Options trading basics teaches us that the VIX or CBOE Volatility Index demonstrates the market’s expectation of 30-day volatility. It measures market risk and is also known as the investor fear gauge. With this in mind, covered call writers are faced with a dilemma. Increased market volatility will translate into higher option premiums because the time value component of the premium is directly related to volatility. On the other hand, a high overall market volatility increases our risk as share value can plummet and erase our initial gains. So is a higher VIX a positive or a negative?

One question that is frequently posed to me is that if the VIX is low do we stop selling calls because of lower premiums? This implies that a high VIX is a positive for covered call writers. Let’s take a look at an extreme example in 2008 when the VIX went from the 20 – 30 level to the 70 – 80 level in the last 4 months of the year:

VIX in 2008

As a general rule, the VIX and the performance of the overall market (S&P 500) are inversely related as demonstrated in the chart below where the market takes a dive in the last 4 months of the year:

S&P 500 in 2008

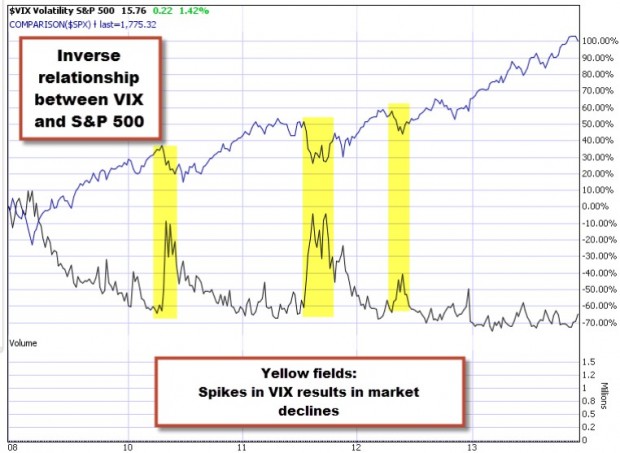

To confirm this relationship, let’s look at a comparison chart of the VIX and the S&P 500 since the decline in 2008. In the chart below, note how the VIX has been declining while the overall market has been accelerating. Whenever there was a short-term spike up in the VIX, there was a corresponding decline in the market performance:

VIX vs. the S&P 500 from 2008 – 2013

This past week

With the markets reflecting huge price swings this past week, we would expect a rise in the VIX and an inverse movement of the S&P 500. Here is the comparison chart as of 10 AM ET on April 11th, 2014:

VIX rising this past week

VIX and covered call writing:

Covered call writing is a conservative strategy and those who use it are generally conservative investors looking to generate cash flow with capital preservation in mind. As such, a high VIX is no friend of covered call writers although we can use our common sense principles to manage those scenarios. A low VIX (under 20) is usually a positive for us because it means a more stable market and oftentimes a rising market as we have experienced since early 2009.

How to manage a high VIX:

We can “stay in the game” by selling in-the-money strikes, using options with lower implied volatility (set goals at 1 – 3% instead of 2 – 4%) and use low beta stocks from our premium reports and ETFs.

How to manage a low VIX:

This is one of the factors that will give us the confidence to take a more bullish stance and sell at-the-money and out-of-the-money strikes with higher beta stocks and higher implied volatility options.

The exit strategies selected in these environments are detailed in my books and DVD Programs.

Conclusion:

The VIX is a factor that should be considered in our covered call writing decisions. It should neither be feared nor embraced but rather managed using the fundamental, technical and common sense principles of the BCI methodology.

Amazon sale of my latest book, Stock Investing For Students

I have been informed that Amazon.com will be running a sale on the kindle version of my 4th book, Stock Investing For Students. The price is being reduced from $9.99 to $2.99 for a limited time frame from 4-14 to 4-20-14. Here is the Amazon.com link:

In the brief amount of time since the book was published, I am humbled to report that it has become required reading for finance students at The University of Maryland and will be the basis of an online college credit course later this year through an international broker-dealer. Thanks so much for your support and for helping to make the launching of this book so successful. For more information about the book or to order the paper-version:

Next live webinar: eMoney Show

Tuesday April 22nd

3:20 – 4:20 PM EDT

Place: your computer

Market tone

This week’s decline in the markets was highlighted by concerns over low inflation which may reflect weak economic growth throughout the globe:

- Minutes from the March 18-19 FOMC meeting suggested that the Fed will not be raising short-term interest rates in the near future despite the Central Bank’s lowering of its bond-buying program by $10 billion per month

- Initial jobless claims for the week ending April 5th came in at 300,000, lower than the 320,000 predicted by analysts

- Revolving credit (like credit cards) dropped by $2.4 billion in February mainly due to the harsh weather conditions

- Non-revolving credit (cars, student loans) however, rose by $19 billion in February

- The total rate for consumer credit (A report of the dollar value of consumer debt, including categories such as credit card use and store charge accounts -known as revolving debt- as well as longer-term loans for autos, education, recreation vehicles – known as nonrevolving debt. The level of consumer credit is considered a barometer of consumers’ financial health and an indicator of potential spending patterns) came in at $16.5 billion higher than the $14.1 billion expected;. This represents an annualized rate of 6.4%

- According to the Labor Department, the Producer Price Index (a measure of the average change over time in the selling prices of a fixed basket of goods by stage of production, industry, and commodity. It is considered a leading indicator for consumer inflation. The “core” PPI excludes food and energy prices—which account for roughly one-quarter of the broad PPI and tend to fluctuate widely—providing a truer reflection of inflationary trends) increased by 0.5%, much more than the projected 0.1%. The year-over-year reading, however, came in at 1.4% price growth

For the week, the S&P 500 declined by 2.6%, for a year-to-date return of (-)1.2%, including dividends.

Summary:

IBD: Market in correction

BCI: This site maintains a cautiously bullish outlook on our overall economy but is taking a defensive posture as market volatility has increased (still below levels of extreme concern). As a result, we are favoring in-the-money strikes 2-to-1 until that volatility subsides.

Here’s to a better week ahead,

Alan and ther BCI team (alan@thebluecollarinvestor.com)

www.thebluecollarinvestor.com

Alan,

How do you factor in the volatility of the individual stock when making your final decisions?

Thanks,

Paul (new member)

Paul,

The use of implied volatility is an important consideration in our covered call decisions. It is not necessary to calculate or look up IV because the option premium will shed light on this statistic.Since the time value of the premium is mainly impacted by time to expiration and implied volatility of the underlying security and since we are selling mainly 1-month options, the % return as it relates to time value will help guide us in our final decisions.

Now there is no right or wrong as to the % return we set as our goal because that is an individual decision based on market assessment, chart technicals and personal risk tolerance. The higher the % return (time value), the greater the risk. My personal goal for initial returns is 2-4% per month. More aggressive investors may set higher goals and vice-versa.

Good question.

Alan

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 04/11/14.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are in Earnings Season, be sure to read Alan’s article, “Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The BCI Team

I have noticed over the last year or so that the spreads on the Bid/Ask have on several stocks have been excessive(even when there is good volume (see attachment-CAR). Even when trying to get filled at the mid-point I would be unsuccessful. What is your take on this? Thanks.

Bob C.

Bob,

Let me respond in 2 parts. First, don’t use the mid-point. Drop down a bit in favor of the market maker. Your successes will increase with that approach. For example, if the b-a spread is $3 – $3.50, place a limit order for $3.20 and remember not to check the “all or none “box.

In the BCI methodology, our guideline is an open interest of 100 contracts and or a b-a speard of $0.30 or less. As you can see from the option chain below, the highlighted option do meet our criteria. CLICK ON CHART TIO ENLARGE AND USE THE BACK ARROW TO ERETURN TO BLOG…see comment below this one as well

Bob,

As a followup to last comment, below is the calculations from the multiple tab of the Ellman Calculator WITHOUT negotiating the b-a spread…worst case scenario.

Alan

Alan, I have a few questions to ask you about the charts/running list, to carry on from those other ones I asked you. I’ll start with the running list,:-

1. When prioritizing the running list factors(of price,etc) I wanted to make “Price” as my 1st priority, with my 2nd being “Bold listed stocks”. But can I make a “strong technical chart” (price above EMA’s in an uptrend) as my next(3rd) priority instead of the “Industry rank”? (I saw this as more important.)?

2. If there is a divergence or two on a stock with mixed technicals then does this put you off buying it, or would you buy it and then sell ITM options?

3. If the market and/or a stocks price has risen up quite a bit and is now consolidating, then is it worth me to buy a protective put option in case of a market fall?

4. And if the price has gone down a bit and consolidating, then do you still sell ITM options, or are you in hope of the price to go up and so sell OTM options?, – does it depend on how far the price has fallen?

I do have 2 things to query you on about the Vix, and so would likely ask them to you next. Thanks

Adrian,

My responses:

1- Yes, prioritize as you see fit. The reason we provide so much information in our premium stock reports is that it allows our members (and me) to use the information to meet the needs of our trading styles and personal risk tolerance.

2- Stocks with mixed technicals that earn their way onto our watch list also have great fundamentals and meet our common sense requirements (minimum trading volume etc.). These stocks are absolutely eligible to use in the current month. I will generally sell ITM strikes for these candidates but in a strong bull market would consider OTM strikes as well.

3- There is nothing wrong with purchasing protective puts to protect against catastrophic losses. For many investors, it will help you sleep better at night. The downside is that your % returns will suffer. It’s a personal decision each investor must make. As I have published so many times in the past, I do not use protective puts but use every other strategy available to me to mitigate losses and enhance gains. I have no problem with those who prefer to use this strategy.

4- A stock that has suffered a large price decline will not pass our screens. A stock with a small price decline and is currently consolidating can be a candidate for either ITM or OTM strikes. I use the confirming indicators (MACD histogram, stochastic oscillator, volume) and overall market assessment o make that decision.

Alan

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 04-18-14.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are in Earnings Season, be sure to read Alan’s article, “Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The BCI Team

Hi Alan,

Great blog and have been a viewer of your videos on youtube for the past year. Thanks!

If VIX is high, what are your thoughts on selling out-of-the-money puts on equities that you will eventually write calls against? In other words, get paid for buying a stock at a lower price.

Thanks,

Jeff

Jeff,

Excellent point. This is a great approach in bearish and volatile markets. Here is an article I published on this subject:

https://www.thebluecollarinvestor.com/using-cash-secured-puts-to-enter-covered-call-positions/

Alan