Portfolio overwriting is a form of covered call writing where share retention, capital preservation and generation of modest cash flow are specified goals. We are looking to generate an additional option premium income stream while retaining the underlying shares. The risk of exercise and sale of our shares will always be present, but we can craft our trades in such a manner that the risk becomes much less than 1%.

What is standard deviation (SD)?

This is a measure of the range in a data set showing how far, on average, data points move from the data’s mean average.

What is 1 SD as it relates to implied volatility (IV) & stock price movement?

This quantifies the market expectation of a stock’s price movement over 1 year, falling into that range 68% of the time. Let’s say a stock is trading at $100.00 and its at-the-money (ATM) IV is 25%, we expect price movement to fall into the $75.00 – $125.00 range 68% of the time. We can take advantage of SD IV to assist in selecting strike prices based on our strategy goals.

How does 1 SD IV apply to Portfolio Overwriting?

Since we don’t want our shares sold, we select strikes so high that the probability of exercise is extremely low. BCI has developed a calculator (BCI Expected Price Movement Calculator) that has a conversion formula inherent in the spreadsheet that will convert the annual IV to one specific for the contract we are considering and offer a trading range based on 1 SD IV. Since the data will fall outside that range 32% of the time, our concern is only the 16% at the upper end of the range. Bottom line: When using 1 SD IV, the risk of exercise factor is approximately 16% (1/2 32%).

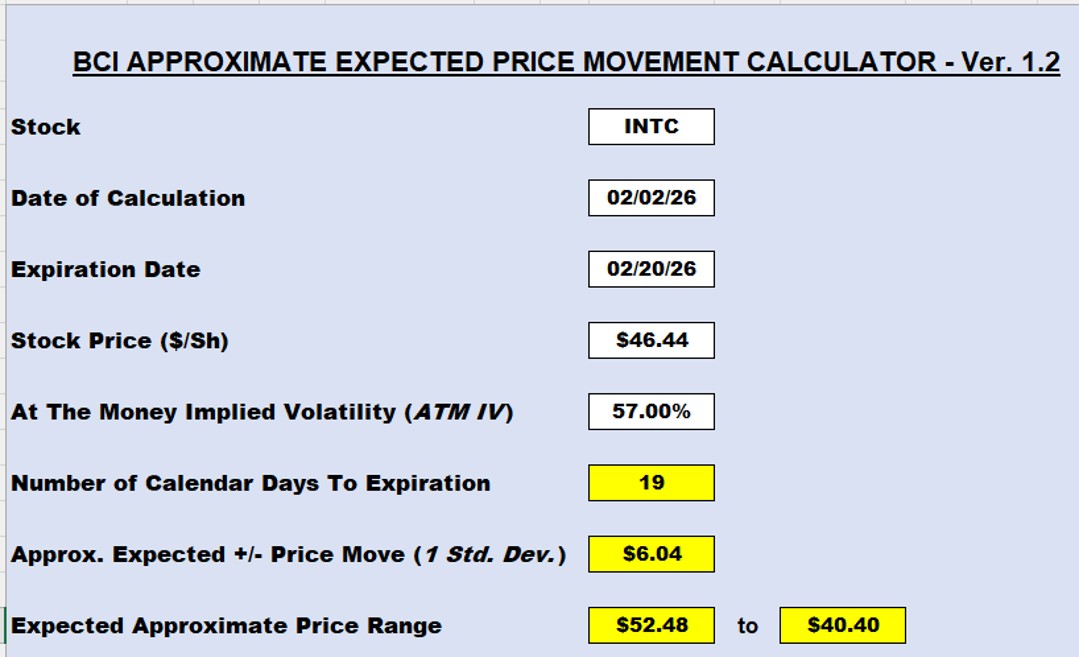

Real-life example with Intel Corp. (Nasdaq: INTC) using the BCI Expected Price Movement Calculator (ATM IV = 74%)

- Data entry in the white cells

- 74% IV is for 1 year; the spreadsheet has a conversion for this 33-day trade

- Based on 1 SD, INTC is expected to move up or down by $7.88 (above red oval)

- We would consider a strike $43.00 or higher for a 16% risk of exercise factor and this does not include our ability to buy back the option prior to contract expiration, making the practical risk <1%

Can we use 2 SDs and how is that calculated?

2 SDs is simply double 1 SD. In this case, INTC is expected to move up or down by $15.76 (2x $7.88) 95% of the time. Based on 2 SDs, we would select strikes above $50.00. The risk of exercise is 1/2 5% = 2/1/2%, w/o exit strategies.

Can we make any significant returns using 1- and 2 SDs?

INTC had an extremely high IV at the time I was writing this article. Lower IVs would generate lower returns, but let’s move on with the calculations. The $43.00 strike (1 SD) shows a bid price of $1.37, and the $50.00 strike (2 SDs) has a bid price of $0.69.

1- & 2-SD calculations using the BCI Trade Management Calculator

- 1 SD: The $43.00 OTM strike returns 3.87% in 33 days, 42.81% annualized (brown cells). There is also 21.47% upside potential (purple cell) if INTC moves up to or beyond the $43.00 strike.

- 2 SD: The $50.00 OTM strike returns 1.95% in 33 days, 21.56% annualized (pink cells). There is also 41.24% upside potential (blue cell) if INTC moves up to or beyond the $50.00 strike.

Discussion

2 SD IVs can be used for portfolio overwriting, particularly for high IV options. The approximate risk of exercise is 2.5%. With exit strategies it becomes < 1%.

EXPECTED PRICE MOVEMENT CALCULATOR

The Expected Price Movement Calculator is designed to generate an approximate projected trading range for the underlying security, specific for selected contract expiration dates. The at-the-money implied volatility (IV) of the stock or ETF (exchange-traded fund) is used to achieve this valuable information.

Click here for a video to learn more.

Free training resources

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to publish several of these testimonials in our blog articles. We will never use a last name unless given permission:

1. Las Vegas Money Show- 2 presentations

February 23 – 25, 2026

The Collar Strategy: Covered Call Writing with Protective Puts

Protecting covered call trades from catastrophic share loss

This is the strategy Bernie Madoff pretended to use. He called it the split strike conversion strategy, but it was simply a collar. The covered call sets a ceiling on the trade and the protective put guarantees a floor on the trade

Topics discussed

- What is the collar strategy?

- Uses for the collar

- Entering a collar trade

- Option basics for calls

- Option basics for puts

- Real-life example with NVDA

- What is an option-chain?

- Real-life example using the BCI Trade Management Calculator (TMC)

- Strategy pros & cons

- Educational products & discount coupon

- Q&A

Selling Cash-Secured Puts to Buy a Stock at a Discount or to Enter a Covered Call Trade

2 outcomes & 4 applications

Selling cash-secured puts is a low-risk option-selling strategy which generates weekly or monthly cash-flow. This presentation will detail how to craft the strategy to generate cash flow, buy a stock at a discounted price or to initiate a covered call trade. Topics included in the webinar include:

- Option basics

- The 3-required skills

- 4-practical applications

- Traditional put-selling

- PCP (Put-Call-Put or wheel) Strategy

- Buy a stock at a discount instead of setting a limit order

Real-life examples along with rules, guidelines and calculations are included in this presentation.

Time, date & registration link.

2. Palm Beach Traders Club

March 10, 2026

6:30 PM – 8 Pm ET

Private Investment Club / guests are welcome (free)

Wine-tasting event follows for those interested.

3. Long Island Stock Investors Meetup Group: Part II

Thursday March12, 2026

7:30 PM ET – 9:00 PM ET

Ultra-Low-Risk Approaches to Covered Call Writing & Selling Cash-Secured Puts

Introducing Our Latest Products, Creating New Investment Opportunities

4. Hollywood Florida Money Show

April 10, 2026

11:40 AM – 12:25 PM

The Put-Call-Put (PCP) or Wheel Strategy

Using Both Covered Call Writing and Put-Selling to Generate Monthly Cash Flow

Selling stock options is a proven way to lower our cost-basis and beat the market on a consistent basis. Two such low-risk strategies are covered call writing and selling cash-secured puts. This presentation will detail how to incorporate both strategies into one multi-tiered option-selling strategy where we either generate cash-flow or buy a stock at a discount. I refer to this as the Put-Call-Put (PCP) Strategy, also referred to as the wheel strategy.

The basics and pros and cons of low-risk option-selling strategies will be discussed as well as an analysis of a real-life example and introduction into the BCI Trade Management Calculator (TMC). This seminar is appropriate for those who look to generate modest, but consistent, returns which will enable us to potentially beat the market on a consistent basis while focusing on capital preservation.

More details to follow.

5. Young Investor’s Club at The University of Central Florida

April 16, 2026

Private student investment club.

6. Sarasota Investment Group

Portfolio Overwriting: A Form of Covered Call Writing

Wednesday April 22, 2026

Details to follow.

7. BCI Educational Webinar #10: The Put-Call-Put (PCP) or “Wheel Strategy”

Thursday May 14, 2026, at 8 PM ET

Using both covered call writing & cash-secured puts in a multi-tiered option selling strategy. A 68-day real-life example taken from one of Alan’s portfolios will be analyzed.

BONUS: Barry will share a real-life credit spread trade using our BCI Conservative Credit Spread Management System.

Discount coupons and a live Q&A session will follow the presentation.

8. Orlando Money Show

October 5 – 7, 2026

Details to follow.

Premium Members,

This week’s Weekly Stock Screen and Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 02/20/26.

Be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them on The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

https://www.youtube.com/user/BlueCollarInvestor

Barry and The Blue Collar Investor Team

Hi, Alan.

I sold a 1-week cash-secured put on MRK and would appreciate your thoughts on managing it.

• Ticker: MRK

• Trade entry: 2/23/26

• Expiration: 2/27/26

• Share price at entry: 123.22

• Strike: 120 (OTM)

• Premium: 0.53

• Break-even: 119.47

• 3% exit guideline: 116.40

One day before expiration, price is 119.69 (it was around 119.30 earlier today), the stock is still outperforming the market on a monthly basis (see image), and I do not see any negative news.

For a short-term weekly cash-secured put like this, how would you apply your 3% guideline (if at all), and how strictly would you adhere to it as expiration approaches?

William,

The 3% guideline (not a rule, a guideline) is in place to avoid substantial loss when share price turns against us.

Now, if an option is about to expire ITM, and we don’t want to take possession of the shares, we turn to a different exit strategy … rolling the option or just closing the option if we don’t want to use that underlying in the next contract cycle.

In your MRK example, you may choose to “allow” exercise and then write a covered call (put-call-put or PCP or “wheel strategy).

Having an arsenal of exit strategy choices and executing them based on our goals, is one of the metrics that sets BCIs apart from everyone else.

Good question.

Alan

Premium members:

This week’s 5-page report of top-performing ETFs, along with our sample trade of the week, has been uploaded to your premium site. The Select Sector SPDR section is now crafted to align with our streamlined (CEO) approach to covered call writing. The report also lists Top-performing ETFs with Weekly options, mid-week market tone as well as the implied volatility of all eligible candidates.

We have also included a sample trade taken from one of our BCI watchlists.

Premium member video link:

https://youtu.be/EXMO-KwZuJs

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team