In bear, volatile and uncertain market environments, covered call writers turn to ITM call strikes and protective puts to create greater protection to the downside. In this article, the pros & cons of each hedging technique will be analyzed using a real-life example with NVIDIA Corp. (Nasdaq: NVDA).

Why consider ITM call strikes in challenging market environments?

ITM calls strikes have intrinsic-value components to them (the amount the strike is lower than current market value). This component of the option premium, along with its time-value component will lower the breakeven price point to a greater extent than ATM or OTM call strikes, which have only time-value premium. This additional (limited) downside protection is paid for by the option-buyer (not us) in the form of intrinsic-value. In return from benefitting from taking this defensive posture, we are eliminating any additional income from share price acceleration.

Why consider protective puts (collars) in challenging market environments?

Adding protective puts to our covered call trades (collars) costs money. We, the option sellers, pay for it. Collar trades should be established with a net option credit which will result in a positive initial return, some upside potential, a small zone for potential losses and then protection all the way down to zero (catastrophic share loss is avoided).

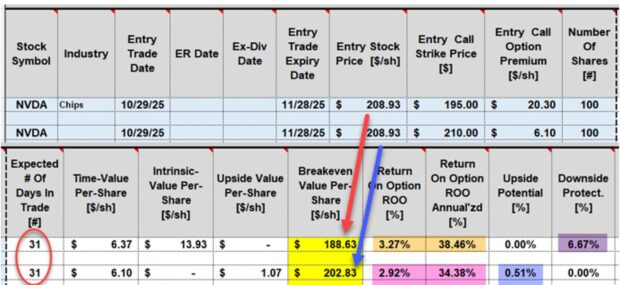

Real-life example with NVDA: 1-month Option chain on 10/29/2025

- For an ITM covered call, we’ll select the $195.00 strike, which has a bid price of $20.30

- For the protective put/ collar trade, we’ll select the OTM $210.00 strike which has a bid price of $11.85, and the $195.00 protective put which has an ask price of $5.75

- The net option credit for the collar is $6.10 ($11.85 – $5.75)

Comparing calculation returns for both approaches using the Trade Management Calculator (TMC)

- THE ITM $195.00 call lowers the BE price to $188.63 (red arrow)

- The collar lowers BE price to $202.83, (blue arrow) but will then also protect against catastrophic share price decline below the $195.00 put strike

- The initial time-value return for the ITM strike is 3.27%, 38.46% annualized (brown cells)

- The initial time-value return for the collar is 2.92%, 34.38% annualized (pink cells) with an additional upside potential of 0.51% (blue cell)

Summarizing returns and protection

- The initial returns are similar so path selection should not be based on initial calculations

- The ITM call offers protection down to $188.63, with risk of share value loss from that point down to zero (of course, we would initiate exit strategy intervention way before zero!)

- The collar offers protection down to $202.83 and then from $195.00 down to zero, leaving a risk range between $202.83 and $195.00

- Given these calculations, each investor can decide which approach aligns best with their personal risk tolerance and strategy goals as both offer significant protection for our covered call trades

Discussion

In bear, volatile and uncertain market conditions, covered call writers can generate significant annualized returns while still crafting their trades to garner substantial protection to the downside. In this article, ITM call strikes and adding protective puts (collars) were analyzed.

PREMIUM MEMBERSHIP & New Member Discount Coupon

$200.00 DISCOUNT COUPON: For new annual members: join200

Free training resources

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to publish several of these testimonials in our blog articles. We will never use a last name unless given permission:

Hi Alan,

Abdul

1. Hollywood Florida Money Show

April 8: Trading Panel

April 9: 2-hour Master Class

3:30 – 5:30

The Put-Call-Put (PCP) or Wheel Strategy

Using Both Covered Call Writing and Put-Selling to Generate Monthly Cash Flow

Selling stock options is a proven way to lower our cost-basis and beat the market on a consistent basis. Two such low-risk strategies are covered call writing and selling cash-secured puts. This presentation will detail how to incorporate both strategies into one multi-tiered option-selling strategy where we either generate cash-flow or buy shares of stock at a discount. I refer to this as the Put-Call-Put (PCP) Strategy, also referred to as the wheel strategy.

The basics and pros and cons of low-risk option-selling strategies will be discussed as well as an analysis of a real-life example and introduction into the BCI Trade Management Calculator (TMC). This seminar is appropriate for those who look to generate modest, but consistent, returns which will enable us to potentially beat the market on a consistent basis while focusing on capital preservation.

April 10: Portfolio Overwriting

11:40 – 12:25

2. Sarasota Investment Group

Portfolio Overwriting: A Form of Covered Call Writing

Wednesday April 22, 2026

Details to follow.

3. BCI Educational Webinar #10: The Put-Call-Put (PCP) or “Wheel Strategy”

Thursday May 14, 2026, at 8 PM ET

Using both covered call writing & cash-secured puts in a multi-tiered option selling strategy. A 68-day real-life example taken from one of Alan’s portfolios will be analyzed.

BONUS: Barry will share a real-life credit spread trade using our BCI Conservative Credit Spread Management System.

Discount coupons and a live Q&A session will follow the presentation.

4. American Association of Individual Investors: NYC Chapter

June 10, 2026, at 6 PM – 8 PM ET

More information to come.

5. Toronto Money Show

September 24 – 25, 2026

MaRS Center, Toronto Canada

6. Orlando Money Show

October 5 – 7, 2026

Details to follow.

Premium Members,

This week’s Weekly Stock Screen and Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 03/20/26.

Be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them on The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

https://www.youtube.com/user/BlueCollarInvestor

Barry and The Blue Collar Investor Team

Alan,

Great “wartime” video and reminder of the fundamentals.

Quick question, how are you choosing the strike prices? Is it based on being one or two standard deviations away from the current price based on IV? Or a target total return?

Thanks.

Todd

Todd,

The video analyzed a cash-secured put portfolio where we want to avoid exercise of the deep OTM put strike. I’ll focus on this in my response.

If we are using covered calls, this answer may be slightly different depending on exercise requirements (may not want to sell shares or no problem if shares are sold).

There are 2 metrics we can use to determine put strike prices … delta and implied volatility (IV). For IV, we can use 1 standard deviation (SD) or 2 SDs.

These reliable metrics will quantify for us the risk of exercise. Next, we must make sure that the selected strikes meet our pre-stated initial return goal range. For these ultra-low risk portfolios, that could be between 5% and 20% annualized. Goals will vary from investor-to-investor.

Alan

Alan

How did you pick the put strike prices?

Why no mention of beta?

I have been doing weekly puts for some time and batting near 100% while selecting betas of approximately -.1 and ARR of 10-15%. (my rules)

I am happy with this return (for a portion of my portfolio) since the risk is so low.

Bob

Bob,

I look at delta (risk of exercise) and implied volatility (1 – 2 standard deviations) to determine my strike prices.

I prefer IV over beta because it is forward-looking compared to historical. Beta is also a good metric, but I give the nod to IV.

So pleased to learn of your success, using this conservative approach. Keep it up!

Alan

Thanks.

One last question re IV.

Do we use the IV % at the current price and date or the strike price and the date of the strike?

thanks

bob

Thanks Alan. Do you recall what the SDs were for the examples in the video? If not, no worries.

Todd

Todd,

Here’s how I do it: I use the ATM IV and the BCI Expected Price Movement Calculator to generate an expected trading range based on 1 SD.

Then I double the calculated expected price movement to generate a 2 SD strike. If the return on that 2-SD strike meets my pre-stated initial time-value return goal range, I go with the lower strike. If not, I use the 1 SD strike.

Let me give you a hypothetical example: If the ATM IV and the Expected Price Movement Calculator show a price movement up or down of $6.00 for a $50.00 stock, the 1SD deviation will leave me at a $44.00 strike. The 2 SD strike would be at $38.00 ($6.00 x 2). If the bid price of the $38.00 strike meets my goals, I go with that one. If not, I’ll use the $44.00 strike.

In other words, I use the safest strike that meets my goals.

Alan

Very clear. As I expected. Thanks for taking the time to clarify!

Todd

Bob,

Glad to help. Use the ATM IV for the contract in question.

Alan

Premium Members:

1. This week’s ETF Report has been uploaded to your member site. Login to the member site and scroll down on the left side to access the report.

ETF Report Video Link:

Explanation of the report format:

https://youtu.be/addf7Y54ixwput

2. I’ve attached two 2-contract covered call trades, using NVT as the underlying stock. I executed these trades on 3/23/2016, for the 4/17/2026 expirations (26-days). Significant initial returns, upside potential and downside protection were generated at the onset of the trades. This is an example of laddering strikes when selling multiple contracts with the same underlying security. This stock (NVT) closed at $127.01 today, up $3.07 from the starting point. It is $12.01 above the $115.00 put strike, $14.87 above the ITM breakeven and $6.60 above OTM breakeven. This trade has 23 days remaining until expiration, so the final outcome is yet to be determined, but I’m quite pleased with the current status. As always, I remain prepared to execute exit strategies, if those opportunities arise.

3. Our loyalty pledge to you: Premium members will NEVER experience a rate hike as long as premium member subscriptions remains active … NEVER.

4. Have you seen my new video on Wartime Option Strategies?

https://youtu.be/wMq0vC9tjhA

Wishing you the best results,

Alan & the BCI team