. Here is a sneak preview:

BCI Stock Repair Calculator

Upcoming event

AAII National Investor Conference: Las Vegas Nevada

October 26 @ 8:00 am – October 28 @ 1:00 pm

October 26th – 28th, 2018 (Friday through Sunday)

Alan’s presentations: Saturday October 27th at 9:30 AM and 1 PM

Visit Alan, Barry and the BCI team in the exhibit hall Friday, Saturday and Sunday

Just added

New York City: March 10, 2019

Philadelphia: September 2019

Details to follow

Online discount broker file updated

Located in the Free Resources section of the general site and in the “Resources/Downloads” section of the premium member site.

Market tone

This week’s economic news of importance:

- IMF World Economic Outlook 2019 3.7% (3.9% last)

- NIFB small business index 107.9 (108.8 last)

- Producer price index September 0.2% (as expected)

- Wholesale inventories August 1.0% (0.6% last)

- Weekly jobless claims 10/6 214,000 (205,000 expected)

- Consumer price index September 0.1% (0.2% expected)

THE WEEK AHEAD

Mon October 15th

- Retail sales September

- Business inventories August

Tue October 16th

- Industrial production September

- Home builders’ index October

Wed October 17th

- Housing starts September

- Building permits September

- FOMC minutes

Thu October 18th

- Weekly jobless claims 10/13

- Philly Fed manufacturing October

- Leading economic indicators September

Fri October 19th

- Existing home sales September

For the week, the S&P 500 moved down by 4.10%% for a year-to-date return of 3.50%

Summary

IBD: Market in correction

GMI: 0/6- Bearish signal since market close of October 8, 2018

BCI: An extremely volatile and down week has made decisions for the November contracts unclear a week prior to expiration of the October contracts. The trade war with China, tariffs and a rising interest rate environment has combined for a nervous, irrational stock market, hopefully short-term. Friday’s action was encouraging. This past week was a perfect example of where “hitting a double” opportunities must be explored. The VIX popped above 20, the first time since April 2nd and only the 3rd time in the past year. Each previous time, the market recovered and the VIX declined. Earnings season results, the Fed re-thinking another rate hike this year and calming of trade war rhetoric with China are factors that can lead to a re-establishment of the bull market.

WHAT THE BROAD MARKET INDICATORS (S&P 500 AND VIX) ARE TELLING US

The 6-month charts point to a neutral-to- bearish tone. In the past six months, the S&P 500 was up 5% while the VIX (21.31) moved up by 22%.

Wishing you much success,

Alan and the BCI team

At the beginning of the article, you said to sell 2 out of the money options…..however, you only own 100 shares of underlying…..doesn’t this pose a risk in the event that they both get assigned, and you only have the 100 shares? I’m probably not thinking this through.

Joanna,

The concept is a bit tricky in that it is different from what we usually do.

You are 100% correct that we must avoid naked option-selling. However, with this stock repair strategy the 2nd short call is “covered” or protected by the additional call purchased. We are long (own) 100 shares + long 1 call contract and these positions protect the 2 short calls.

Alan

Andrey,

This is not a naked option scenario. The 2nd short call is “covered” by purchasing the long call much like the “Poor Man’s Covered Call” where a LEAPS option is purchased and short calls are sold against that position.

I would check with your broker regarding how these trades are managed as there may be specific rules that apply and vary from broker-to-broker.

Alan

Alan, as usual you are GREAT!

But how to enter all these 3 legs?

Poor man’s c.c. together? and

the c.c. like a usual c.c.??

Andrey,

The shares are already owned prior to executing this strategy.

Step 2: Buy the near-the-money long call.

Step 3: Sell 2 call options against the (now) 2 long positions to fund the long call.

Alan

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 10/12/18.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are at the start of Earnings Season, be sure to read Alan’s article, “Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The BCI Team

barry@thebluecollarinvestor.com

Alan;

How often do you use the stock repair strategy? Do you look at calls 30 days out?

Best;

Terry

Terry,

Since the majority of my stock portfolios is dedicated to covered call writing and put-selling, I have no need for the stock repair strategy. I use the exit strategies detailed in my books and DVDs for position repair or enhancement.

I select the topics for my blog articles based on member feedback and recently there has been a lot of emails regarding this strategy and that’s why I published this article much sooner than originally planned.

Typically, the strategy uses contracts that expire in a 30 – 45 days range.

Alan

Good strategy! But will you be needing additional margin from your broker to sell the 2nd Call ( will it be considered as a naked/unprotected short call?) or because of your long Call, additional margin will not be required?

Andrey,

This is not a naked option scenario. The 2nd short call is “covered” by purchasing the long call much like the “Poor Man’s Covered Call” where a LEAPS option is purchased and short calls are sold against that position.

I would check with your broker regarding how these trades are managed as there may be specific rules that apply and vary from broker-to-broker.

Alan

Alan,

my small experience with “Repair Strategy” was very positive.

I had 3 successful trades where the repair added aprox. 2% gains to my original CC trade, and 2 neutral results, where the repair went worthless without any damage to my original CC trade.

As a matter of fact, I have currently a repair on NSP

I did buy back the 10/19/18 short leg last Thursday at 10% of the value recieved, and may get a positive result if the 10/19/18 long leg recovers next week.

Roni

I’m accustomed to you teaching SELL SELL SELL… Are you saying that when executing a @ the money long BUY call contract the brokerage will allow that contract as collateral when executing a SELL to call option contract?

Thanks

Joseph,

Yes, the long call protects the short call. In essence, we have a covered call trade with the shares and 1 short call and a bull-call spread with the ATM long call and OTM short call.

I am almost always on the sell side of options. That’s where I have found the greatest return success. The stock repair strategy is geared to “stock-only” portfolios where share price has declined and we use our knowledge of stock options to lower our breakeven without adding additional cash to the trade.

Those who feel that using this strategy would be useful for their trading style, check with your broker to determine the level of trading approval required.

Alan

Alan,

In your recent article on repairing your stock depreciation situation, you started with this stipulation:

How to structure the stock repair strategy:

•Let’s say we buy 100 shares of BCI at $60.00 and a few weeks later the stock is trading at $50.00

•Buy 1 x $50.00 call for $4.00 (buy 1 at-the-money call)

•Sell 2 x $55.00 calls for $2.00 (sell 2 out-of-the-money calls between current market value and original share purchase price)

•Net option credit or debit should be near $0.00, in this case it is $0.00

1.Assuming we do not sell naked calls, rather only covered calls, if we have only 100 shares of BCI stock, how can we sell two contracts covering 200 shares of stock. Does buying a call give us the equivalent ownership of 100 shares of BCI thus allowing us to sell the 2nd contract?

2. If so, I assume the expiration date must be the same for the two contracts (otherwise, if the purchased call expired before the sold call, the latter would be “naked” until it’s expiration date)?

3.As the market price of BCI starts climbing to, say, $53, might the seller of the $50 call see which way the wind was blowing and choose to execute the contract, thus “robbing” us of $2/share when it hits $55?

Jim

Jim,

This is not one of our exit strategy choices for our covered call writing portfolios. It is most appropriate for ” stock only” portfolios where we want to lower our breakeven without adding additional cash. For ccw trades, we use the arsenal of position management techniques detailed in my books and DVDs.

My responses:

1. The second short call IS protected by the long ATM call option. This leg becomes a bull put spread, much less risky than naked option-selling. The long call guarantees us the right to own these shares at the strike price by the expiration date.

2. Yes, the expiration dates are the same.

3. When we purchase a call option, exercise is determined only by us, the call buyer up to expiration. The option seller has no exercise rights, only contract obligations. The seller of a call option can buy back the option but that will not impact our position in any way.

Alan

Alan,

I have 2 questions.

1. Convert Dead Money to Cash Profits.

In this strategy, at anytime during the contract cycle, when the stock price drop significantly, and when the technical is negative, we would back back the option, sell the stock, then buy a new stock and sell the option.

At what percentage of stock price decline is considered significant? Would you say when we break even?

2. Mid Contract Unwind.

Do we deploy this strategy during the first half of the contract cycle?

Thank you Alan.

Byung,

1. We close the short call and long stock positions simultaneously, when share price is significantly under-performing the overall market (S&P 500). A good guideline range would be 8% – 10% from share price when the trade was entered. Frequently, this will occur after taking other action like rolling down. This fits the range offered by IBD recommendations and my guideline for setting 10% trailing stop-loss orders in longer-term buy-and-hold portfolios (found in my book, “Stock Investing for Students”).

2. The MCU strategy is generally employed in the first half of a contract or very early in the second half of a contract. We seek to generate at least 1% more than the time value cost-to-close.

Alan

Hello Jay,

where are you ?

Roni

Roni,

Leave it to you to think of a fellow traveler on the road and reach out to him – thanks! I hope I am not lost in the wilderness :).

I have been monitoring the Blog: I am glad many new voices have joined us!

Plus thanks for your continuing contributions as always….

I have been portfolio over writing. But since the market is my main hobby I have spent more time day trading buying and selling options using support and resistance levels to leverage the heightened volatility priced into them these days. I use SPX since it is a cash settled equivalent of SPY and you never have to worry about being assigned anything except cash! It’s options move dramatically on M/W/F when it expires which can be good and bad :)!

Not the sort of trade we typically discuss here. But I encourage anyone interested with the time to study up on it to do so.

Roni, it was kind of you to ask about me :)! My penny in the pond is a down US market until our elections. So that is how I have been trading it. – Jay

Hi Jay,

I missed this your reply on the 15th and just read it now.

Your trades intrigue me, but I presently do not have the time to study them in earnest.

Your tip about the elections event is very much apreciated.

Roni

Alan – Regarding this blog on “Stock Repair Strategy” would you please clarify something. In the BCI example you’re buying one call at the money and selling two calls out of the money. Is it correct say that both of these transactions are uncovered? Specifically, are the two calls being sold covered by the underlying stock?

Thanks. Mike

Mike,

Both calls are covered, one with the long 100 shares owned and the other with the long ATM call. To be clear, there are NO naked option positions with this stock repair strategy.

Alan

Alan.

Thanks for your response. Perhaps I’m missing something fundamental with this strategy so I’m hoping you’ll please indulge me for a follow-up question.

Here is the BCI stock repair strategy example as I understand it:

Buy 100 shares of BCI @$60

Buy 1 $50 call for $4.00

Sell 2 $55 calls for $2.00

If I understand your response below, one of the $55 calls being sold is covered by the 100 shares of the underlying stock (this part is clear to me). The second $55 call being sold is covered by the purchase of the $50 call for $4.00.

Can you explain how buying the $50 call is covering the second sold call at $55? It sounds like buying the $50 call is somehow the equivalent of owning another 100 shares of the underlying stock. I assume that 200 shares of the underlying are needed to write the two $55 calls.

Also isn’t buying the $50 call for $4.00 a naked position? What is “covering” this position given that the 100 shares of the underlying are covering the sale of one of the $55 calls? Does a Broker typically allow this?

Again I greatly appreciate your assistance with these questions.

Take care,

Mike

Mike,

Buying the $50.00 call gives us the right, but not the obligation, to purchase BCI at $50.00 at anytime up to 4 PM ET on expiration Friday. We are in total control determining whether that option is exercised, closed or allowed to expire worthless if the strike expires out-of-the-money. In essence, it is the equivalent of “owning” the shares if we decide to…our choice. If the short call is exercised (not in our control), we can then exercise the long call and cover the shares at the strike price, $50.00 in this case.

A naked option scenario would exist if we sold a call and did not cover it with either a long call or the underlying shares. The term does not apply to buying a call option. If we sell a naked call, our risk is unlimited. If we buy a call, our risk is the premium paid for the call.

The 2 short calls are “covered” by the 1 long call and the 100 shares owned.

Brokers will allow this type of trading based on the level of trading approval defined by that brokerage.

Alan

Hi Alan,

I am a new trial subscriber. I have traded call, puts and some spreads over the last few years. However, I have never sold covered calls before. I love the resources you provide on your website.

My question is where do I begin to trade i.e. ETFs, Stocks, Blue Chips or Dividend Capture ? I am 70 years old, retired and I’d like to start out with some conservative positions.

Thank you David

David,

Welcome to our BCI community.

You are taking an intelligent approach and that can’t be overstated given the unusual market downturn over the past 2 weeks.

Paper-trading with an ETF or Blue Chip account is a good place to start. Set initial time value return goals on the conservative side, say 1% – 2% per month. That’s the criteria I set in my mother’s (more conservative) portfolio. Perhaps, set up 2 accounts. One for ETFs and one for blue chips. Use a cash amount you plan to fund your accounts with when you go “live”

Make sure you master all 3 required skills (stock selection, option selection and ***position management). As a premium member, we will do most of the legwork regarding stock (or ETF) selection. In a few months, you’ll be all set to initiate your positions and start generating cash flow.

Alan

Hi Alan,

Since the correction started, I have bought – back all my 10/19 short calls, and I’m looking at a considerable total paper loss.

As this is a broad market situation, with no specific aparent motivation, I have not done any changes to my positions.

I am waiting for it to blow over, hopefully soon, and I wonder if you agree with my reasoning.

Roni

Roni,

I am (and most anyone in the stock market) in the same position you describe. I, too, have closed short calls and rolled down in several instances…still leaving paper losses on the current month’s contracts. I will wait until Friday to re-evaluate how to manage next contract month’s positions.

The US and global economies have not changed in the past 10 days but China, Saudi and interest rates concerns are impacting the market in the short-term.

Non-emotional trading is especially important during these aberrations.

Alan

Alan,

thank you for your prompt help.

Roni

Analysts are all over the place…

I was down 5% yesterday….Now this afternoon, down 2.5%. All positions long.

I see KBE is lagging the others (Bank ETF).

EWW recovering nicely.

Too late now for Hit Double, but not complaining.

Mario

I meant down 2.5% for the month.

Roni,

My hunch is some of the uncertainty in the current market will be resolved by the US elections.

What I plan to do, and thank heavens nobody need follow my advice, is keep buying things I think are quality in small batches on down days then wait to cover them when October expires until after the election.

A two and a half week period simply holding stocks and ETF’s uncovered will not kill me :)! Or, if the itch is too strong to have some protection, cover half my holdings ATM or ITM and leave the rest alone until an outcome is known and digested or use weeklies and skip the election.

An even more conservative approach would be to just sit on any cash freed up this Friday until then. But you risk not buying on what are likely to be some good wash out sale days before month end. I am sure as heck not going to sell anything now and take loses since a rally in November is better than a coin toss bet in my opinion and I know I can’t time it exactly. – Jay

Hi Jay,

good to see you back and well.

The elections, yes, I have forgotten about them. You are correct.

We have decisive elections here in Brazil too on October 28.

It’s the 2nd stage for president. far right candidate Bolsonaro will probably be confirmed against leftist Haddad.

This would be very good news for the Brazilian economy, and for my company too.

Roni

Hey Roni,

I hope your election turns out in your and Brazil’s best interest. Oh, and in mine too – I hold some EWZ and hope it bounces on Oct 29th :)! If you get a minute please look at the holdings in EWZ and let me know if there is a better ETF for Brazil? Thanks.

SPY is the best one I can think of if you wanted to boil the US down into one ticker symbol. But I fully realize you know US stocks inside and out by name and trade them every month. – Jay

Hi Jay,

I will check out the EWZ this weekend, and let you know next week.

I expect it is based on the best brazilian stocks taded on the B3, which is the Sao Paulo stock exchange, and the most important in Brazil.

the MSCI index is very similar to the Dow, and it has climbed steadily on the expectations for the Bolsonaro win..

Last Monday the polls showed him gaining momentum at 59% against his opponent Haddad at 41%.

Roni

Jay,

You have all permutations covered in your post. Now, which is the sure winner!

Mario

Hey Mario,

If I knew which one was the sure winner do you think I would be hanging around with you guys on a comment blog :)?

When I got Alan and Barry’s new book I just dove into it skimming around. Only last week did I read the full intro and learn you were also a contributor. Well done!

Today was a fun day with the market up big. I have read that a characteristic of a down trending market is large one or two day up moves. There is even a term for them: “Dead Cat Bounces”.

Hard to say if this is one of those? It did give me the chance to get out of some call spreads and add a couple put positions. I also wrote a couple cc’s today. Best regards, – Jay

Thanks for noticing the mention in the CCW Alternative Strategies book. Glad to help Alan and Barry.

I like the fact you are always mentioning or using a myriad of trading strategies.

I know you have mentioned in the past the buy and wait sequence, buy long, wait for a rise in price, then add the short call. When that works that’s nice. I tried that a few times and it was nice to have a lower BEP and higher ROO as results. Made a difference. Means one must monitor a position and decide when to buy and hopefully do not have a decline in price.

I did notice we had a discussion in the blog a month or two ago about the buy and wait and the feeling by Alan and a one or two others was it was best to buy the covered call immediately. Most likely to get a better outcome over many trades. I was reading Alan’s Vol. 2 of the Complete Encyclopedia that I purchased this year and noticed that there was a few pages on this very subject. Surprised to see it there. Also searched and found the same article in the blog but it was helpful to read it in the book. Many other good sections in the book as well, including Put-Call parity, volatility.

Mario

Premium members,

New Blue Chip (Dow 30) Report now available to Premium Members:

The Blue Chip report for the November 2018 contracts has been uploaded to the member site. 3 stocks have been removed and 5 have been added from last month’s report.

Alan and the BCI team

Alan,

I have a question regarding your article:

https://www.moneyshow.com/articles/optionsidea-43293/

“Selling covered call options and cash-secured puts is a smarter strategy than buying options because 90% of options expire worthless.“

A covered call limits your profit but not your loss so I don’t understand why this is a smart strategy. If you are bullish, long stock is better than covered call and if you are bearish, selling the stock is also better so in which case this strategy is for you worthless?

Regards,

Jeremy Geneva, Switzerland

Jeremy,

In the article, I define the “…90%…expire worthless” comment as a myth: Then, I clarify:

10% expire worthless

55% – 60% are closed

30% – 35% expire worthless

The reason covered call writing should be considered is that it lowers our cost basis, thereby improving our opportunities for successful outcomes. If we buy a stock for $48.00 and sell the 1-month expiration $50.00 call for $1.50, our breakeven is $46.50, not $48.00.

Let’s now deal with your 2 (valid) concerns:

1. Capping the upside: Our initial 1-month return is 3.1% ($1.50/$48.00). If share price moves above the $50.00 strike, our total realized 1-month return is 7.3% [($1.50 + $2.00)/$48.00]. If the price continues to accelerate, we still generated a huge 1-month return and have our exit strategy arsenal to buy back the option if it is in our best interest.

2. Downside risk if bearish: We never use an underlying when we have a bearish assessment. It is possible that a bullish assessment can become bearish during the contract in which case we launch our position management trades.

To sum up:

After mastering the 3-required skills (stock selection, option selection and position management), covered call writing provides the opportunity to consistently beat the overall market because it lowers our cost basis.

Alan

Checkout Chapter 2 of Alan’s Complete Encyclopedia Vol. 1:

Why sell options?

Why there are so few investors who sell covered call options

Three golden rules for covered call writing

********************

Being able to achieve 1.5-2.5 per month annualizes to 18% -30% per year with ITM covered calls which have downside protection and lower you cost basis with the premium received.

In addition you can select on OTM strike to get your premium plus share apprecitation on a equity with positive technicals and that satisfy your fundamental goals.

There are downsides, which concern me also in a mixed, volatile market. While the S&P has been up 5-8% this year, I am up only 2-3% with the choices I have made in this mixed year (great last 2 years).

With long calls, at the end of one month you may not have exceeded your breakeven which is you strike plus the premium to buy the call.

With a covered call that decides to decline despite it have positive or mixed technicals / fundamentals, you buy back the option at a certain point. so you can avail yourself to other income opportunities is the stock rallies back up. At your buy back 20% or 10% point, I have found you are 4-7% below your entry stock purchase price but 2-4% below your Breakeven.

If you underlying still declines, you can decide to exit complete if your equity has particular negative tone, and it is not the overall market having an issu. A 2% gain on 10,000 underlying is $200. a 10% loss on our covered call is $1000. That wipes out the gains of several covered calls. To compensate, that is the reason you diversify your Account Value, also position some OTM covered call with share appreciation to realize 4% or more.

Mario

Premium members:

This week’s 8-page report of top-performing ETFs and analysis of ALL Select Sector Components has been uploaded to your premium site. The report also lists Top-performing ETFs with Weekly options as well as the implied volatility of all eligible candidates.

New members check out the video user guide located above the recent reports.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

Thanks Mario,

I like to think of options trading as a pyramid. The base is selling cc’s and csp’s. The next is trading spreads and the top with the least capital is speculative buys.

I bought an expiring SPX call today for $700 and sold it for $2800 a couple hours later. I could have just as easily lost the full $700. Trade tiny at the top of the pyramid :)! – Jay

Congrats Jay, you are my hero.

Thanks Terry, I appreciate the kind words.

If you choose to speculate in addition to selling core covered call positions please study it first, do it small and think risk before reward! – Jay

Speaking of speculation I admire any of you who resisted the temptation to buy Lotto tickets :). My significant other and I spent $10. Should we win we will retain Counsel, get a safe deposit box, leave town and go into hiding until we can make sense of it all :)!

Good luck and pleasant weekend to all – see you on the new Blog! – Jay

Jay;

Good advice. BTW no winner so next drawing $1.6 Billion with a B.

Terry,

Good morning! New blog is up so you may not see this but the size of that jackpot boggles the mind. Yet someone will win that and it will change their lives and those of the people close to them and their kid’s kids forever.

I guess that is why the line to get tickets was out the door at my neighborhood Exxon station last evening when I was just getting gas for the car….- Jay

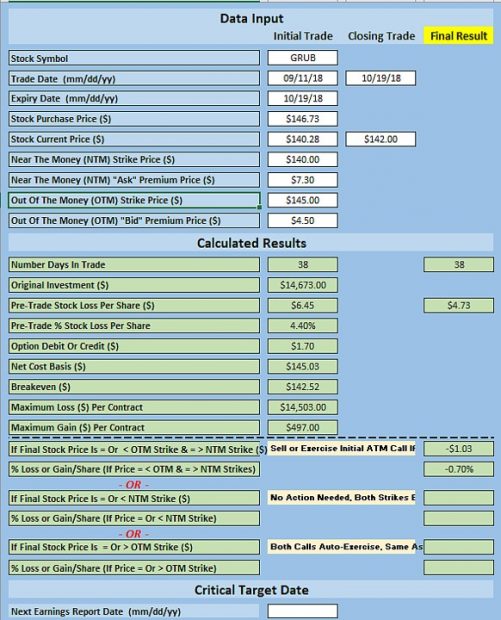

Great article. Question. When I run the numbers, it appears that the maximum gain in the calculator should be $503, not $497. Which is correct?