Selling covered calls and cash-secured puts are the main strategies highlighted in our BCI community. Much of the information disseminated on the Blue Collar site, books and DVDs is based on member feedback, inquiries and comments. In September 2017, Marc sent me an email question about selling naked (without owning the underlying security before selling the option) out-of-the-money call options against shares with poor fundamentals and technicals. The rationale behind such a strategy is that cash would be generated from the option sale and share price would most likely not appreciate due to the lack of bullish fundamentals or technicals. Options would therefore expire worthless resulting in a near risk-free profit. I decided to publish Marc’s entire email inquiry and my subsequent responses because I feel this is such an important topic for our members to fully understand before deciding on which strategies are most appropriate for our families.

Marc’s email to Alan

Hello Alan,

At last yesterday I managed to open my first covered call positions, thanks to your detailed explanations given in your books and videos and your latest weekly stock report. Now I just sit, wait and read your book about exit strategies 🙂

Some question arose from thinking over after looking into another book from (author name deleted) about writing naked calls (book title deleted).

Briefly: the writer of the named book advertises for selling uncovered deep OTM calls in their book.

My question in this context:

**************************************************************************************************

Wouldn’t it be ok to write a deep OTM naked call on an underlying which has very bad fundamentals and technicals and set a stop buy order (let’s say at a level where the call rises to 100% or 200%) for the underlying just in case it is climbing suddenly?

Some kind of “late covering call writing” this would mean.

If it’s really true that 80% of all options expire worthless then this should be a very easy way of making money via the statistics:

starting with setting stop buy orders on different “bad” stocks, then writing lots of different deep OTM calls on these stocks, and simply wait.

If a stop buy is be executed and then trigger buying back the call (generating a loss on this call) and track/analyze the underlying to look what happened.

The advantage would be that the needed capital would be much less because you do not need to own the stock in most cases.

I am aware that you have to forget about any dividends in this case but maybe it is worth it.

You just would have to do the opposite in a screening process as you do: selecting stocks with poor fundamentals and technicals which even might be easier I could guess.

***************************************************************************************************

Something I must have got wrong because this would be actually too easy and “too good to be true”…

So please tell me: where is the hook in this probably quite bad idea?

Thanks for your great help and support.

Marc

Alan’s response to Marc

Hi Marc,

I never comment on other authors or their books, but I can make some general comments which you should find useful. Let me start with this: If any strategy appears too good to be true, it generally is.

General information:

- Deeper OTM calls generate very little time value premium unless the underlying stock is highly volatile (risky)

- Why would anyone buy that option? They believe it will end up in-the-money. Who’s right?

- Stops at 100%/200% means losing double or triple our investments. It’s all about percentiles.

- It is not true that 80% of options expire worthless. About 1/3 of options expire worthless, 10% are exercised and the rest are closed prior to expiration.

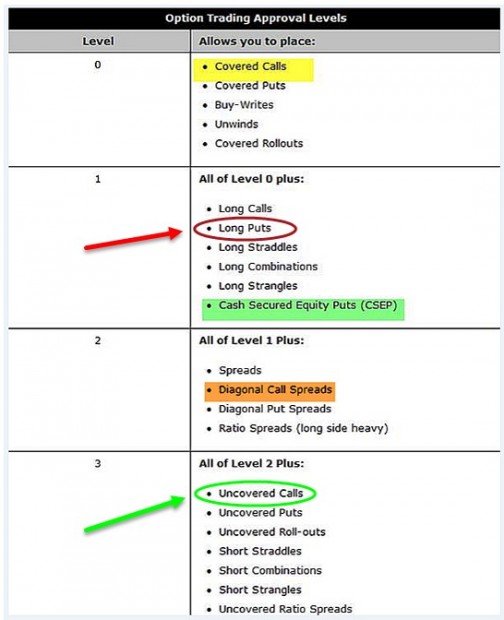

- Naked options are risky. Share price can gap-up and stop losses can be by-passed. Technically, risk is unlimited.

- If bearish on a stock, puts can be purchased where risk is limited to the cost of the put. Put value will rise if we are directionally correct on share value decline. The chart below shows that buying puts requires a lower level of trading approval than does selling naked calls.

- Naked options require a higher level of broker approval. This is because it is not appropriate for most retail investors (see screenshot below).

- We can use covered call writing in our self-directed IRA accounts. We cannot use naked option selling in these accounts because of the implied risk.

- Dividends should not be a major factor when selling options.

- Markets tend to move up in value. Taking bullish positions is riding our bicycle downhill. Bearish positions are like riding uphill. There are exceptions.

- There is no one strategy that is right for every investor and naked option selling is appropriate for some sophisticated investors with high risk-tolerance. For most retail investors, naked option selling is too risky and include me in that latter pool.

Levels of trading approval

Levels of Trading Approval for Calls and Puts

I may use your question and my responses in a future blog article as I view it as a very important topic.

Best regards,

Alan

Discussion

Selling naked call options is a high-risk strategy which may be appropriate for some sophisticated investors with high-risk tolerance. It is not appropriate for most retail investors and that comment is reflected in the higher level of trading approval (compared to more conservative option strategies) required by most brokerages.

New comparison chart now available

Premium members: We’ve had several inquiries regarding the differences between stock options and index options. I created a comparison chart and uploaded it to the member site in the “resources/downloads” section. I will be following this up with either an “Ask Alan” video or blog article or both. Here is the location of that chart:

Upcoming events

1- The Association for Technical Analysis (AFTA): Dallas Texas

“How to Generate Monthly Cash Flow and Buy a Stock at a Discount Using Two Low-Risk Options Strategies”

Tuesday April 17, 2018 6:30 PM – 9 PM

Crowne Plaza 14315 Midway Rd Addison, TX 75001-3505

2- Long Island Stock Trader’s Investment Group

Tuesday May 8th, 2018 7PM -9 PM

Using Stock Options to Enhance Portfolio Returns

3- Las Vegas Money Show

May 14th @ 12:30 – 1:30

4- Just added: Money Show San Francisco

August 23, 2018

Information to follow

Market tone

This week’s economic news of importance:

- Producer price index March 0.3% (0.1% expected)

- Wholesale inventories February 1.0% (0.9% last)

- Consumer price index March (-)0.1% (expected)

- Federal budget March (-)209 billion ((-)176 billion last)

- Weekly jobless claims 4/7 233,000 (230,000 expected)

- Job openings February 6.1 million (6.2 million last)

- Consumer sentiment index April 97.8 (101.0 expected)

THE WEEK AHEAD

Mon April 16th

- Retail sales March

- Homebuilders’ index April

- Business inventories Feb

Tue April 17th

- Housing starts March

- Building permits March

- Industrial production March

Wed April 18th

- Beige book

Thu April 19th

- Weekly jobless claims through 4/14

- Leading economic indicators March

Fri April 20th

- None scheduled

For the week, the S&P 500 moved up by 1.99% for a year-to-date return of (-) 0.65%%

Summary

IBD: Market in confirmed uptrend

GMI: 2/6- Sell signal since market close of March 23, 2018

BCI: Selling 2 in-the-money strikes for every 1 out-of-the-money strike for all new positions. Currently fully invested and slowly re-adjusting portfolio positions to more bullish positions. Global and US economies are a positive while political events are concerning. The Friday evening bombing in Syria was anticipated.

WHAT THE BROAD MARKET INDICATORS (S&P 500 AND VIX) ARE TELLING US

The 6-month charts point to a bearish sentiment. In the past six months, the S&P 500 was up 2% while the VIX (17.41) moved up by 78%. The VIX has calmed a bit from the prior week..

Wishing you much success,

Alan and the BCI team

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 04/13/18.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are at the start of Earnings Season, be sure to read Alan’s article,”Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The BCI Team

barry@thebluecollarinvestor.com

Alan,

Fabulous article on Naked Call options. I expect many comments.

I joined BCI two full years ago after reading many books on options and your Classic Encyclopedia (well worn by now and loose pages as well). I can say confidently you never stop learning about the world of Options. So many ways to look at them and implement investment strategies, from both perspectives of being a holder (owner) or writer (seller).

Your BCI methodology on covered calls makes it easier to implement and manage a particular field of options. The many other ways to invest with options do take time to understand, implement, and manage, which does not necessarily mean they have better overall outcomes in the long run compared to using Covered Calls as you support it.

As you mention, 30% of calls expire worthless. 60% are offset or closed before expiration, 10% are exercised. I imagine some of the reasons are:

* 30% expire worthless: Holders do not realize they can sell the option back some time before expiration and come out ahead because of the remaining time value; the remaining time value do not exceed the commission incurred if the option is closed before expiration.

*10% are exercised or assigned:

A. Holders do not know they could sell back the option to realize the time value for additional profit instead of owning the stock and selling at the market; they want to own the stock; they forgot to close or offset the option before expiration; an ex-dividend date is coming up and holders of a call exercise their right to buy the security by the day before the ex-dividend date.

B. Writers do not want buy back and roll the option because of an upcoming earnings report and therefore let assignment occur – which takes away their stock; do not want to hold a stock position anymore.

*****

It is interesting to note that covered call positions, which includes a purchase of a long stock position with a sold short call want the stock price to be neutral, moderately bullish or moderately bearish (Page 6 Classic Encyclopedia). Moderately bullish because you are limited at the upper end with share appreciation with an OTM strike. Moderately bearish because you have downside protection with an ITM strike and a Breakeven point where the stock and option position begins to have a loss.

Naked call writers, on the other hand, want the stock price changes to be the opposite neutral or bearish, since the maximum reward occurs if the option stays worthless below the strike.

Mario

Alan,

I can’t tell you how many times I read articles claiming that 80% – 90% of all options expire worthless as Marc stated in his question. What you wrote in this article makes more sense. Thanks for setting the record straight.

Marsha

Hey Marsha,

Wouldn’t it be fun to just “be an option” for an expiry :)? How much would our price change? How many accounts would we go in and out of? How many traders would we help or hurt?

In my silly imagination I have wondered the same thing about old worn dollar bills. Since being printed how many people have held this bill? How many states and countries has it been in? How many times has it been taxed :)? How many debts public and private, legal and illegal has it been tendered for?

Oh well, I will never know but fun to ponder! – Jay

Nice response. There is a “famous” trader (Karen ?) whose only strategy was sell naked Puts on poorly perform stocks. One year she made millions, later she lost what she made and more. For a poorly performimg stock a better strategy is a carefully crafted debit vertical Put spread (the short is usually NTM and the long ITM). One then can make money on theta and on delta if one gets the direction right. Also the risk is the debit (money paid to the broker). An alternative is a deep vertical credit spread with the short OTM (delta about -.3) and the long further OTM (delta about .1). Riskier if stock plunges. Or flip it to a vertical call credit spread.

For me vertical credit spreads are like picking up quarters on the tracts in front of a spead train. If you do that type of strategy line up a good gastroenterologist.

Was lucky with a rolldown with KWEB on Thursday and Friday.

On Thursday I rolled down to Strike 16 @ 1.28 for a 2% benefit (Return cost basis 63.73)..

.

On Friday early morning it gapped down over 2% and I was able to offset the position and fill a BTC @ 0.40, 0.42 after commission for a STO-BTC cycle benefit of 1.4% gain ((1.28 – 0.42)/63.73).

The position is still long at a net loss. Waiting for a price recovery or another rolldown opportunity in this very volatile whipsawing market.

Mario

Alan,

With all due respect, writing naked calls/puts is no more “risky” than writing covered calls.

Sure, naked sales must be more closely monitored, but If you purchase underlying X and sell calls on X with a Delta of Y all you’re doing is slowing things down by having a lower net delta.

You can accomplish the exact same thing by selling naked, further out of the money options. The risk is entirely controlled by the seller of the option in that they can choose to close it or adjust it anytime they want.

Chris,

I absolutely agree that careful monitoring will assist in mitigating some of the risk implied in naked call selling.

A few thoughts for your consideration:

1- Covered call writers are undertaking an obligation to sell at the strike price. By owning the shares before selling the option, we know our exact cost-basis. Naked call writing means buying the shares at market (at perhaps a much higher price than the strike sold) or closing the short call at a higher cost if share price rises, our main concern.

2- Monitoring will assist, for sure but doesn’t account for gap-ups when unexpected positive news is made public.

3- Our government permits covered call writing in self-directed IRAs. Not so for naked call writing.

4- Brokerages require a higher level of trading approval for naked call writing while covered call writing is universally the easiest option strategy to get approved by our brokerages.

5- Your point of a lower net Delta is a good one implying less market risk for covered call writing.

Naked option-selling may be appropriate for some but for most retail investors with capital preservation as a main concern, option-selling should be initiated in a more conservative manner, in my humble opinion.

Alan

Chris,

I see where Alan states: “Naked options are risky. Share price can gap-up and stop losses can be by-passed. Technically, risk is unlimited.”

I can see your point, looking at the delta angle.

You could lower the risk, at return expense, by hedging always with a protective long put (married put / collar ) to offset the covered the call delta.

But isn’t the main point of covered calls for BCI’s methodology is to provide a manageable investing environment for IRAs and individual portfolios using carefully selected securities, position management,exit strategies, and common sense principles.

With a covered call, if the stock gaps up, your underlying is just assigned. A naked call would give you large losses with a delta of -1.

In the other direction, price declining, covered calls do suffer a loss with a reduced delta or loss rate initially (1-0.5- 0.5 for an ATM short call, approaching 1 for Deep OTM). but at least you are able to sell the security and you do not need a margin account and its resulting margin calls.

Mario

.

Off subject, but does anyone know of an online discount broker that allows you to issue a “Do Not Exercise” declaration online instead of having to do so by phone?

I buy weekly calls (usually 50 or 100 contracts) and sometimes, on losers, hold them through expiration as there is no market to sell into but there is sometimes the possibility they might go ITM at the last minute and be automatically exercised.

I am with etrade, $4.95 per trade plus $0.50 per contract. Started with PCFN on Prodigy, it was sold to DLJ which was sold to Harris which was sold to etrade. Never been anywhere else. They will not allow an online”Do Not Exercise” declaration.

Thanks,

Hoyt

Hi Allan,

I have a couple of questions: in a very volatile market like this,

1) for covered call writing, how deep do you go ITM strike?

2) for selling cash-secured puts, how far do you go OTM?

Thanks.

Ronnie

Ronnie,

In bear and volatile markets, I set my strikes as follows:

1- Target the lower end of my initial time value monthly return goals (2% – 4%, in my case)…so closer to 2%.

2- Check the option chain and look for ITM calls and OTM puts that approximate these time value return goals…done.

By lowering time value return goals, we will be going deeper ITM or OTM yet still staying within the parameters of our return goals.

Alan

Alan,

I watched your excellent video Ask Alan #145 – “Evaluating A Losing Covered Call Trade””

My question is why did you not have to buy back the two options when you sold the stock, and take that cost as an additional (above the stock loss) loss against the position?

Thank you,

Sid

Sid,

When you review the video you will notice that I did mention buying back the options but the amount of the cost-to-close was not given in Kevin’s email to me. I approximated this cost-to-close by using the 10% guidelines. Without these stats, the loss between share loss and option gain would have been $345 but I used $400 when factoring in these buy-to-close estimated stats.

Alan

Is there any statistics regarding naked Puts options ending up being assigned, worthless?

Andrey,

The best stats I know of are the ones I quoted in this article:

1/3 of options expire worthless

10% of options are exercised

Of course, the specific strikes selected and how they are managed will influence final results.

Alan

Alan,

I have learned a lot about covered call writing from your website, weekly newsletter and books, and I thank you for it. I have a couple of thoughts I’d like to pass along to you.

You often refer selling cash secured puts as “buying a stock at a discount,” and you do make it clear that it is possible the underlying stock might not be purchased, depending on its price movement. Is it correct to describe selling covered calls as “selling a stock at a premium,” with the similar non-guarantee of a stock sale? I never see covered call writing described that way – please correct me if you have previously described it as such. If you have any opinion on this thought thank you for sharing it.

I recently noticed that a stock I follow was trading ATM for a certain strike price, and yet the time values of the ATM call and ATM put for the same expiration date were quite different. I researched this observation and read about volatility skew https://www.investopedia.com/terms/v/volatility-skew.asp as the probable explanation. I think this would be an interesting topic for a future article.

Again, thanks for providing quality educational insights into options trading.

Regards,

Marc

Marc,

Yes, some “imply” that covered call writing is selling a stock at a premium when the goal was to sell the stock anyway and why not get additional premium in the process. However, most covered call writers are leveraging the underlying to generate monthly (or weekly) cash flow rather than selling the stock. Good point.

I have written about volatility skew in the past and have information detailed in the Complete Encyclopedias. Here is a link to an article I published 6 years ago:

https://www.thebluecollarinvestor.com/volatility-skew-understanding-option-premiums-over-different-time-frames-and-strikes/

Perhaps another isn’t a bad idea…I’ve made a note.

Alan

2 quick questions. I have read the entire margin manual for my broker but I cannot seem to have these 2 questions answered regarding assignment/exercise fees.

1. If the options holder decides to exercise before expiration on my covered call, who gets slapped with the assignment fee…me or them?

2. If my covered call expires in the money and it’s auto-exercised, who pays the fee in that case?

Joanna,

Always check with your broker for their trading commission schedule. In general, whenever our shares are sold, be it from auto-exercise or request from option buyer, we pay a trading commission. Some brokerages charge an additional fee if the sale is resulting from option exercise. If that is the case, try negotiating that fee down to a typical stock sale trading commission. If the broker declines, consider a different broker.

Alan

Premium Members:

This week’s Weekly Stock Screen And Watch List has been revised and uploaded to The Blue Collar Investor premium member site and is available in the “Reports” section. Look for the report dated 04/16/18-RevA.

The reason for the revised report is that we updated the Risk/Reward information. As a result, one new stock has passed our screening process added to the report — SKX.

Best,

Barry and the BCI Team

Premium Members,

There was a typo in the Market Overview (first) page of the latest report. The date shown is an incorrect date. The dates should read 04/13/18, not 04/06/18. However, no change to the data content. Thank you John.

Best,

Barry

Hi Alan,

Thank you for providing all the useful investment information. Could you tell me where I can get the option tree you are using, because the option tree in my brokerage account doesn’t show the intrinsic value. I am still learning from your tutorial video. Thank you very much.

Sincerely,

Joe

Joe,

Recently, I have been using screenshots of option chains from cboe.com and finance.yahoo.com.

You can generate intrinsic value information by using the multiple tab of the Ellman Calculator. Download a free copy here:

https://www.thebluecollarinvestor.com/free-resources/

Alan

Joe,

I use Etrade and Fidelity as brokers. Their browser (I use Chrome) platforms do not show give the option to add the Intrinsic and Time Value (Extrinsic) values. But their trading platforms do, which is what I normally use for trading.

It does make it easier to do your calculations if you have the columns shown.

With Fideiliy I like the fact I can set up watchlists of my actual positions with purchase price columns that you can modify. You add options as well. The watchlists can be created in the Browser platform and then opened up in their trading platform Active Trader Pro). You can then add the Intrinsic and Time Value Columns. If you open up the watchilist on a browser, the intrinsic and time value columns do not show up.

With Etrade, in a browser you can open up option chains, but the extrinsic and Time value columns can not be added. In their trading platform, the intrinsic and Extrinsic columns can be added.

With Etrade, in the trading platform simple watchlist can be created, but only with Stock symbols. Options symbols cannot be added. Purchase not options and their is no option to add your own purchase price column that you can modify.

Mario

Premium members:

This week’s 8-page report of top-performing ETFs and analysis of ALL Select Sector Components has been uploaded to your premium site. The report also lists Top-performing ETFs with Weekly options as well as the implied volatility of all eligible candidates.

New members check out the video user guide located above the recent reports.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

Alan,

Would you kindly suggest your favorite stocks or etf’s for writing covered calls at this time. I have about 100k in cash.

Thanks.

Nancy

Nancy,

The stocks and ETFs eligible for covered call writing (and put-selling) are the ones with elite fundamentals (sales and earnings growth), chart technicals and meet our common sense principles like minimum trading volume etc. We update these lists for our members on a weekly basis.

Stock selection is one of our 3-required skills along with option selection and position management. Once mastered, we can begin to grow that $100k.

If you haven’t seen our free beginner’s tutorial (may not apply to you), use this link and put in your email address to get in:

https://www.thebluecollarinvestor.com/beginners-corner/

Alan

Alan,

Please can you help me, my delta for my sold put is -1.000 (as shown in the tab of IB’s TWS platform). This means I have a 90% chance that my sold Put will end worthless?

Thank you!

Andrey

Andrey,

Deltas of in-the-money put options get closer to -1 as expiration approaches. In-the-money options will get exercised if the option isn’t closed (bought back) prior to contract expiration. At-the-money put options typically have a Delta of -0.5, and the Delta of out-of-the-money put options approaches 0 as expiration approaches. The deeper in-the-money the put option, the closer the Delta will be to -1.

If we don’t want the shares “put” to us when the strike is deep in-the-money, we must close the short put position.

Alan

Alan,

I have watched all 8 lesson of yours from YouTube, thanks for sharing the information and knowledge.

I have some queries from your video if you don’t mind me asking. Regarding to your strategy that you are sharing, are they for European type option? The reason why I am asking is, when I am listening to your exit strategy, it sounds like the contract can only have exercise on the expiration date.

The second question that I have is regarding to the premium report. Does it suitable for both European and American type option?

The third question is, how should I determine which strike price I should write?

Last but not least, do you have any particular broker or advise that I should go with?

Thank you so much and looking forward for your reply.

Best regards,

Darren

Darren,

My responses:

1. Since we are using stocks and exchange-traded funds (ETFs) as our underlyings, the associated options are American style which can be exercised at any time. That said, early exercise is rare and when it occurs, is usually associated with an ex-dividend date.

2. Yes, the calculator can be used for European style options but we use stocks and ETFs in the BCI methodology.

3. Strike selection: see this article I previously published:

https://www.thebluecollarinvestor.com/selecting-a-specific-strike-price-for-our-covered-call-positions/

4.Brokers: check out the online discount broker file after putting in your email address at this link:

https://www.thebluecollarinvestor.com/free-resources/

Alan

I have studied the example you have provided of the premium report. In the comments section, you often indicate “MACD” with a down arrow, and “STO” with an up arrow. Could you please explain in more detail what this means?

Joanna,

A “down” arrow for either MACD histogram or the stochastic oscillator indicates a bearish signal and an “up” arrow is used when here is a bullish signal. Here is a link to an article I published last year with more details:

https://www.thebluecollarinvestor.com/using-technical-indicators-to-assist-with-strike-selection/

Alan

Good morning, Alan –

A quick question: In order to avoid “weekend surprises”, do you enter a monthly trade on expiration Friday or do you wait until the following Monday?

Thanks –

-JEFF

Jeff,

Excellent observation. Unless we are “rolling options” prior to expiration of near-month contracts, it is best to wait until Monday to establish new positions. This has to do with the nature of Theta (time value erosion) which starts off slowly and therefore the time value loss of our premiums, if waiting from Friday to Monday, is negligible. Also, market-makers usually account for the weekend calendar days relating to Theta on Thursday or Friday before the weekend.

As you stated in your question, by waiting to Monday we avoid weekend risk.

Alan

Some observations:

What a crazy market. That’s twice this year where I have been surprised with price gyrations within 2 days before Expiration Friday. There is no sure bet and it is a casino. But we can be ahead of the curve with this Covered call methodology and its management, I am finding out that after a successful performance for the last two years (16% and 24%), we can take a hit and then move on.

Roll downs:

It seems like the market knows when I do a roll down. I wait till the 2nd day of the 4th of 5th weeks in a cycle to make 3 roll downs that have been consistently consolidating at a level and then next day they start to move up. 3 of 4 ot them I was able to buy back on the market dips where the Buy to Close netted me a net gain. One security XES I did let it be assigned for this weekend so I invest the money elsewhere.

For future roll downs, I intend to wait for the Friday 7 days before expiration to make a decision, since I found out, if the Last Price is near the strike, there can be some value in making the roll down.

FIVE:

This is an interesting stock. I purchased on 12/11/18 and rolled it twice and finally let it be assigned on 3/16/18 in 3 accounts with an 8.74% gain. Earnings on 3/21 were positive and I re-purchased it on 4/5 at 72.22 with a strike of 75 OTM. The DOW swings had not effect on it. It peaked at 78.28 on 4/18, just 2 days before expiration. Would you believe it finished today with the market down 201.95 below the strike of 75 at 73.84 (Gain for cycle 3.42%). That’s fine with me as it saved me a lot of work to roll out to 80.

Will probably take a Wait and Sell stance when it peaks back up since an 80 strike for Monday currently (Expiration 5/18) is only paying 0.60 at 73.84 which is a local return 0.8% (.6/73.84) or 0.83% with my position Return cost basis of 72.12.

Mario