Covered call writing and selling cash-secured puts are cash-generating strategies. These profits can be impressive as isolated events but what if we then take these proceeds and re-invest them to amplify our returns? The BCI philosophical approach to option-selling stresses the importance of re-investing our short-term premium returns whenever possible. Of course, for many of us, these revenues are needed to supplement our active income. When I started selling options, the revenue was used to help fund my sons’ college and professional school educations as well as purchase my first real-estate investment property. I currently sell options in my mother’s account to enhance the quality of her golden years. However, in situations when premium returns can be re-invested, the power of compounding can truly be defined as the 8th wonder of the world.

Compounding and long-term investing

To demonstrate how compelling compounding our profits can be, I will reference my book, Stock Investing for Students which is a long-term investment plan predicated on re-investing all passive income. Whether we are short or long-term investors, the power of compounding must be respected and considered. Here is the plan based on historical data (no monkey business…and stats can be adjusted to any time frame):

- 40-year plan starting after high-school graduation

- Start with an investment of $1,000.00 to open a brokerage account

- Invest 10% of your gross annual income (GAI)

- 1/12th of this 10% figure is invested monthly via dollar-cost averaging

- All dividends are re-invested

- Assumes an average GAI of $60,000.00 for the first 20 years

- Assumes an average GAI of $80,000.00 for the last 20 years

- Uses low-expense-ratio, broad market index funds generating an 8% annualized return

- Can move to individual stocks and options to generate even higher returns

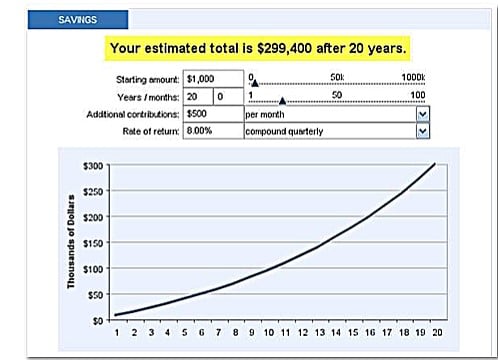

First 20 years

Compounding Profits for the First 20 Years

Using a compounding savings calculator found at www.bankrate.com, we generate a portfolio balance of$299,400.00.

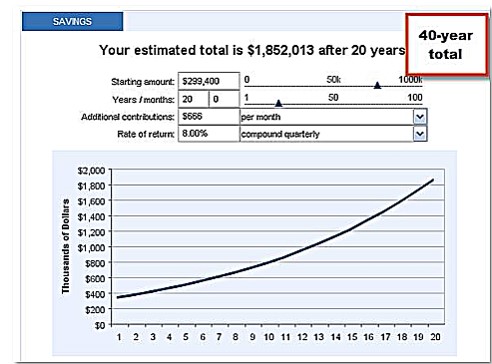

Last 20 years

Compounding Profits for the Last 20 Years

Based on the low side of historical data, the calculator shows a final portfolio balance of $1,852,013.00. Using individual stocks and stock option-selling should significantly enhance these final returns.

Discussion

Option-selling should result in returns that consistently beat the overall market. By re-investing these profits and taking advantage of the power of compounding, these cash flows will be elevated to substantially higher levels.

Upcoming event

AAII National Investor Conference: Las Vegas Nevada

October 26 @ 8:00 am – October 28 @ 1:00 pm

October 26th – 28th, 2018 (Friday through Sunday)

Alan’s presentation: Saturday October 27th at 9:30 AM

Visit Alan, Barry and the BCI team in the exhibit hall Friday, Saturday and Sunday

Market tone

This week’s economic news of importance:

- Markit manufacturing August 54.7 (54.5 last)

- ISM manufacturing index August 61.3% (57.9% expected)

- Construction spending July 0.1% (0.5% expected)

- Trade deficit August -$50.1 billion (-$50.4 billion expected)

- ADP employment August 163,000 (217,000 last)

- Weekly jobless claims 9/1 203,000 (212,000 expected)

- Productivity Q2 2.9% (3.0% expected)

- Markit services PMI August 54.8 (55.2 last)

- ISM non-manufacturing index August 58.5% (56.9% expected)

- Factory orders July -0.8% (-0.6% expected)

- Nonfarm payrolls August201,000 (200,000 expected)

- Unemployment rate August 3.9% (3.8% expected)

- Average hourly earnings August 0.4% (0.2% expected)

THE WEEK AHEAD

Mon September 10th

- Survey of consumer expectations August

- Consumer credit July

Tue September 11th

- NFIB small-business index August

- Job openings July

- Wholesale inventories July

Wed September 12th

- Producer price index August

- Beige book

Thu September 13th

- Weekly jobless claims 9/8

- Consumer price index August

- Core CPI August

- Federal budget August

Fri September 14th

- Retail sales August

- Industrial production August

- Consumer sentiment September

- Business inventories July

For the week, the S&P 500 moved down by 1.03% for a year-to-date return of 7.41%

Summary

IBD: Market in confirmed uptrend

GMI: 6/6- Bullish signal since market close of July 9, 2018

BCI: Selling an equal number of ITM and OTM strikes for new positions.

WHAT THE BROAD MARKET INDICATORS (S&P 500 AND VIX) ARE TELLING US

The 6-month charts point to a slightly bullish tone. In the past six months, the S&P 500 was up 7% while the VIX (14.92) down by 15%.

Wishing you much success,

Alan and the BCI team

Alan have you considered writing covered calls on the VIX (e.g. VXX) with sufficient downside protection to account for its natural decline over time? Would love to hear your view here.

Thanks a lot, and looking forward to staying in touch if your time allows such interactions.

Regards,

Attila

Attila,

For most retail investors, this is not a good idea. These products are quite complicated and very difficult to utilize for successful covered call writing.

You astutely pointed out the flaw with VXX…natural decline because it is an ETN based on the 2 nearest VIX futures where the back month is usually more expensive than the near month…this results in slow decay as you pointed out. Here, we are riding our bikes uphill. That said, money can be made in rare circumstances.

A better approach, if one was dead set on using volatility covered calls, would be to set up a synthetic long stock position (since there is no spot VIX market) by buying an ATM call and selling an ATM put on the VIX and then writing an OTM call against that synthetic long stock position (I’m getting a headache from all this!).

This latter approach would work best in high volatility scenarios. I say, why get involved in additional transactional situations when we can simplify our lives with stock and ETF underlyings?

I’d be interested to hear from any members who have used VIX covered calls and their experiences with these products.

Alan

Aland and Attila,

I have experience trading VIX derived futures ETN’s/ETF’s like VXX, UVXY and the short version SVXY. I understand their design workings and flaws. I also trade VIX options in my IRA.

I will start by using one of the few “never” statements in my investing vocabulary other than never sell covered calls over an earnings report: never hold VXX or it’s leveraged evil twin UVXY as an investment for longer than a few weeks. It will nibble you to death if wrong on direction. That’s not what they are designed for. They are deteriorating assets over 80% of the time and are best used for speculation in short term trades when acutely bearish if you have no access to the options on VIX like Alan used in his synthetic position example above.

As he said, these products are complicated and while you likely understand VXX and why it is forever working it’s way to long term zero others here may not. Another of my “never” rules is never trade/invest in anything you can’t explain easily to a stranger!

If you are bearish and want short term protection I think it’s best to stick with selling ITM covered calls on holdings and/or buying blanket S&P puts or put spreads so you are not spending commissions buying puts on lots of different holdings.

Thanks for the chance to share my opinions! – Jay

Alan, Atila and Jay,

I just checked the history of VXX and noticed several reverse stock splits. This alone is a big red flag.

Marsha

Marsha,

I could not agree with you more! VXX is constantly reverse splitting to keep it’s price up in a tradable range.

If you want to see a picture of the “uphill bike ride”Alan mentioned click on vixcentral.com.

The upward sloping curve you see represents the future cost of new contracts versus today. The technical term for that is “contango”. VXX can lose value even on small S&P down days when the curve is shaped that way. The fund is replacing expiring low cost futures contracts with more expensive ones.

Now, catch a VIX spike and VXX will spike! The curve will invert, that’s “backwardation” and for that time you are riding your bike downhill while the curve is inverted :)!

A story for another time is what happened to the funds like SVXY and XIV that short the curve in it’s normal state and got wiped out when that bet was caught over played and over margined when the VIX spiked this past winter.

I am still of the mind VIX is a mean reverting instrument best played to the short side after VIX spikes using calls or CSP’s on SVXY, SVXY buys or VIX puts. The historic mean on VIX is 20, in recent years closer to 15 and any time it spikes into the high 20’s and beyond layering into short bets against it has almost always worked.

If you stay long in VXX hoping/waiting for a VIX spike it can continue to erode longer than you can stay solvent! – Jay

Jay,

Just read your reply to Marsha….Now I have a headache…. It’s a lot to ponder for the first day of the Blog! It’s great, though, to have members bring up a subject area which triggered some good responses.

Mario

Jay,

This comment is gold:

“never trade/invest in anything you can’t explain easily to a stranger!”

Thank you Alan and Mario for replies above. I did not intend a deep dive into VIX products. What I did intend was to warn friends they are tricky so please research them before you use them.

I lost money in them years ago before I understood them and I would hate that to happen for anyone here today. – Jay

Hi Attila,

after reading your post, plus all the responses, I really wonder why anybody would elect to invest in this product.

I do understand the charm of ETFs, which give you diversification, and also sets you free from Earnings Reports surprises.

Personally, I prefer stocks. Real, live, dynamic, and useful companies as underlying for my Covered Calls monthly trading.

To me it feels more exiting. Like participating in the world economy.

Roni

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 09/07/18.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Best,

Barry and The BCI Team

barry@thebluecollarinvestor.com

Alan,

I just close last Friday 3 trades (covered call expiring on 21st September) since I was not sure about the market and the 3 equities start to show not so positive signals.

I realized a total of 2.7%, on line with my monthly target.

Now I have cash in my account and I would like to open other positions (I like ULTA) but the question is: I still trade covered call option expiring on 21st September or I have to move to 19th October expiring?

The idea is to buy ITM strike of 21st September option and then before expiring decide to roll out/roll out and up or left the option to expire.

ITM because ULTA has had a great week but next week is a question mark and may be it will lose some points if somebody start to cash.

Thanks and have a nice day.

Mauro

Mauro,

Generally, when I enter new positions with 2 weeks remaining to contract expiration, looking to ITM strikes that target 1 – 2% of time value initial returns is a reasonable approach. Because of the limited time for position management, the intrinsic value of the premium will provide additional protection to the downside. I do prefer this approach to moving into the October contracts. Especially for those of us who trade dozens of contracts, having all expire on the same date makes management more practical.

Alan

Alan,

I have finished your ebooks on Covered Calls and Cash secured Puts. A lot of great info.

One thing that confused me is the exit strategy for covered calls when stock price is well below our cost basis near the expiration date. I understand that we keep the call premium we received but we are already losing more money in the underlying stock than the premium we received from the call selling. But you covering the call and selling another call for the next month for lower strike than the original call (which could be equal or less than our original purchase price). In this case, don’t we commit to sell the underlying stock for lower price than we bought it for and thus commit to making a definite loss?

Sorry if I am confusing something here.

Seth

Seth,

looks like there is nothing to add to Ron’s and Mario’s perfect responses.

Still, I would like to try to clear your doubts about selling the next month call at a lower strike.

I believe this strategy is designed for mitigating your loss (if you still “love” the stock), and give you some more time to work on it, and possibly, turn it around.

Roni

Seth,

I am sorry, but you’ve already incurred a definite loss. A “paper” loss is, in fact, a definite loss. If the underlying stock still meets your investment criteria, you can continue to hold it long, while picking up an additinal option premium by employing the appropriate exit strategy.

(Having already read two of Alan’s books, you are off to a good start; now you have to read some of his other books. In particular, I would suggest the “Complete Encyclopedia for Covered Call Writing” and “Exit Strategies for Covered Call Writing”

Seth, good question… I have been in this situation many times, but in a long position already at expiration. Supplementing Ron’s comments… these are some of the actions I would pursue. Maybe others feel differently.

You position is at a large loss at expiration with an OTM position and Gain = Stock price – breakeven and Return ROO% of Gain / Cost Basis (Strike or Price of stock, depending on your initial trade ITM or OTM, respectively).

You reached this point after maybe trying unsuccessfully to fill an order to close the option for the 20% or 10% rules for a possible Hit the Double recovery. (Normally occurs when you are at a 5-8% loss from my experience, varies.)

At Expiration you let it expire worthless.

On Monday or thereafter, you can unwind the long position is stock is negative or you do not see a possible recovery situation with the market tone.

If the underlying is mixed or you feel it can recover to a higher point, you can also in Weeks 1 and 2 of 4, place an order to unwind at your breakeven point. That has happened to me many time. On a market open or other news, it might spike up to fill the order. It it is trending up, you can cancel your unwind order (I often decide to unwind and go for another investment – observing the stock keep climbing to my misfortune.)

At Weeks 3 (of 4), if the stock is sideways trading in a range, you can evaluate a roll down position OTM to the next higher to see if a 3% loss jumps to a 1% loss or similar numbers by expiration time with the current STO premium. Then, if at expiration it is still OTM, you add a new option leg for the next cycle to further improve your ROO%. If it is in the money, you can let it be assigned and be happy with the reduced loss, or evaluate a roll to the new strike if you still like the underlying.

Mario

Alan,

I am looking weekly stock selections and I like how they are labeled making it easier to choose from different sectors to diversify.

My question is, which monthly expiration do I choose when I, let’s say, open a position today? Do I buy September monthly or October monthly? When do you switch from one month to another?

Thanks.

Seth,

There is no one correct response to this question but I’m happy to share with you how I approach expiration dates. Since I average 50 -100 contracts per month, it makes it more practical for me to have all contracts expiring on the same date…the 3rd Friday of the month since I trade Monthly contracts. Some of our members prefer Weeklys and others may go our further than 1 month (without conflicting with earnings reports). Money can be made with all these approaches.

If I close a position mid-contract, I look to replace it with a new position expiring in the same contract month by setting lower initial time value goals. For example, if my original monthly goal was 2% – 4% for initial time value returns, I may drop to 1% – 2% mid-contract.

If we are in the last week of a contract and close a position, I’ll wait for the start of the new contracts to use that cash in a new position. The logarithmic nature of Theta (very little time value erosion initially) will do little damage to our overall time value returns and we are eliminating an additional week of risk.

Alan

Thank you Alan. Very helpful to know.

Another question: how do you determine your exit strategy from the underlying? I know we can aim doing double but what if the underlying price keeps dropping? At what point do you decide to exit? Are there certain “cut losses” thresholds or do you exit when the stock is no more in the weekly selected stock list?

Thanks again.

Seth,

In my books and DVDs, exit strategies are a major focus of the strategies. For a declining stock when using covered call writing, we use our 20%/10% guidelines to close our short call positions. The next step depends on time within the contract, overall market assessment, evaluating stock news etc. There are specific guidelines with examples taken directly from my own portfolios to exemplify how to manage these scenarios…too many to enumerate in this venue.

As far as a guideline as when to close the long stock position after implementing other mitigating strategies, an 8 – 10% price decline is a fair range to consider.

Alan

Alan,

Good article on compounding.

Eleven years ago I took all five of my grandchildren (ages 11-17 at that time) to my credit union and set up a savings account for each of them. I set up a program where I would match their savings up to $100.00 each month. But if they ever withdrew any funds I would stop the match. Two of them went online and set up a monthly withdrawal of $100.00 each month which was then automatically deposited in their credit union savings accounts. Smart kids!

Four years later I set up them each up an account with Vanguard. I put $3,000.00 in for each, which was Vanguard’s minimum at that time. My new deal was that I would match their Vanguard investments up to $3,000.00 per year as well as maintaining the credit union program. As a part of this program I set each one of them a personalized savings compounding calculator. It showed them what their present balance was, had a cell for investment additions, a cell for investment returns (set by me at 8%) and a cell to show the total at any point in the future.

Needless to say their minds were blown!

All five have done very well. The two I described above have become obsessive savers and have account balances that are unbelievable for young people in their mid twenties. They still enjoy life by spending money on experiences not things. One is a Dentist, how ironic, and one teaches English Lit at her Alma Mater. Of the other three one is an OBYGN, one is a registered nurse responsible for the most critical NICU babies and the youngest is still in med school. I am a very proud Poppa and like to think that I played a small part in their success.

I think it may have been Napoleon Hill who first introduced to the concept of compounding interest. I believe he may have described it as the eighth wonder of the world.

I agree.

Hoyt T

Hoyt,

What a great story…thanks so much for sharing.

You have quite an impressive family and I’m sure they realize how fortunate they are to have a Poppa like you.

Alan (aka Papa)

Hoyt,

wow !!! Fantastic, and inspiring.

Congratulations – Roni

Hey friends,

Great story Hoyt, thanks for the share!

As a follow up to the discussion at the top of the thread this video out today will be helpful for fellow market junkies out there!

https://www.tastytrade.com/tt/daily_recaps/2018-09-11/episodes/term-structure-of-volatility-09-11-2018

It supports my opinion that you should not sit around holding VXX waiting for a spike in VIX but when you see one short it for it’s subsidence/mean reversal/normalization using VIX options or SVXY. – Jay