Apr 9, 2016 | Investment Basics, Option Trading Basics, Stock Option Strategies

Covered call writing and selling cash-secured puts involve both buying and selling of call and put options. We are dealing with two types of options as well as utilizing both long and short positions of each. When we factor in the major Greeks, it is important to...

Mar 12, 2016 | Covered Call Exit Strategies, Exit Strategies, Investment Basics, Option Trading Basics, Put-selling, Stock Option Strategies

The Greeks play a major role in both covered call writing and selling cash-secured puts. Understanding these factors and tailoring our strategy based on this insight will allow us to elevate our returns to the highest possible levels. In today’s article, we will...

Dec 26, 2015 | Investment Basics, Option Trading Basics, Options Calculations, Stock Option Strategies

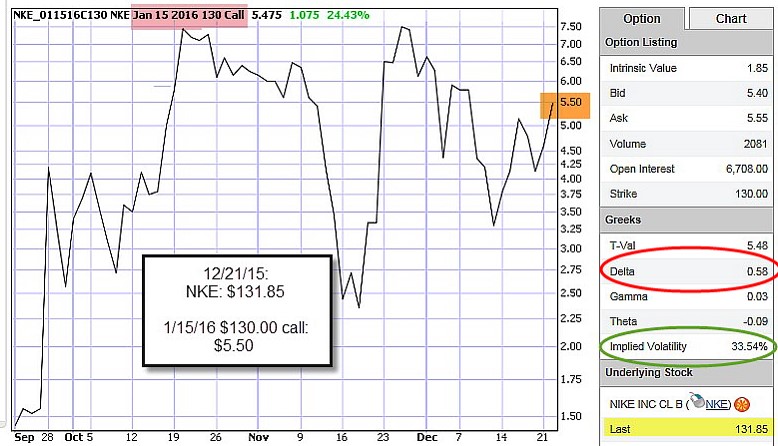

Covered call writers and put-sellers know that option value is impacted by the change in stock price by the amount of its Delta. Delta, one of the option Greeks, is defined as the amount an option value will change for every $1.00 change in share value. If a call...

Sep 26, 2015 | Investment Basics, Option Trading Basics, Options Calculations

The Greeks are a mathematical means of estimating the risk of stock options. Delta measures the change in the option price due to a change in the stock price, Gamma measures the change in the option delta due to a change in the stock price, Theta measures the change...

May 2, 2015 | Exit Strategies, Investment Basics, Option Trading Basics, Stock Option Strategies

Understanding and mastering the Greeks are key factors in becoming an elite covered call writer and put-seller. In this article, I will focus on delta, one of the important Greeks, as it relates to the moneyness of options (in-the-money, at-the-money or...

Podcast

Podcast