Covered call writers will frequently find themselves in a position where the short call is expiring in-the-money (ITM), while still wanting to use the same underlying shares for the next contract cycle. How should this be managed?

3-approaches to be analyzed

- Close both legs of the trade on expiration Friday and open a new one on Monday

- Allow for exercise at the current strike price and open a new trade on Monday

- Roll the option prior to 4 PM ET on expiration Friday (could be earlier)

Pros & Cons of each approach

Closing both legs and re-opening on Monday: This will avoid the weekend risk of shares declining in value and allowing the shares to be purchased at a lower cost basis on Monday. There will be a small time-value cost-to-close (CTC) the original short call. Also, there is the risk that share price may accelerate when trading begins on Monday.

Allowing exercise and re-opening on Monday: This will save us the small time-value CTC and benefit us if share value declines when trading begins on Monday. The risk in this approach is that share value may open higher on Monday.

Rolling the option prior to contract expiration: Prior to 4 PM ET on expiration Friday, we close the current option and open a new, later-dated same or higher strike. This will result in a small option CTC time-value debit but will ensure that our cost basis will not accelerate for a stock that has performed well and we want to retain in our portfolio. This approach is the one I would favor.

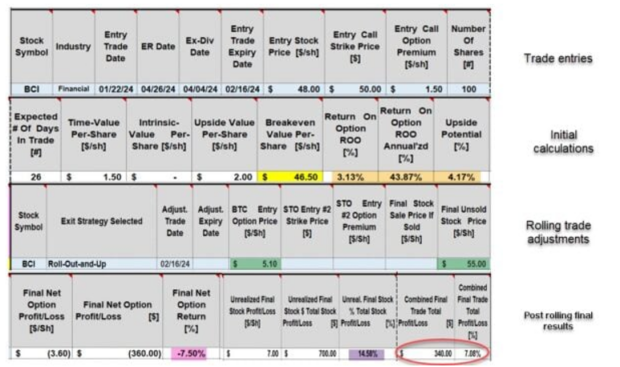

Hypothetical example of rolling a trade out-and-up (BCI example)

- 1/22/2024: Buy 100 x BCI shares trading at $48.00

- 1/22/2024: STO 1 x 2/16/2024 $50.00 call at $1.50

- 2/16/2024: BCI trading at $55.00

- 2/16/2024: BTC the 2/26/2024 $50.00 call at $5.10

- 2/16/2024: STO 1 x 3/15/2024 $55.00 call at $2.00 (roll-out-and-up to an ATM strike))

Initial trade and post-adjusted (rolling-out-and-up) entries and calculations:

The BCI Trade Management Calculator (TMC)

- Initial calculations show a 26-day return of 3.13%, 43.87% annualized (brown cells)

- There is an additional upside potential income stream of 4.17% (also brown cell)

- The 1st aspect of rolling-out-and-up is the $5.10 CTC and is entered into the spreadsheet in the adjustment (exit strategy) section

- At this point, we have a net % option debit of 7.50% (pink cell) and net unrealized stock credit of 14.58% (purple cell), for a final current month return of $340.00 per-contract or 7.08% (circled in red).

- In the screenshot below, the next contract entries and initial calculations will be analyzed

Post-rolling-out-and-up entries and initial calculations

- The $2.00 per-share premium, results in a 29-day initial time-value return of 3.64%, 45.77% annualized (brown cells)

- Since this is an at-the-money (ATM) strike, there is no upside potential or downside protection of the initial time-value profit (green cells)

- There is always a breakeven price point, in this case, it’s $53.00 (yellow cell)

Discussion

When our covered call trades are expiring ITM, we have several choices if we want to use the same underlyings in the next contract cycle. There are pros & cons to each approach. I strongly favor rolling the options when I am still bullish on the underlying stock or ETF.

Stock Repair Calculator

What is the stock repair strategy?

- Own shares at a price higher than current market value (unrealized loss)

- Willing to forego potential profit in exchange for lowering the breakeven price point

- Not willing to add additional funds to the current losing position

- Instead of buying shares at the lower price to “average down”, an at-the-money (near-the-money) call option is purchased and funded by selling 2 out-of-the-money call options

- 2 long positions (stock and ATM or NTM call)

- 2 short positions (OTM calls covered by long positions)

- This action will lower the breakeven price point

- The strategy does not protect against additional downside loss

- The strategy does cap the upside

Click here to learn more and order.

Premium Membership Price Increase Notification: No Rate Increase for Current Members

On September 1, 2024, BCI will be raising membership rates for new members only. This will not apply to current members. It has been 3 years since we had a rate increase. In that period, we have added dozens of training videos, additional downloads and resources and more quality data to our stock and ETF reports. We are fortunate to have such a robust and expanding membership and strive to provide the best high-quality information and tools at the lowest industry prices.

This price increase will not apply to current active members as you are grandfathered into the current rate for life or as long as your membership remains active. This is our loyalty pledge to you.

The increase for new members will go into effect on September 1, 2024, as follows:

Monthly: $19.95 for the first (trial) month and $69.00 each 30-days thereafter (currently $57.95).

Annual: $778.95 for the first 13 months (includes a reduced first month and a free last month) and then $828.00 every 13 months thereafter (includes 1 free month). Currently $657.40 and $695.40.

All new members who subscribe between now and 8/31/2024 will be grandfathered into the current rate and will see no price increase on 9/1/2021.

Thanks to all our loyal members for your support over the past 17 years and for putting BCI on the financial map.

Click here for member benefits video.

Click here for membership information.

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to publish several of these testimonials in our blog articles. We will never use a last name unless given permission:

Alan,

Thank you for your Portfolio Setup spreadsheet! I do enjoy and appreciate you, Barry and the BCI system have improved my retirement portfolios over the years.

Best wishes,

Jim

Upcoming events

1. BCI-Only Webinar (Zoom)

July 18, 2024

Exit Strategy Choices After Exercise of Cash-Secured Puts

When we sell cash-secured puts, we are undertaking the contractual obligation to buy shares at the strike price by the expiration date. Typically, we only sell puts on elite-performers that we would be agreeable to own in our portfolio.

This presentation will analyze 4 potential exit strategy opportunities to consider should the put option be exercised. Information on the following strategies will be highlighted:

- Selling the stock

- Holding the stock in our long-term buy-and-hold portfolio

- Write a covered call (PCP or “wheel” strategy)

- Implement the Stock Repair Strategy

In addition to these strategies, the following topics will also be included in the webinar:

- Option basics for selling cash-secured puts

- Option basics for covered call writing

- Real-life examples

- Calculations using the BCI Trade Management Calculator (TMC)

- Event super discount offer

There will be information offered to all levels of options trades, from beginners to advanced.

A live Q&A will follow the presentation. Attendees can ask any questions related to covered call writing or selling cash-secured puts.

2. Investment Masters Symposium (live, in person event)

August 1, 2024

Presentation #1: 8:45 AM – 10:45 AM (2hour option class)

Presentation #2: 5:45 PM – 6:30 PM (All Stars of Options panel discussion)

Paris Hotel, Las Vegas

Covered Call Writing & Selling Cash-Secured Puts to Generate Consistent Cash Flow

Basic & advanced principles for trading low-risk stock options with capital preservation in mind

This presentation will detail stock selection, option selection and position management, the 3 required skills to become elite covered call writers and put sellers. It will also include ultra-conservative approaches to these strategies using Delta and implied volatility to create statistically beneficial trades. Rules and guidelines will be discussed to take the emotions out of our trades resulting in high-probability positive outcomes.

Detailed analysis will be provided regarding how to craft our trades to the current market environment, personal risk-tolerance and strategy return goals.

A multi-tiered option-selling strategy which combines both covered call writing and selling cash-secured puts will also be examined. It is known as the PCP (put-call-put) or “wheel strategy.”

Attendees will be introduced to a one-of-a-kind trade management tool, the Trade Management Calculator, which is used to enter, manage and generate final realized and unrealized trade results.

The course is structured to benefit both beginner and advanced option traders, using real-life examples to enhance the learning process.

Presentation #2: All Stars of Option Trading Event

3. Mad Hedge Investor Summit

September 10, 2024

11 AM ET – 12 PM ET

Zoom webinar.

Tuesday September 10, 2024

11 AM ET – 12 PM ET

How to Generate Greater than Maximum Covered Call Writing Returns Using Exit Strategies

Incorporating the mid-contract unwind (MCU) exit strategy into a 12-day trade

More information & registration link to follow.

4. Stock Traders Expo- live event in Orlando Florida

October 17 -20

Details to follow.

5. American Association of Individual Investors/ Los Angeles Chapter

November 9, 2024

12 PM ET – 1:30 PM ET

Private webinar for members of this AAII investment club

Alan,

I have a large account with stocks that give dividends and want to sell covered calls out of the money to keep the shares. In your book, you call this portfolio overwriting.

My questions is about dividends. You say not to have a covered call in place if there is an ex dividend date coming up. Does this mean I should wait till the day after that date to sell covered calls? Is that enough time?

Thanks a lot.

Jorge

Jorge,

Early exercise of our options is extremely rare. When it does occur, it is usually related to ex-dividend dates.

If it is critical to avoid exercise, we should write our calls the day of, or any time after the ex-date.

The most common time for early exercise (remember, very rare) is the day prior to the ex-date.

Alan

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 07/12/24.

Be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them on The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

https://www.youtube.com/user/BlueCollarInvestor

Reminder: Premium Member’s pricing is locked into your current rate and you will never see a rate increase as long as the membership remains active.

Barry and The Blue Collar Investor Team

Dear Barry,

I have a few newbie questions that I couldn’t find clear answers to online, until I found you. I would really appreciate your help.

I sold a covered call on SPY with a strike price of

710

a

n

d

a

n

e

x

p

i

r

a

t

i

o

n

d

a

t

e

o

f

J

u

l

y

10

t

h

.

A

s

o

f

t

o

d

a

y

(

A

p

r

i

l

30

t

h

)

,

S

P

Y

h

a

s

r

i

s

e

n

t

o

710andanexpirationdateofJuly10th.Asoftoday(April30th),SPYhasrisento718. My call now has a delta of 0.58 and $20.13 of extrinsic value remaining.

I am struggling with when I should roll this option. If I wait longer, the price may go up even more. But rolling right now also feels difficult, given how aggressively both SPY and QQQ have been rallying.

What would you do in my situation?

Thank you very much for your insight.

Best regards,

Dear Barry,

I have a few newbie questions that I couldn’t find the right answer to on the internet, until I found you. Please help.

I sold a covered call on my SPY, strike price 710, expiring July 10th. As of today, April 30th, SPY has reached 718, my delta is 0.58, with 20.13 extrinsic value.

I’m struggling with when to roll this option. If I wait longer, the price may go up even more. But rolling right now feels crazy too, as SPY and QQQ are both rallying like crazy.

What would you do in my situation? I would truly appreciate your advice.

Thank you.

Alan,

You have stated many times that weekly and monthly option give greater annualized returns than options expiring many months out or even LEAPS for that matter. Is there a formula to calculate the difference or do we just have to calculate each and then compare?

Thank you very much.

Frank

Frank,

The best way to compare annualized returns of various dated expirations is to enter the data into our Trade management Calculator (TMC) and allow the spreadsheet to do the math.

That said, there is a formula with limited capabilities, the “Square Root Formula”. This states that in order to double the returns of a shorter-dated option, we must go out 4 times the timeframe of the shorter-dated option. Here’s an example:

If we generate $2.00 per-share when selling a 1-month option, we must go out 4 months to generate $4.00. The square root of 4 = 2. We will not receive 4x the premium by going out 4 months, only 2x the original premium. Yes, we will receive a larger premium going out 4 months, but the annualized return will be lower.

*** This formula applies only to at-the-money (ATM) strikes.

Bottom line: The best way to compare annualized returns is to use our TMC. The square root formula is instructive in that it demonstrates that shorter-dated options typically generate higher annualized returns.

Alan

Alan,

Based on your response to Frank, shouldn’t we only be selling weekly options to get the most premium and annualized returns? Am I missing anything?

Thanks,

Ron

Ron,

I use both. Both work well. Weekly and monthly expirations both have their pros & cons.

Weekly options will, generally, generate higher annualized returns … yes. They also avoid weekend risk and help navigate around ER and ex-dividend dates.

Monthly expirations allow us to screen a larger pool of underlying securities, require less frequent management and typically have greater option liquidity (some exceptions).

Bottom line: Both work well and expiration selection should be based on understanding the advantages and disadvantages of each.

Alan

Alan:

I would be interested to know if there is an upper limit IV value above which you would be reluctant to consider an option trade.

Also, is the IV value among the parameters considered in developing the weekly list of suggested option prospects?

As always, thank you for your response & the great work done by you & your staff.

Paul

Paul,

Implied volatility is an important factor in our option trading decisions. The premiums we receive and the associated risk we are incurring is directly related to IV.

I do not use specific IV stats to eliminate or embrace specific trades, but rather % returns which is directly related to IV.

For example, in my monthly portfolios, my initial time value return goal is 2% – 4%, and I’ll go as high as 6% in strong bull markets., but never higher. This will ensure that I avoid extremely risky (high IV) scenarios. I do not allow high premiums entice me into high-risk trades.

In my weekly portfolios, I cut my return goal range to 0.5% – 1% per week.

We do provide IV stats in our premium member reports, but do not eliminate securities with high IVs. The reason is that, in our BCI community, we have members that are comfortable with a broad range of risk they are willing to incur. There is no right or wrong here. We provide watchlists of elite-performing securities with all the data needed for our members to make selections that align with their return goal range and personal risk tolerance.

Your point of factoring in IV is an excellent one.

Alan

Alan,

Is your guideline of 2 to 4 percent based on a monthly time period or does it apply to weekly options as well?

For example: if I am looking to sell a monthly call option with 4 weeks left until expiration, I should use the 2-4% guideline. But if I am looking to sell the monthly option with 2 weeks left, would I divide the premium by the cost of the shares and then multiply the results by 2 to see if the results fit within the 2-4% guidelines?

Alan B.

Alan,

Yes, to both. I have been using the 2% – 4% guideline for cash reserve for 20+ years now. I use it in all my portfolios … weekly and monthly. I have found it to be both reliable and useful in management of my trade positions.

I don’t reduce the amount for shorter-dated options because we never know how much intrinsic-value we have to pay to close an ITM strike.

Alan

Alan,

So, if there is only one week left on a monthly option, when looking to sell that option, the premium should still be in the 2-4% range?

Alan B.

Alan,

I misunderstood your question … sorry. I thought you were referencing the cash reserve required for potential exit strategy opportunities.

Now, to answer your real question:

When selling a weekly call option and to stay within my personal risk-tolerance (may differ from others), I use an initial time-value return goal range between 0.5% – 1 1/2%.

Alan

Alan,

I know that this is something I should know. But when you set an alert for BTC option, are you setting the alert for the price based upon the mark, bid or ask. I assume the ask.

Thanks,

Tom

Tom,

Good question.

We set the 20%/10% BTC GTC limit orders based on the premium received. If we sold an option for $2.00, the limit order is set at $0.40 at the start of a monthly contract and it is changed to $0.20 with 2 weeks remaining. We use 10% for weekly expirations.

These are “guidelines”, so we can opt to close if the value is getting close to, but hasn’t quite reached, the threshold. Otherwise, the process is automated for us.

Our Trade Management Calculator (TMC) gives us the exit strategy BTC price points in the yellow cells in the 1st section of the spreadsheet.

See the image below.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Alan

Alan,

One last question when you have a chance.

If market moves in such a way that you hit your breakeven point first, do you close BTC or wait it out if at beginning of the month option and still 3 weeks from expiration.

Tom

Tom,

I am structured and non-emotional regarding my trade management. I adhere to our 20%/10% and 7% guidelines when considering closing my short calls or long stock positions, even if the BE price point is breached.

Alan

Premium members:

This week’s 4-page report of top-performing ETFs, along with our sample trade of the week, has been uploaded to your premium site. The Select Sector SPDR section is now crafted to align with our streamlined (CEO) approach to covered call writing. The report also lists Top-performing ETFs with Weekly options, mid-week market tone as well as the implied volatility of all eligible candidates.

We have also included a sample trade taken from one of our BCI watchlists.

Premium member video link:

https://youtu.be/EXMO-KwZuJs

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team