One of the covered call writing exit strategies in our arsenal as expiration approaches is rolling in-the-money strikes out-and-up. This involves buying back the near-month strike and selling a higher strike in the next contract period. Since there is an intrinsic-value component to the cost-to-close, we must add additional cash to the position in order to execute this transaction.

Hypothetical example

- Buy 100 x XYZ at $80.00

- STO $100.00 call at $3.00

- At expiration, XYZ is trading at $120.00

- BTC the $100.00 call at $20.10 ($20.00 intrinsic-value)

- STO the next month $140.00 call at $3.00

Time-value credit aside, we had to add $2000.00 per-contract to keep the trade viable. The good news is that we now have a stock worth $20.00 more (unrealized share value gain) than the previous strike would allow. However, additional cash is required to execute this rolling-out-and-up trade.

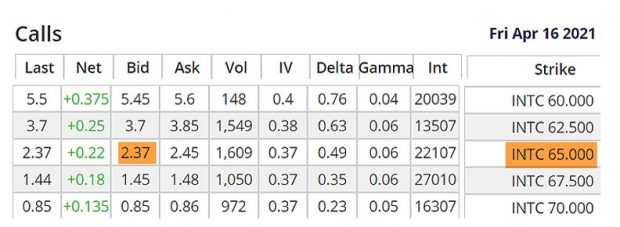

Real-life example with Intel Corp.(NASDAQ: INTC) on 3/19/2021 with INTC trading at $64.50

- 3/19/2021: BTC the $60.00 call at $4.55 ($4.50 is intrinsic-value)

- 3/19/2021: STO the 4/16/2021 $65.00 call at $2.37

- Rolling time-value credit: $2.37 – $0.05 = $2.32 per-share = 3.87%

- Cash required to add to trade negated by increase in share value = $450.00 per-contract

Option-chains

INTC Option-Chain to Close March Contract

INTC: Option-Chain to STO the April Contracts

Discussion

Rolling an in-the-money covered call out-and-up will result in a time-value credit. However, to accomplish this, additional cash will need to be added to the trade in the form of intrinsic-value. This additional cash is neutralized (at the time of the trade) by the increase in share value from the original strike price to the lower of the current market value or the new strike.

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to share some of these testimonials in our blog articles. We will never use a last name unless given permission:

Hi Alan,

At our recent Money Show event, yours was the highest attended course of the event and we had lots of interaction. The viewers had only great things to say. So, thank you.

The Money Show Team

Upcoming events

1- BCI-Only Webinar: Free Webinar Covered Call Writing and Selling Cash-Secured Puts

Covered Call Writing and Selling Cash-Secured Puts: 2 New Strategies Developed by BCI

The VOLQ-covered call strategy and Weekly 10-Delta Put-Selling strategy

August 19, 2021 (Thursday)

8 PM – 9:30 PM ET

- A link will be posted on the BCI site and emailed to all those on our mailing list as the event approaches

- No pre-registration needed

- Our platform allows the first 500 attendees to access the webinar

To join our mailing list and receive our free newsletter go to our blog page

Subscribe to our Mailing List here

2- Mad Hedge Traders and Investors Summit: Free webinar

September 14- 16, 2021

Information and registration link to follow.

***********************************************************************************************************************

Market tone data is now located on page 1 of our premium member stock reports and page 1 of our mid-week ETF reports.

****************************************************************************************************************

Alan,

When you establish a collar, can you adjust the call or the put during the contract period up or down depending on your strategy? I have not found any material regarding my question in your books as yet.

Also, it would be helpful if there was a way the daily put’s could be entered into the same Daily Covered Call Check Up spreadsheet since it appears that they both use the 20/10 rules.

Thank you for your assistance with this questions.

Craig

Craig,

We are in the process of developing a trading log for both covered call writing and put-selling (one spreadsheet fort both strategies) which will incorporate all exit strategies allowing us to monitor our trades start-to-finish.

That said, the active leg of the collar trade is the short call so view it as covered call writing with an “insurance policy” to mitigate catastrophic share gap-down. When using our collar calculator, we can adjust the net call premium as we buy-back and re-sell call options. At the conclusion of the trade, put and share results can be incorporated into final results… if we sell the put, enter the net put credit or debit and if we sell the stock, we have a known credit or debit.

Stay tuned for our new trading log. We believe it will be the only product of its kind.

Alan

Hi Alan,

I am a new Premium member and am trying to do my first Covered call.

I have purchased 100 shares of SJR Shaw Communications as per your weekly sheet. I purchased them for $29.05

I have had a look on Yahoo at selling the Call at $30 and the Bid is zero premium?

Is this correct? Or is this because the Stock exchange is closed over the weekends?

Regards,

Todd

Todd,

Re-check the bid-ask spread on Monday between 11 AM and 3 PM ET to get a more reliable quote. SJR is a low-volatility security so premiums will reflect that low volatility. I would expect that with nearly 200 contracts of open interest, there will be an opportunity to generate some meaningful cash-flow.

Alan

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 07/30/21.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them on The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

On the front page of the Weekly Stock Report, we now display the Top Performing ETFs, the Top SPDR Sector Funds, and the 4 single Inverse Index Funds. They are sorted using the 1-month performances from the Wednesday night ETF report and the prices from the weekend close.

Please make sure that you review the new feature that we’ve added…Implied Volatility or IV. This is the At The Money (ATM) Implied Volatility for all of the stocks in the report.

Since we are now in Earnings Season, be sure to read Alan’s article, “Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The Blue Collar Investor Team

barry@thebluecollarinvestor.com

I was burned bad by the Boeing gap down due to holding it in margin. I had 200 shares, 100 purchased at 225, and the next 100 purchased at 240.

For the 225 holdings I sold ATM and rolled up to 232.50 for roughly 1200 dollars in premiums over the course of two months.

For the 240 holdings, I sold ATM for Aug 20, around 600 in premiums.

The decline triggered a maintenance call and I unwound the 240 shares at 220, losing roughly 1500 dollars in the process.

For the remaining 100, I covered an august 27 call at 235 strike and rolled it to Jan ’22 at 250 for a net premium of around 800 dollars in addition to marginal gains from previous contract sales that I negated with gambles in purchased calls. My break-even is now 224$ !

I am very frustrated with myself in part for being too cavalier with margin but also for reacting hastily without any clear strategy for my position management – I’m now locked in for 5 months in a volatile stock that might undergo a downturn due to delta variant and future earnings.

So far, my assessment of the trades are that:

1. Margin is very dangerous and I should not use as much of it as I did

2. I should consider writing ITM only for margin and possibly also use collars as a rule

3. Avoid the tendency to be stubborn, seeking a home run with my stock choice; I did cover the 240 call when Boeing was at around 230 with the objective of waiting for a rally that did not materialize(that happened at 205$); I could’ve sold a near-term deep ITM call (200$) to blunt the loss that I was forced to realize. Overall, I consider this to be a busted trade

Short of rolling down significantly or a full unwind,, I’ll probably need to buy protective puts over the next 5 months. I am curious if there’s a least-painful way to accomplish that; Perhaps I could buy two weeks out and roll every Friday? Buy a month, two months out? Bite the bullet and buy a jan ’22 put? Very frustrated! thanks

Robert,

I will respond in general terms without offering specific financial advice.

When a stock price movement disappoints, we ask ourselves this question: ” Are the fundamental, technical and common-sense requirements still in place that led us to selecting this security? If yes, we continue to manage our positions. The 20%/10% guideline BTC limit orders are critical.

If no, we take our loss, learn valuable lessons from our trades and enter new positions with different underlyings. It’s important to remember that we have no loyalty to the stock but a great affinity to the cash it represents… where is that cash best placed to increase the chances of the greatest returns?

Some additional comments:

1. I agree with your assessment that margin could be dangerous and therefore (my opinion) not appropriate for most (okay for some) retail investors.

2. ITM calls and collars are excellent defensive plays in all scenarios when markets are bearish or volatile. They can also be used if they align with our personal risk-tolerance and helps us sleep better at night. Margin has little to do with these approaches.

3. Rolling-out 6 months is tempting because it will generate large premiums. There are negatives to this approach:

– Longer-term options generate lower “annualized” returns.

– Longer-term options bring us through multiple risky earnings-reports.

– Longer-term options decrease the frequency with which we can re-evaluate our bullish assumptions of the underlying.

In my humble opinion, there are more negatives than positives with longer-term options.

The key question we must ask ourselves is where should we place the cash remaining in this trade… in the current underlying or a new one?

When I have a losing trade, I view it as a positive if I can learn from it and it makes be a better investor.

Alan

Premium Members,

There was a typo in the ER Date for NVDA in the report uploaded last night. The correct ER date is 08/18/21 vs, what the report is currently showing, Tom B., thank you for spotting the typo.

Best,

Barry and The Blue Collar Investor Team

Alan:

Your discussion today regarding adding cash to a position when rolling Covered Calls Out & Up was of particular interest to me, as I hold a substantial portion of my equity holdings in essentially a Buy & Hold (Overwriting) Portfolio, & as a result, I employ a Roll Out & Up exit strategy at times to avoid unwanted assignment.

I understand the concept of “buying-up” the value of the underlying involved, & your book on Exit Strategies covers the subject & the mathematics involved well. But my comment involves treatment of the cash so added in the transaction.

If the underlying involved were held in a buy & hold portfolio, & no option positions were involved, the investor would still get the increase in value resulting from price appreciation with no contribution of additional cash. Therefore, would it not be accurate to consider the cost of the additional cash added when selling Covered Calls as a net cost of so doing vs. simple buy/ hold investing?

Regards,

Paul

Paul,

There are 2 perspectives regarding the additional cash added to the trade as discussed in this blog article:

1. From the perspective of covered call writing, the strategy we are using.

2. From the perspective of ” had we used a different strategy”, simply buying and selling stock, in your inquiry.

Let’s start with the second… it is true that had we not put a cap on share appreciation by selling the covered call option, we would benefit from share appreciation without adding additional cash to the trade… agreed.

However, the strategy we are using is covered call writing and when we buy-to-close the ITM short call, we are paying a large (percentile) intrinsic-value price… it is a debit into our account. Since we recognize this debit, we must also account for the unrealized benefit gained from closing the original short call in the form of “buying-up” share value. It is absolutely essential to recognize this fact when evaluating our exit strategy arsenal.

For those of us using portfolio overwriting, we use deep OTM strikes to allow for significant share appreciation and mitigate the need to roll ITM strikes at expiration as well as decrease the probability of assignment. These trades must be managed differently than conventional covered call writing.

To sum up: When deciding on a strategy, we must recognize the pros and cons of that investing approach. Since I know you to be a sophisticated investor who always does your due-diligence, I’m sure that has been accomplished. We’re now on a train that left the “had we used another strategy” station several stops ago.

Alan

Hi Alan,

I hope to find you well. I sell ITM covered call on growth stocks and average down sometimes depending on the drop in share price and the timing of the drop in share price.

For example,

I bought 1000 CRSR Shares at 29.06 and sold covered call simultaneously at 27.50 expiring August 20th while collecting total premium of $3. I understand the 1.56 is intrinsic value. However if the stock drops to 27 in near term what are your thoughts on averaging down and essentially eating away most of the $1.56 of intrinsic value. This would mean the entire $3 as premium and roi would more than double. I would hold on to the new batch of shares bought at 27 to average down or sell into September otm call at 30.

Your guidance on this will be much appreciated.

Thanks,

Saadi

Saadi,

When share price declines, our focus is on the stock and the reason for the downturn rather than on the option premium. We ask ourselves if the reasons we chose this security (fundamental, technical and common-sense) are still in place. If yes, we manage as per our exit strategy arsenal. If not, we close and move the cash into another, better-performing security.

Analyzing CRSR and the initial trade structuring, we generate a 5.2% 1-month initial time-value return with 5.4% downside protection of that time-value profit. Such substantial returns translates into a high implied-volatility underlying with potential for dramatic price movement in either direction. There is nothing wrong with this as long as this trade aligns with our personal risk-tolerance and target goals. Let’s say it does.

After entering the trade, we set our 20% buy-to-close limit order at $0.60 (20% of $3.00). If and if and when the threshold is reached, we decide on the next step based on our strategy methodology.

To your question regarding averaging-down if share price declines significantly. Do we want to add additional cash to a losing trade? If we do add additional cash, why not select a better-performer? We must focus on what is important to us… the cash, not the stock. I avoid averaging-down in my portfolios.

Alan

Premium members:

This week’s 4-page report of top-performing ETFs and analysis of the top-performing Select Sector SPDRs has been uploaded to your premium site. One and three-month analysis are included in the report. Weekly performance has also been incorporated into the report although not part of the screening process. Weekly option availability and implied volatility stats are also incorporated.

The mid-week market tone is located on page 1 of the report.

New members check out our ongoing and never-ending training videos (“Ask Alan” and Blue Hour webinars). We add at least one new video each month. Only premium members have access to the entire library of these training tools.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

Hi Alan

Trust you’ve been keeping well. Thanks again for your great education.

I have a query around playing the bid-ask spread. In either a blog or video, you mentioned it was easier to do when legging-in but that it was possible when using a Buy Write Order which is what I use. Please would you expand on that.

Also, the new column on the premium report ‘Aprx Curr ATM IV%’, please would you explain how to incorporate this information into the process of selecting the best stocks for the contract month. Does the higher number mean that the returns are likely to be out of the 2 – 4% guideline and if so, is there a guide as to what this number is around?

I have been paper trading for the last 3 – 4 months and am gaining more confidence as I try to marry the doing with the theory/information you provide.

Much appreciate your time in answering my questions and thanks again.

Regards

Shirley

Shirley,

Your due-diligence is impressive.

With buy-write orders, we can incorporate the adjusted option limit order into the net debit limit order. As an example, if a stock is trading at $29.00 and the option bid price is $1.00, the buy-write net debit limit order is $28.00. Let’s say, we want yo use $1.20 on the option sale based on a wide spread… we enter a net debit limit order of $27.80. Market-makers are not subject to the “Show or Fill Rule” when entering an order tied to multiple exchanges so greater success is realized when legging-in.

The new column we added to our premium stock reports can be used to establish a projected trading range. Here is an article I published on this topic:

https://www.thebluecollarinvestor.com/using-the-nasdaq-100-volatility-index-volq-in-covered-call-writing-decisions-a-real-life-example-with-invesco-qqq-trust-nasdaq-qqq/

I will be writing more on this topic as the member feedback has been impressive. We will also be adding a trading range calculator based on the formulas shown in the article.

A high IV does mean greater premiums and higher risk but we can manage the risk. We can also stay in the 2% – 4% range by using deeper ITM or OTM strikes on high-IV securities.

Keep up the great work.

Alan

Hi Alan,

I had a problem using the limit of 20% on AMD, because of VIX it’s IV was in the 40’s . Any advice will be appreciated.

Richard

Richard,

The 20% guideline for calls is based on the initial option premium received, not on the security’s implied volatility.

If we sold the option for $2.00, we set a buy-to-close limit order at $0.40 (20% of $2.00) in the first half of a monthly contract. We change to 10% ($0.20) in the latter half of the contract. This applies to securities of all implied volatility stats.

Alan

Alan,

SFIX sewed me a straight jacket yesterday. So, I decided to get back into the game and start selling CSPs again.

On 7/21/21, I entered 5 CSP trades, four of which I exited on 7/27/21 when the market crashed unexpectedly. I decided to stay in SFIX because the fundamentals were good, chart was moderately ok with a MACD on the upswing, and no earnings report within the life of the option.

The SFIX trade I entered was the August 13th 52 put for a premium of $1.21. Everything was fine, with absolutely no news, no negative corporate actions or any other catalyst and then BAM….yesterday it cratered by 10%.

The only thing that makes me ok with this is that I had set an alert that told me when the price per share hits 3% below the strike price. Without hesitation or trying to rationalize staying in the trade (we’ve all done this…admit it…you hesitate to exit the trade because you think it’s going to bounce right back after you get out), I adhered strictly to the rule and bought back the put. It was hard, but I am glad I did because it continued to crater in a massive way.

Will I quit because I’m discouraged? No, because I am confident that moving forward, so long as I follow the rules of the strategies, I will statistically speaking be profitable over time.

Joanna

Joanna,

Having a structured plan for trade management as well as trade entry will keep us protected against emotional trading which is a major hurdle for most retail investors,

Well done.

Alan

Hi Alan,

This if Guerry we’ve emailed in the past. I’m a new premium subscriber and I have an idea that I want to run by you.

I’ve created my own spreadsheet to track my positions daily. One column that I’ve added is the “Current Exit Amount”. It’s the net profit to get out of the option and stock positions. I’ve set up conditional formatting on the “Current Exit Amount” field to change the fill color to light green when the amount is greater than the initial premium when I sold the option.

This situation occurred for me yesterday on 200 shares of CLOU that I owned. I was able to get of of the position for a profit of $117 versus the $100 premium from the initial sell of the 2 option contracts. That freed up some capital buy another stock and sell the August option on.

Do you think this is a valid exit strategy to use?

Hope you have a great day.

Thanks,

Guerry

Guerry,

I love the concept of creating a second income stream when share price accelerates and we have generated both option premium plus share appreciation. We are definitely on the same page here.

We actually have this covered in the “mid-contract unwind” exit strategy, an integral part of our BCI methodology. See the exit strategy chapters in both versions of “The Complete Encyclopedia for Covered Call Writing” for several real-life examples as well as those in our covered call writing online video program.

The key to maximizing our returns when these opportunities arise is to measure the time-value cost-to-close the original position against the amount of potential profit we can realize from position #2. We like to see at least a 1% or higher initial time-value return over the time-value cost-to-close position #1. As an example, if the time-value CTC is 0.5%, we want to see at least a potential 1.5% initial time-value return for trade #2.

Use the “What Now” tabs of the Elite or Elite-Plus Calculators to generate these statistics.

Keep up the good work.

Alan

Hi Alan,

Love your content as always and looking forward to your webinar on 19th August.

I learned a lesson about writing calls before special dividends yesterday. As you will know, OMF paid $0.70 regular dividend and a $3.50 ‘special’ dividend yesterday. I wrote the slightly OTM $61.50 Aug20 call on Wednesday, one day prior to the stock going ex-dividend. I felt that writing an OTM call with 16 days to expiration would be a low risk of early assignment.

To my surprise, the call strike changed down to $58 today – a change of $3.50 in line with the amount of the special dividend. I unwound that position today at a small loss, but wiser for the experience!

My question: does this always happen when a SPECIAL dividend is paid? I haven’t noticed it for regular dividends. Is there anything on the options contract that indicates the strike price is subject to change?

Also, I note that you have an ‘Ask Alan’ video – no 36 – called Special Cash Dividends and Contract Adjustments. I tried to watch this yesterday but it doesn’t seem to be working. Many of the Ask Alan videos now show as private and I’m unable to view them.

Thanks as always.

Richard

Richard,

Your position did not change yesterday. The Options Clearing Corporation (OCC) makes sure that buyers and sellers of calls and puts are “made whole” when there a corporate event like a special dividend distribution. Quarterly dividends are baked into our option premiums but special 1-time dividends need special treatment.

On the ex-date, the holder of the shares (us) are entitled to the dividend distribution at a future date. At the same time, share value decreased by the special dividend amount, $3.50 in this case. To make option buyers and sellers whole, strikes are adjusted accordingly, down to $58.00 for OMF. At close yesterday, OMF was trading at $58.35. No harm, no foul… actually a favorable position.

This is standard operating procedure for 1-time special dividends.

We did have a technical issue with our “Ask Alan” videos yesterday and my tech team reported to me that all videos will be available to our premium members this morning.

Alan