Mastering both conservative option selling strategies, covered call writing and put-selling will allow us to maneuver our way through most market situations. This past Wednesday, May 27, 2015 several of the stocks on our BCI Premium Watch List gapped up. On last week’s blog commentary I addressed the situation with BRCM and AVGO and the merger rumors causing their meteoric price increases. Another gap-up occurred with Synaptics, Inc. (SYNA) as shown in the chart below:

SYNA gap-up on May 27, 2015

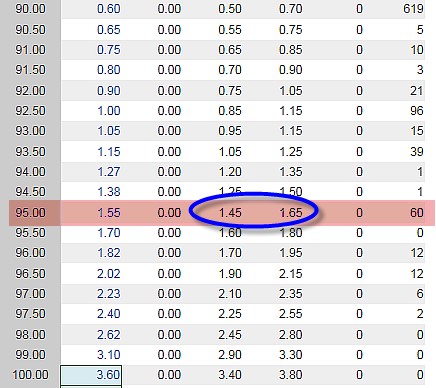

SYNA gapped up nearly $4.00 per share to $99.11. Was this an opportunity lost? Let’s assume for a moment that we planned to buy SYNA at the “pre-gap-up price” of $95.00. Now we have a dilemma because share price is so much higher. One way to deal with this situation is to use our put-selling skills. Below is a screenshot of a put options chain for SYNA pre-market on May 28, 2015:

Put option chain for SYNA on 5-28-15

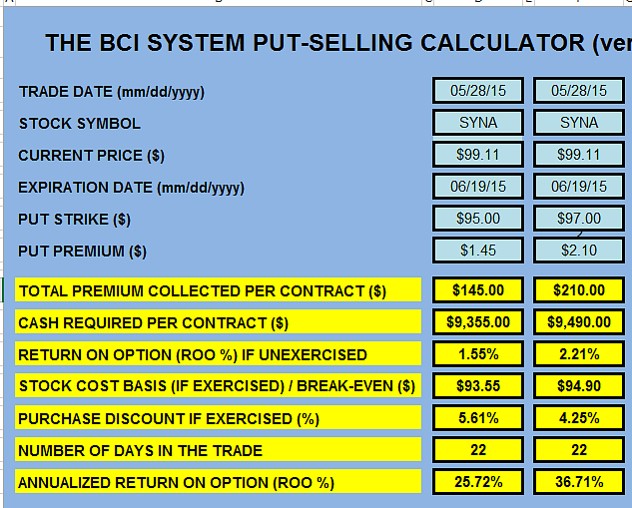

We can sell the $95.00 put for the published price of $1.45, and, if exercised, buy the shares at a cost basis of $93.55 or we can sell the $97.00 put for the published price of $2.10 and, if exercised, buy the shares at a cost basis of $94.90. The beauty of this approach is that if the options are not exercised, we have leveraged this security to generate a significant cash flow. Next, let’s feed the option chain information into the BCI Put Calculator:

Put calculations for SYNA

Note the following:

- If unexercised, the $95.00 put generates an annualized return of 25.72%

- If unexercised, the $97.00 put generates an annualized return of 36.71%

- If exercised, the $95.00 put results in a cost basis of $93.55, a 5.61% discount from current market value

- If exercised, the $97.00 put results in a cost basis of $94.90, a 4.25% discount from current market value

- For both puts, the cash required to secure those puts is slightly less than the cash required to buy 100 shares at $95.00

Discussion

Mastering the skills of covered call writing and selling cash-secured puts will allow us to deal with most market events like the gap-up of the price of a security we are interested in. By selling out-of-the-money cash-secured puts (strike price below current market value), we can craft our trade to buy the shares at the pre-gap-up price. If the trade is not executed, we still will have generated a significant cash flow. Another way to view this is that we either purchase the shares at our price or get paid not to buy that security.

***For a free copy of the single-column BCI Put Calculator click on the Free Resources link on the top black bar of this page. Both the single and triple column versions are available for free to Premium Members in the “resources/downloads” section of your premium site.

NEW ASK ALAN VIDEO FORMAT: SAMPLE PHOTO:

Coming soon: New Ask Alan video format

Market tone

Concerns over Greece’s potential exit from the eurozone weighed on markets. Adding to investor concerns was economic contraction in the US, Canada and Switzerland. This week’s reports:

- The US economy contracted in the first quarter by 0.7% annualized, revised down from the initial estimate of 0.2%. Key factors were the larger trade deficit, smaller inventory accumulation and weaker consumer spending than first estimated in addition to a harsh winter

- Pending home sales rose by 3.4% to a seasonally adjusted 112.4 in April 14% above the previous year and the highest level since May 2006

- Sales of new homes rose by 6.8% in April to a seasonally adjusted annual rate of 517,000

- US home prices continued to rise in March, according to the S&P/Case-Shiller Home Price Index. Over the 12 months ended in March, the national index increased by 4.1%

- Durable goods orders dropped by 0.5% in April after a revised 5.1% gain in March

- The US Conference Board’s index of consumer confidence rose to 95.4 in May from a downwardly revised 94.3 in April

- The University of Michigan’s consumer sentiment gauge rose to a final reading of 90.7 for May from 88.6 at midmonth

- Initial unemployment insurance claims rose 7,000 to 282,000 for the week ended May 23rd, the 12th consecutive week below 300,000

For the week, the S&P 500 declined by 1.1% for a year to date return of 2.3%.

Summary

IBD: Confirmed uptrend

GMI: 6/6- Buy signal since market close of May 11, 2015

BCI: Cautiously bullish favoring out-of-the money strikes 3-to-2

Wishing you the best in investing,

Alan (alan@thebluecollarinvestor.com)

Alan,

What formula do you use to get the purchase discount % in the calculator. Hope this question isn’t too basic.

Thank you.

Bonnie

Bonnie,

On this site there is no such thing as a question that is too basic. You ask an excellent question.

The formula:

(current market value – exercised cost basis)/ current market value

Let’s say a stock is trading at $32.00 and the $30.00 put is sold for $1.00, the exercised discount % is as follows:

($32.00 – $29.00)/ $32.00 = 9.4%

Alan

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 05/29/15.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Best,

Barry and The BCI Team

Alan,

I traded bull put credit spreads on the weeklies for AMBA, ILMN, IBB, SWKS, FFIV, SYNA, CELG, VXX, some more than once. All contracts expired worthless. Profit for the month was $6200 including the cost of the protective puts. Maximum potential risk was never more than $40K during the month.

Thanks again for the timely useful list.

Regards,

Pete

Pete,

Congratulations on your excellent income month! I too use stocks off the list to sell put spreads when bullish. I also sell call and put spreads on SPX on a weekly rolling basis just above resistance levels or below support levels. They work well in range bound markets like we have had.

Alan, presto, your next book idea – how to generate income selling credit spreads never buying anything :)! – Jay

Congrats to Pete…love to hear the great news.

Jay, thanks for the suggestion. It’s already in the queue…near the front but we are working on a few other projects first.

Alan

Hi Alan,

you have never steered me wrong so I would value your thoughts on my current situation with one stock.

I own 300 shares of TORC Oil and Gas TOG:T selling on the Toronto Stock Exchange. I bought the shares at $11.10 in May and sold 3 June calls for .20 with an $11 strike price.

The stock is currently trading at $9.66 and the contracts expire in less than 3 weeks. Assuming the stock price stays underwater, what are my option selling strategies for the following near month a the premiums are exceedingly thin at the $11 strike price and I will be faced with the process of being exercised below my cost basis if I try to capture more premium with a lower strike price. the implied volatility for near month options is around 20%.

it is worthy to note that the stock has a 5% dividend that is secure and the largest single shareholder is the federal Canada Pension Plan which has publicly expressed its support for the stock including increasing its position.

Should I sit on the stock and collect the dividend, purchase more to lower my cost basis (not a terrible idea, the biggest drag on the stock is the current crude and Natgas prices but they will recover over time).

I don’t want my enthusiasm for covered call as an income enhancer to create a situation where the risk profile is negatively impacted.

Thank you and please continue to spread the word. Knowledge is power.

Ian

Ian,

I’m starting with the assumption that trading and commissions on the TSE are similar to those of US Exchanges:

The most crucial step in solving this dilemma is to define your goal. One of the most challenging issues for retail investors is to attempt to juggle multiple strategies with one position. Is our goal to generate cash flow by selling covered calls? Is it to collect a substantial dividend for a stock we want to own in a buy-and-hold portfolio? Are we trying to do both (portfolio overwriting)?

If it is income generation from cc writing, this stock may not meet your goal. Your 1-month return was under 1% and that doesn’t include your broker commission…check the math.

If your main mission is to collect a dividend, ccw may not be a good strategy because you must watch ex-dividend dates that may result in early assignment.

If you are portfolio overwriting, which is the most likely case, you must consider the following:

1- Set a monthly goal for option profit (usually 1/2 to 1%)

2- Write out-of-the-money calls that meet your goal (may be under your cost basis but if calls are OTM by 5% or more, early assignment is unlikely).

3- Avoid ex-dividend dates. Write calls the day after the ex-date or write 2-month calls the month prior to the ex-date (see Chapter 14 of the Complete Encyclopedia…).

4- Be familiar with all position management techniques that will allow you to avoid assignment 99% of the time (it’s never 100%).

Alan

New seminar just added: Northern New Jersey:

July 20th

6:15 – 8PM

Saddlebrook Marriott Hotel

https://www.thebluecollarinvestor.com/event/northern-new-jersey-saddlebrook-chapter-of-aaii/

Running list stocks in the news: TASR re-invents itself:

In my first book, “Cashing in on Covered Calls”, I admitted to buying way too much TASR because option returns were so high as a result of the stock being so volatile during the trial years of their stun guns (early 1990s). I learned a valuable lesson.

After all these years, TASR has caught my attention but this time for all the right reasons. It has a great story to tell. In addition to the $164 million per year generated by stun gun sales, it now also produces body cameras for police officers and has an established relationship with those who would buy these products. TASR also recently released EVIDENCE.COM, a cloud-based hosting arena for offices to upload such files. There are now 22,000 users of EVIDENCE.COM up 45% from last quarter.

As a result, consensus estimates for this year and next has risen as analysts are recognizing the potential for growth.

Our Premium Watch List shows a ranking of “B” for its Business Services industry, a beta of 1.33, adequate open interest for near-the-money strikes, a Scouter rating of “5”, and a projected earnings report due date of 7-30.

In the past week, chart technicals have turned a bit bearish so I am waiting for an uptick in momentum indicators before entering a position with TASR but definitely keeping a close eye on this one.

Alan

Alan,

If I own a stock I understand not to sell a covered call if earnings date and/or ex dividend date come before expiration date. Assuming everything else being equal what do I do? 1. Hold on to stock until above dates are passed and receive no monthly premium? 2. Sell stock and buy a new position on list and write a covered call thus getting a premium for the month? 3. Sell a OTM naked put on a new stock thus getting stock put at a lower price or keeping the premium? I prefer #3. Am a bit confused. Read your books.

Thanks,

Karl

Karl,

You pose an excellent question that does not have one simple answer. It’s like asking a baseball manager how to get a runner into scoring position: should we bunt, hit-and-run or steal a base. All are a means to an end just different ways of achieving a common goal.

Our investment goal is to achieve the highest returns while staying within our personal risk tolerance requirements. Those parameters will differ from one investor to another although most of us are conservative investors.

Ex-dividend dates: Unless there are associated tax issues, who cares if our shares are sold. That means we have maxed our trade and have the cash freed up to generate additional income streams. If we are determined to keep a dividend-yielding stock, sell the option the day after the ex-date or sell a 2-month option moving expiration further away from the ex-date thereby decreasing the likelihood of assignment.

Earnings reports: Two choices here: Sell the stock prior to the report date of hold through earnings and then sell the option after the price settles. This adds risk to the strategy but also may allow for higher returns when we experience positive surprises. This decision depends on our personal risk-tolerance. I use this latter approach infrequently but have used it in the past with companies like AAPL and CSCO and more recently with ILMN and SWKS.

Alan

Running list stocks in the news: AVGO:

Last week, Avago Technologies price rose by 11.5% after a stellar earnings release and announced deal to buy Broadcom (BRCM, also on our running list). Over the past 4 quarters, AVGO has averaged a 19% positive EPS surprise.

This outstanding company has an impressive history. It was originally part of Hewlett Packard and then spun off as Agilent Technologies which later went private as Avago. The IPO for the “public” AVGO occurred in 2009. Last year the company bought LSI Logic and became part of the S&P 500.

Our Premium Watch List shows AVGO to be in the Chips industry currently ranked “A”, a beta of 1.65, a Scouter rating of “10”, a % dividend yield of 1.00, adequate open interest for near-the-money strikes and the last ex-dividend date as 3-18-15.

Alan

Premium members:

This week’s 6-page report of top-performing ETFs and analysis of ALL Select Sector Components has been uploaded to your premium site. The report also lists Top-performing ETFs with Weekly options.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

THANKS FOR MAKING OUR PREMIUM MEMBERSHIP SO SUCCESSFUL.

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

Running list stocks in the news: MOH:

Molina Healthcare is a managed healthcare organization with government-sponsored programs such as Medicaid. It serves over 3 million members. The company boasts a 26% growth rate in revenues and 15% growth rate in enrollment over the past 5 years. On May 7th, MOH reported a stellar 1st Quarter earnings report, beating earnings estimates and a revenue increase of 53% year-over-year. There have been 3 positive surprises in the past 4 quarters averaging a surprise of 12.9%

Our Premium Running List shows MOH in the Medical industry segment which ranks “A”, a Scouter of “5”, a beta of 1.39 and adequate open interest for near-the-money strikes. The next projected earnings report date is 8-7-15.

Alan