When we sell cash-secured puts, we are contractually obligated to buy shares at the strike price by the expiration date, should the option buyer decide to exercise that option. In the BCI methodology, we predominantly favor out-of-the-money (OTM) put strikes, agreeing to buy the shares at a lower price than current market value.

In bear market environments, we may favor deep OTM put strikes to enjoy the benefit of greater protection to the downside in return for lower option premiums. In this article, we will use one of the option Greeks, delta, to determine strike selection in these situations.

What is delta?

One of the 3 definitions of delta is the approximate probability of a strike expiring in-the-money (ITM) or with intrinsic-value. When this occurs, the option will (almost always) be exercised and shares will be put to the option-seller at the strike price (assuming no exit strategy integration). Typically (but, not always), put sellers want to avoid buying the shares, so delta will measure and quantify that risk. As we go deeper and deeper OTM (strikes much lower than current market value), the risk of exercise becomes less and less as do the option premiums. We must find a balance between risk and returns when establishing our trades.

Real-life example with Solaris Energy Infrastructure Inc. (NYSE: SEI)

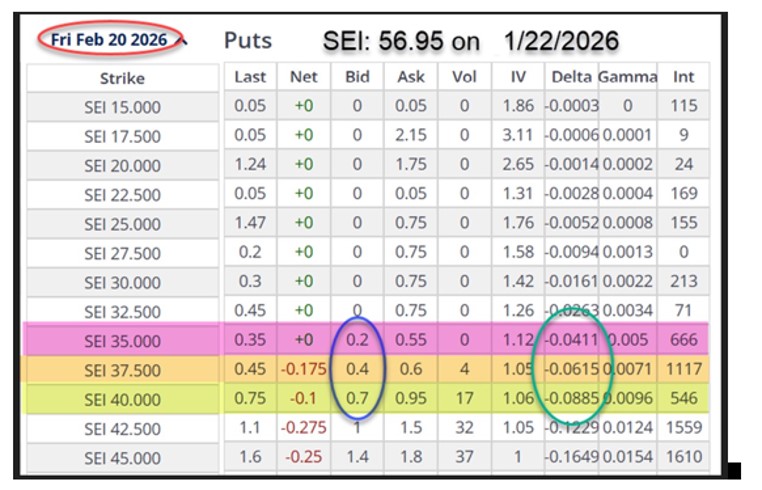

On 1/22/2026, SEI was trading at $56.95. Let’s review the put option chain and look for strikes with deltas < 10%. Note that deltas for puts show a minus (-) sign because put value is inversely related to share price movement.

SEI option chain on 1/22/2026 (SEI: $56.95)

- Red oval: Expiration date is 2/20/2026

- Pink row: $35.00 strike, delta = 4%, bid price = $0.20

- Brown row: $37.50 strike, delta = 6%, bid price = $0.40

- Yellow row: $40.00 strike, delta = 9%, bid price = $0.70

- Note that the lower the risk of exercise (delta), the lower the premium returns

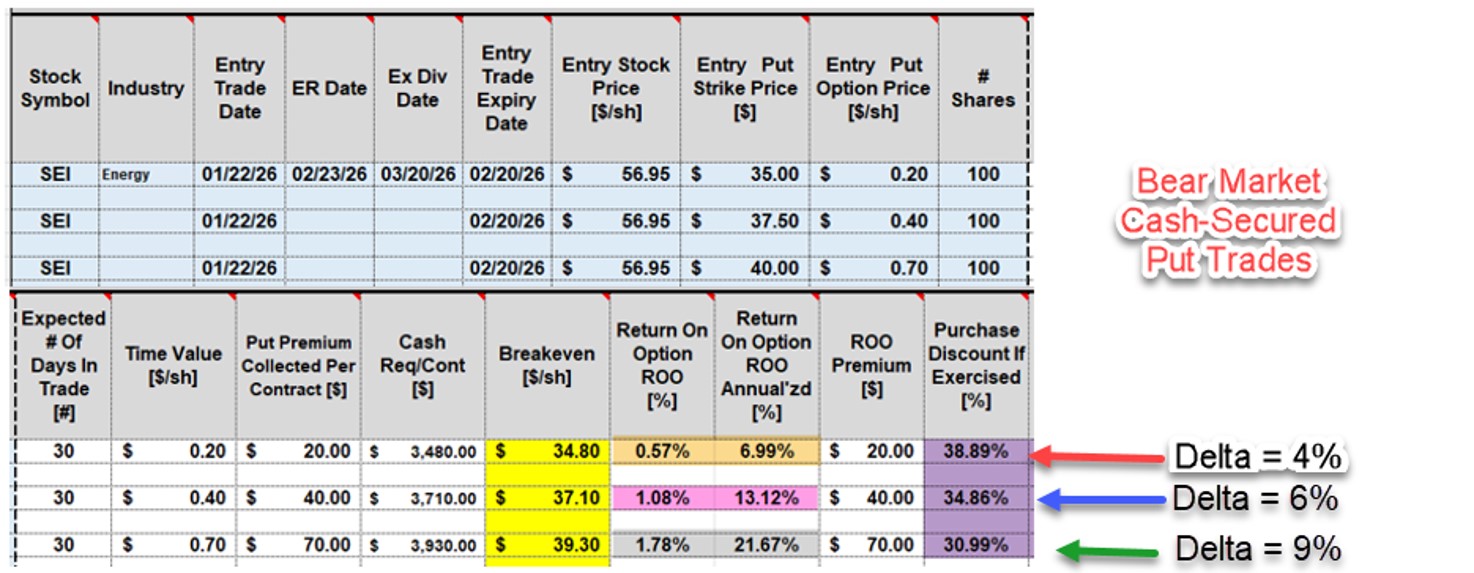

- Let’s calculate the % returns using the BCI Trade Management Calculator (TMC), so we can weigh the risk against the returns

SEI Initial put calculations for the 3 deep OTM strikes

- Red arrow: The $35.00 strike has a delta of 4% and an annualized return of 6.99% (brown cells)

- Blue arrow: The $37.50 strike has a delta of 6% and an annualized return of 13.12% (pink cells)

- Green arrow: The $40.00 strike has a delta of 9% and an annualized return of 21.67% (gray cells)

- The % purchase discount if shares are assigned as a result of exercise (share price moves below the deep OTM strike) ranges from 30.99% to 38.89% (purple cells)

Discussion

In bear markets, we may favor deep OTM put strikes to create greater protection to the downside. Delta is a useful metric that can be implemented to quantify the risk of exercise of the available strikes. We balance risk of exercise with premium returns to guide us to the most appropriate put strikes.

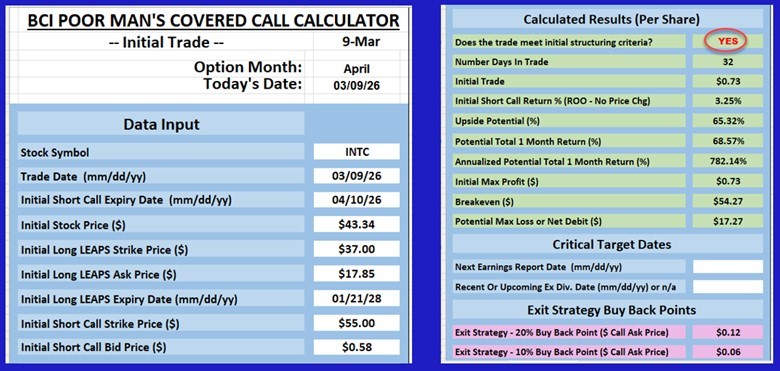

Poor Man’s Covered Call Calculator

The PMCC Calculator is designed to determine initial trade structure and status as well as various position management price point considerations the exit strategy price buyback points to buy back the short calls based on the 20%/10% guidelines detailed in the BCI books and DVD Programs.

For an informational video and more details, click here.

Free training resources

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to publish several of these testimonials in our blog articles. We will never use a last name unless given permission:

New Quasar Markets interview:

1. Mad Hedge Investor Summit

June 3, 2026

12 PM ET – 1 PM ET

Covered Call Writing

Uncovering a 3rd Income Stream in Our Investment Portfolios

Increasing profits and avoiding tax issues using stock options

You have owned shares of stock in your non-sheltered accounts for many years. Share value has been appreciated significantly over time. This has put a smile on your face. Many of these securities have also generated dividend income. This, too, has pleased you. However, there is a 3rd income stream that you can activate right now, leveraging these same stocks, using a strategy known as covered call writing.

This is a low-risk option selling strategy analogous to generating rental income with a real estate investment property. Yes, renting out your stocks for limited periods. We have 2 goals: generate a 3rd income stream + retain the underlying shares to avoid negative capital gains issues.

This presentation will analyze how to implement this form of covered call writing, known as Portfolio Overwriting, always with capital preservation in mind.

2. American Association of Individual Investors: NYC Chapter

Date and time to be confirmed.

Via Zoom.

More information to come.

3. MoneyShow Masters Symposium Las Vegas

July 20 – 22, 2026

Caesars Palace Hotel

Las Vegas

Details to follow.

4. Toronto Money Show

September 24 – 25, 2026

MaRS Center, Toronto Canada

5. Orlando Money Show

October 5 – 7, 2026

Hilton Orlando Lake Buena Vista

Details to follow.

6. Triple Edge Investing Summit: Technical Analysis • Options Strategies • ETF Mastery

Saturday January 23, 2027

Zoom presentation

Paid event

All-day event hosted by 3 experts:

- Dr. Alan Ellman (options)

- Dr. Eric Wish (technical analysis)

- Les Masonson (ETFs)

Hosted by TraderLion University

Details to follow.

Premium Members,

This week’s Weekly Stock Screen and Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 05/29/26.

Be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them on The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

https://www.youtube.com/user/BlueCollarInvestor

Barry and The Blue Collar Investor Team

Premium Members:

1. This week’s ETF Report has been uploaded to your member site. Login to the member site and scroll down on the left side to access the report.

ETF Report Video Link:

Explanation of the report format:

https://youtu.be/addf7Y54ixwput

2. I’ve attached to premium member emails a 5-contract, 5-day cash-secured put trade with SMCI, an elite-performing stock at the time of the trade. I executed this trade on 6/1/2026, for the 6/5/2026 expiration. SMCI closed at $47.42 today, down $0.40 from trade entry. The current price is above the OTM $40 strike by $7.42and breakeven by $7.58. As always, I remain prepared to execute exit strategies, if those opportunities arise. Despite today’s share price decline, there is still decent protection to the downside.

3. Our loyalty pledge to you: Premium members will NEVER experience a rate hike as long as premium member subscriptions remains active … NEVER.

4. New Quasar markets interview:

(21) Quasar Markets on X: “QM Live w/ Dr. Alan Ellman https://t.co/sS9ibZhrJ3” / X

Wishing you the best results,

Alan & the BCI team