Covered call writers receive option premiums for undertaking the obligation to sell our shares to the option holder if that holder decides to exercise that right. Understanding when and why exercise will take place is critical to the implementation of appropriate exit strategies and therefore maximizing our option and stock profits.

Let’s first look at our covered call trade from the perspective of the option buyer. As the holder of the call option the buyer’s goal is to make the most money possible. This can be accomplished by exercising the option and buying the stock below market (when the strike price is in-the-money) or by selling the option prior to expiration. If the strike price is in-the-money will the options be exercised early (prior to 4 PM EST on expiration Friday), will they be exercised after expiration Friday or will they never be exercised? To get an understanding of how this works we must first look at the premium of the call option and the equation that defines what the premium consists of:

Option premium = Intrinsic Value + Time Value

The intrinsic value is the amount that the option strike price is in-the-money and time value is the amount above the intrinsic value. If the option buyer exercises the option, the intrinsic value is captured but the time value is forfeited. This means that it is highly unlikely that the option will be exercised early. A rare exception to this rule is when a dividend is about to be distributed prior to expiration and the dividend amount is greater than the time value remaining on the premium. Let’s look at a real-life example to make all this come alive:

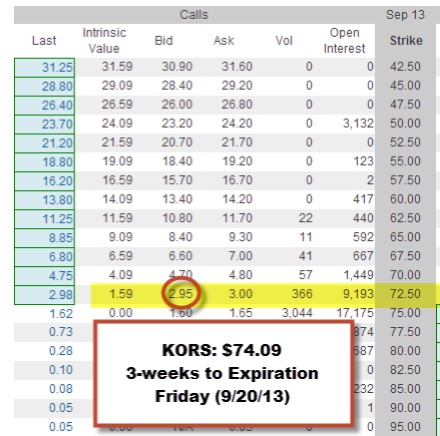

On August 24th, I published an article on this site showing a trade I made using KORS as my underlying. KORS was purchased for $72.36 and slightly out-of-the-money $72.50 calls were sold. As of September 1st, the share price rose to $74.09, leaving the $72.50 calls now in-the-money. The question now is will early exercise occur and my shares be sold? To get an answer, we look to a current options chain:

KORS option chain as of 9-1-13

Amount option holder will receive if early exercise is invoked and shares are sold:

Amount generated = $74.09 – $72.50 = $1.59 or $159 per contract

Amount option holder will receive if option is sold rather than exercised:

Amount generated = $2.95 or $295 per contract

The breakdown of the option premium is as follows:

$2.95 = $1.59 (intrinsic value) + $1.36 (time value)

It is apparent that if the holder chooses the path of early exercise, time value will be lost and that makes no financial sense. Now if there is a dividend distribution prior to expiration Friday in an amount greater than $1.36, early exercise would be much more likely but not guaranteed (many retail investors do not know about dividends and ex-dates).

Are we assured that early exercise will not occur if there is no dividend to consider?

NO. Some investors want to own the stock and will exercise (rarely) even if selling the option will make more sense. We cannot account for other investors making poor financial decisions. These investors should sell the option and then buy the shares at market thereby capturing the time value that early exercise would deprive them of. In these unusual instances, The Options Clearing Corporation (OCC) randomly assigns exercise notices to brokerage firms, which then assigns these notices to their customers (could be you or me!). Our covered call writing decisions should not be based on rare and unusual circumstances but rather on the most likely scenario which is that our in-the-money strikes will not be exercised (barring a dividend issue) prior to 4 PM on expiration Friday. Therefore, if we wanted to hold onto our shares, we would need to buy back or roll the option prior to expiration.

Conclusion

To determine the likelihood of early exercise we need to look at the option premium of an in-the-money strike. Early exercise will result in loss of time value for the option holder and therefore makes no financial sense. Early assignment is possible when there is a dividend distribution or when the holder incorrectly decides to exercise early and the assignment randomly falls to our account.

Upcoming live seminars:

September 24, 2013

Philadelphia Chapter of the American Association of Individual Investors

http://www.aaii.com/chapters/meeting?mtg=2469&ChapterID=22

6:30 PM Registration and 7 PM start.

The charge is $15 for pre-registration and $17 at the door.

Details are available on the above website.

Reservations can be made through Andrew Street at 261 Gypsy Road in King of Prussia, PA 19406

| Start: | September 24, 2013 6:30 pm |

| End: | September 24, 2013 9:00 pm |

| Address: | 540 Fountain , Plymouth Meeting, PA, United States |

October 19, 2013

American Association of Individual Investors Los Angeles Chapter

Alan will be one of two speakers at this event.

Skirball Center 9AM to 12PM

Details to follow.

Market tone:

As events in Syria and investor fear of the Fed decreasing its expansionary monetary policy, the market remains nervous and unpredictable. This week’s economic reports were a mixed bag but the disappointing jobs report seems to encourage many investors that the current monetary policies will remain in effect at least short-term (bad news viewed as good news…go figure!):

- The ISM manufacturing index showed strong growth @ 55.7, higher than the 54.5 anticipated. This was the 3rd increase in a row and a sign of expansion

- The ISM service-sector index rose to 58.6, the highest level since its inception in 2008, up from 56.0 (57 was expected)

- The August jobs report disappointed with 169,000 jobs added, lower than the 175,000 predicted

- June and July payrolls were revised downward by a total of 74,000 jobs

- The unemployment rate for August dropped to 7.3% from 7.4% but mainly because less people were looking for jobs

- The economy expanded at a “modest to moderate pace” according to the Federal Reserve’s Beige Book (a summary of economic conditions in each of the 12 Federal Reserve regional districts (Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco. It provides anecdotal information on topics such as labor conditions, consumer spending, and business activity. Formally called the Summary of Commentary on Current Economic Conditions by Federal Reserve District, it is known as the

Beige Book because of its plain beige cover) - New orders for manufactured goods fell by 2.4% in July (more than the 1.6% expected) after 3 months of increases. Excluding the unpredictable transportation sector, new orders rose by 1.2%

- The nation’s productivity pace (efficiency of producing goods and services) rose in the 2nd quarter at an annual rate of 2.3%, better than the 1.8% anticipated

- The trade deficit for July was wider than expected ($39.1 billion compared to $38.6 billion)

- Construction spending was up 0.6%, more than the 0.4% predicted

For the week, the S&P 500 was up 1.4%, for a year-to-date return of 17.8%, including dividends.

Summary:

IBD: Market in correction

BCI: Cautiously bullish favoring in-the-money strikes 3-to-2

Thanks one and all for your continued support.

My best,

Alan (alan@thebluecollarinvestor.com)

Premium Members,

The Weekly Report for 09-06-13 has been uploaded to the Premium Member website and is available for download.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the BCI YouTube Channel link is:

http://www.youtube.com/user/BlueCollarInvestor

Best,

Barry and The BCI Team

Alan,

I started to paper trade recently. Buying stock is easy,when selling it, since the bid and ask is big spread, I used the middle and less price(close to last price), but it never got filled. How should I handle this matter?

Keith

Keith,

Two points here:

1- Before entering the trade, make sure the open interest (OI) for that option is 100 contracts or more and/or the bid-ask spread is $0.30 or less. If not use a different stock/option pair.

2- To close the short options position, find the mid-point of the spread (mark) and then place a limit order slightly in favor of the market maker. That’s how to execute the trade when trading live. If the paper trade platform will only execute at the published price, move forward with that price realizing that it is not a perfect paper-trading world and your results will ultimately be better than those while practicing. It absolutely still pays to practice. It is essential. Does it pay to practice in the shallow end of the pool before jumping in the ocean? It may not be the same but it must be done! (not my best analogy but you get my point).

Alan

KORS: Trade just executed:

I noticed that KORS was up in price again this morning so I revisited the time value component of the option premium for the $72.50 strike. The bid-ask spread was $3.50 – $4.40. I decided to see if I could “play the b-a spread (pages 222 – 227 of Encyclo[pedia…) down to a $4 premium to close. In less than 10 seconds the trade was executed because the market maker did not want to publish my offer. With the price of KORS trading @ $76.42 at the time, the strike was $3.92 in-the-money so the time value or cost to close was $8 per contract. At this point I have several choices to generate additional cash:

1- Keep KORS anticipating a continuing share appreciation until expiration of the September contracts.

2- Sell KORS (400 shares) and use the $29,000 to start a new cc position seeking to generate between 1-2%

3- Sell KORS if I think its had its run

This is why having a weekly stock watch list is so importrant as opposed to providing it to our members on a monthly basis. My next step is to check the watch list and decide which path to take.

Alan

Alan,

I was looking at your LEAPS strategy and selling DITM calls.

You state as the criteria “Dividend yields must be between 4-8%” Why would it not work for a 10% yielding stock? My guess it that it would be at a higher risk of being assigned.

Thanks,

Dan

Dan,

Stocks that yield > 10% are highly unlikely to be solid performing stocks with adequate trading volume and associated with LEAPS. They are frequently low volume stocks, declining price patterns and without LEAPS (many without options at all). If you can find one that meets our system criteria, I’m okay with that but I made this guideline to help avoid getting into a risky trade. Remember as the price goes down, the yield goes up.

Alan

News of the day:

As of Monday, GS, V and NKE will be added to the Dow 30 and BAC, AA and HPQ will be reoved. Most investors believe that this will have little impact on the markets as most use the S&P 500 as a benchmark.

The recent strength in the markets is partially a result of the decreasing chance of a US attack in Syria and the possible face-saving political solution that has been embraced by the US, Russia and Syria.

Alan

Alan, I’m quite intrigued to see that you got your recent trade of KORS done in only 10 seconds. Just on this, how long does it usually take for an order to get filled- is it usually immediate?, and if my order isn’t filled in this time then shouldn’t I lower my ‘bid’ (or raise my ‘ask’) price for the next attempt, or just keep on trying over and over?

I also left questions to preferably get some confirmation on using beta in the last video blog you did. Thanks

Fred,

Most trades are executed in seconds as long as you enter a reasonable offer. If you enter a limit order between the bid and ask that may not be executed immediately. Check the current price of the option on your brokerage platform after entering the order (if not executed). If the spread has not changed, your order may still be executed…check every few seconds. If you see a new b-a spread with the offer you made now part of the spread, you will then enter a lower offer. You will not always get the better price but you will in a high percentage of the cases if you use all the rules I detail in my books and DVDs. These $20 -$50 bonuses add up over the years.

Alan