Traditional covered call writing consists of buying a stock or exchange-traded fund (ETF) and selling a call option to generate cash flow. Frequently BCI members will think outside the box and add additional strategies and products to create a covered call writing-like strategy. The goal in these cases is not to complicate a realtively straightforward strategy but rather to generate even higher returns. Here is a strategy recently proposed to me that I thought you would find interesting:

The strategy involves the use of covered call writing, leveraged ETFs, weekly options and protective puts. Let’s first define the latter three terms.

Definitions

Leveraged ETFs: Exchange-traded funds that use financial derivatives (like options) and debt to magnify the returns of an underlying index.

Protective puts: A put option purchased for a stock already owned by the put buyer. It protects against a decrease in share price and ensures a minimum sale price of the stock.

Weekly options: Options which exist for eight days. They are introduced each Thursday and expire eight days later on Friday

TNA: This leveraged ETF seeks a return that is 300% the return of its benchmark index (small cap bull fund) for a single day. The fund should not be expected to provide three times the return of the benchmark’s cumulative return for periods greater than a day. By nature, these securities are highly volatile and generate higher option premiums.

The prosed trade

-

Buy 300 x TNA @ $52.70

-

Buy the 6-month $77.50 put option for $27.51 ( 3 contracts)

-

Total position cost = $80.21 x 300 = $24,063.00

-

Guaranteed sales price because of put option is $77.50/share, leaving a debit before cc writing of $2.71/share

Theory behind the trade

-

Sell weekly, slightly out-of-the-money call options on TNA making sure to generate at least $1 per share premium

-

Continue selling these options weekly for 26 weeks generating $7800 ($300 x 26)

-

By put expiration the shares are sold for $77.50 or $23,250.00

-

Total returns = $7800 + $23,250.00 = $31,050.00

-

Less cost basis of $24,063.00 = $6987 which represents a 29%, 6-month return

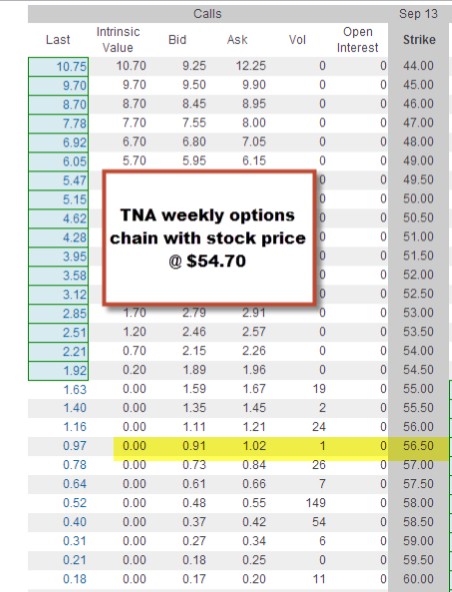

- Let’s look at a recent options chain for TNA to see the strike we would have to sell to generate a weekly return of $1:

TNA: recent options chain

To avoid assignment the stock cannot go higher than $56.50 to meet our weekly $1 (close to $1 in this case) requirement. Next let’s view a recent 1-month chart of this security to see how realistic avoiding assignment for 26 consecutive weeks is:

TNA: 1-month chart

TNA has traded in a $9 price range ($52 to $61) in the past month and so the expectation of assignment during that 26-week time frame is highly probable. To avoid assignment we can buy back the option but that is a debit not accounted for in the original trade proposal. If we allow assignment we would have to repurchase the security at a higher price also incurring an additional, unaccounted for debit.

Assumptions made and related concerns

For 26 consecutive weeks you will never be assigned on the short call. Herein lies the weakness of the strategy. We are dealing with a highly volatile, leveraged security which will generate high option returns but also put us at assignment risk. We are protected to the downside because of the put purchase but vulnerable to the upside.

Conclusion

Traditional covered call writing can be altered through the use of additional strategies like put buying and other option products like weekly options and leveraged ETFs. These strategies will have their advantages and disadvantages which must be fully understood before implementing them into your portfolios and risking your hard-earned money. Once all aspects of the multi-level strategy is understood, only you can determine if it’s right for you. The one rule of thumb you can always take to the bank is that there is no free lunch.

Next live seminar:

October 19th, Los Angeles, California:

http://www.aaii.com/chapters/meeting?mtg=2523&ChapterID=5

Market tone:

The self-imposed government crisis has kept the market nervous but holding up better than many experts expected. This week’s reports:

- Treasury Secretary Jack Lew said that October 17th was the last day that the US government could pay its bills without the debt ceiling being raised. Failure to do so could have a devastating impact on our economy and the world economy as well

- The monthly employment report was not released in full due to the partial government shutdown but did state that jobless claims were up by 1000

- The ISM Manufacturing Index rose to 56.2 beating estimates of 55

- The ISM Non-Manufacturing Index (service sector) disappointed at 54.4 below the level of 57.5 anticipated and the lowest level since November, 2008. This figure, however, still represents growth

- The ISM Employment Index rose to 55.4 from the August level of 53.3, the best level in 2013

For the week, the S&P 500 declined by 0.1%, for a year-to-date return of 21%, including dividends.

Summary:

IBD: Uptrend under pressure

BCI: This site remains moderately bullish on our economy but concerned about the ineptitude of our Congress. Therefore, we are taking a defensive posture and selling an equal number of in-the-money and out-of-the-money strikes.

Wishing you the best in investing from Paris, France,

Alan (alan@thebluecollarinvestor.com)

www.thebluecollarinvestor.com

Premium Members,

The Weekly Report for 10-04-13 has been uploaded to the Premium Member website and is available for download.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the BCI YouTube Channel link is:

http://www.youtube.com/user/BlueCollarInvestor

Best,

Barry and The BCI Team

Hi! Alan

Thanks for discussing my strategy.

You are right with the upside vulnerability, so I got a new idea.

Now I add an out of the money call to the weekly trade, so if TNA increase in price I participate also to he upside. Of course the purchase of the call must be less than the premium I got selling the TNA call.

If TNA goes south I can buy the covered call back and sell a new generating more premium, getting back the money I spent to acquire the out of the money call.

Alan, I got some questions they’re a bit late, but about the weekly options which sound quite lucrative, if I do ever feel good enough to use them.

– First if I decided to use weekly options then do all your exit strategies apply to these one week contracts too?

– If the exit strategies do apply, then how would I then use the 20% /10% rule in this case?

– If there is more monitoring needed(which I presume there is), then should I need an alert system for this?

– Also what type of chart or charts should I use for viewing?

Hope you can reply back. thanks

Fred,

The BCI team is working on incorporating weeklys into our methodology. The 20/10% guideline will not apply. Here are my intial conerns with the caveat that weeklys will be part of the methodology for those members interested (we do include a list of ETF with weeklys in our weekly ETF Reports):

1- The pool of stocks with weeklys is limited (although growing)

2- Less time for exit strategy execution

3- Quadruple the commissions

Stay tuned for more information on weeklys.

Alan

If weekly options do become part of the BCI system then I think I would definitely want to try this product type in the future. Hope more stocks become available for it first! thanks

Fred,

The trend is definitely for more and more stocks and ETFs with weeklys as the public is demanding these products. There has also been the introduction of “minis” for more expensive stocks like GOOG and AMZN where there are 10 instead of 100 underlying securities per contract. Stay tuned.

Alan

Good strategy Alan.

Thanks for publishing such a wonderful content on your website.

Just wanted to share my idea on the concerns you published:

On the upside, if the stock gets assigned. Buy TNA stock again and continue the strategy..

Won’t it work..I think it will work the way you described even after assignment or early assignment.

Sankar,

Yes, the strategy can be continued in this manner but our cost basis will increase. See my comments under the TNA chart:

“To avoid assignment we can buy back the option but that is a debit not accounted for in the original trade proposal. If we allow assignment we would have to repurchase the security at a higher price also incurring an additional, unaccounted for debit”.

Alan