Position management is the 3rd required skill for our covered call writing and put-selling success. On 7/19/2019, Larry shared with me a series of trades he executed with Veeva Systems Inc. (NYSE: VEEV). He astutely “hit a double” and was now looking to roll the option to the following month.

Larry’s trades and inquiry (in Larry’s words)

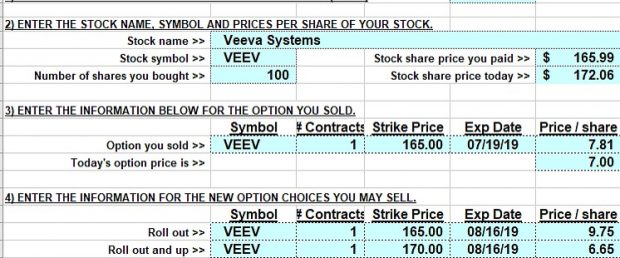

- I bought VEEV @ 165.99 on 6/17 and STO 165C 7/19 @ 7.10

- On 6/26 with VEEV @ 157.68, I BTC @ 3.30 for 3.80 profit on call. ( I know, I know, I violated your 20% rule).

- On 7/1, I resold option (165C 7/19) @ 4.01 Cr. (VEEV @ 163.78). Caught the bounce here.

- Friday, expiration Friday, VEEV trades @ 172.06 with mixed technicals (20/100 EMAs positive, MACD negative). STC 165C 7/19 looks like 6.70/7.30 (I normally limit order at mid bid/ask with Schwab and get it most of time).

- I was looking at either rollout or rollout/up to 8/16 (eps due 8/24) to either 165C @ 9.75 or 170C @ 6.65. The technicals suggest staying ITM.

- What’s your inclination on this one?

The “What Now” tab of the Ellman Calculator: Information entered

When we are considering rolling-out versus rolling out-and-up, we turn to the “What Now” tab of the Ellman Calculator:

Rolling Calculations: Information Entry

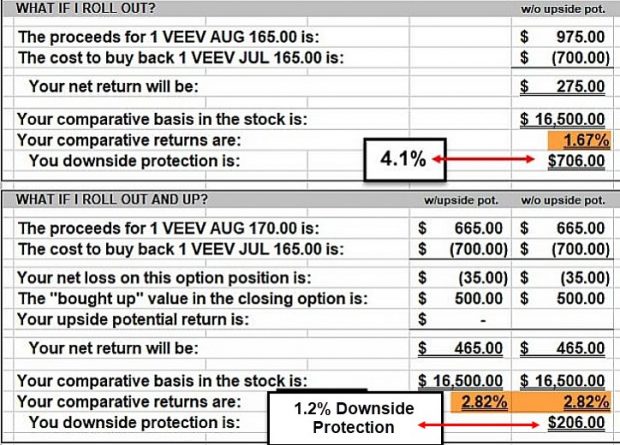

The “What Now” tab of the Ellman Calculator: Calculation Results

VEEV Rolling Calculation Results

Discussion

Based on the information Larry provided, we have the following rolling choices:

1. $165.00: 1.67% 1-month return with 4.1% protection of that profit

2. $170.00 strike: 2.82% 1-month return with 1.2% protection of that profit

We evaluate our initial time-value return goals, personal risk-tolerance and make a call. It will vary from investor-to-investor. If neither return is appealing, we “allow” assignment and use the cash in a new position with a different underlying on Monday.

*** Larry thanks for sharing your trades and great job using our exit strategy arsenal!

New Year discount offer ends Sunday

| As a genuine thank you to the thousands of BCI members, followers, and supporters who’ve made us who we are in the international options investing community, we’ve set up a special promo code to offer you the ability to get 20% off on any/all products available for purchase at the BCI Store. That’s right! Any and all products. Get started with, or expand your library of covered call writing, cash-secured puts, and stock option investing resources today, and become CEO of your own money in 2020. Use coupon code BCI20OFF at checkout. Expires Sun, 1/5/20 at 11:59pm ET US http://www.TheBlueCollarInvestor.com/store |

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to share some of these testimonials in our blog articles. We will never use a last name unless given permission:

Hi Alan,

I have been involved with the stock market since 2005. I had some good times but never consistent until covered calls. I appreciate all your videos and I literally have most of your books. My average return was 2.3% and that’s entering some trades in the 2nd week of the contract cycle.

Thanks for everything you do,

Mark

Upcoming events

1. February 6th – 9th 2020 Orlando Money Show

3- Hour Masters Class Saturday February 8th 1:45 – 4:45 PM

BOOTH 306

2. Tuesday March 10, 2020 Long Island Stock Traders Meetup Group

7 PM – 9 PM

Plainview- Old Bethpage Public Library

Covered Call Writing Blue-Chip Stocks to Create a Free Portfolio of Large Tech Companies

***********************************************************************************************************************

Market tone data is now located on page 1 of our premium member stock reports and page 8 of our mid-week ETF reports.

*********************************************************************************************************************

Hi Alan,

First, very best wishes for the New Year.

My question is: when a stock no longer qualifies for the current week (e.g. AMED last week and EDU this week), are we supposed to close the call and sell the stock or, as long as everything seems to be on track, to simply monitor it more closely.

By the way, AMED qualifies again this week so I did not do anything. For stocks with ER falling before the expiration of the call, it is clear that I need to get out before the day of earnings.

I began about 3 weeks after the AAII Conference in Orlando, put it 100k and am on track to get 2% a month in total returns. That includes a few rolling up of the short call to keep the call strike above the stock price or in 1-2 occasions when the remaining value of the short call falls below 20% of the original sale price.

Since all this is rather new to me (although I have some good exposure to options), I would like to share with you what I have done hoping for some feedback/guidance from you. Is this ok?

Thanks again, Brian

Brian,

Happy New Year to you too.

My responses:

1. Once a trade is initiated, we do NOT close it based on its removal from our premium watch list. We use our exit strategy arsenal if those opportunities present themselves. If we do close a position, we use the most recent list to replace that security.

2. Yes, avoid earnings reports… very important.

3. Feel free to send interesting trades. I use these to share with the BCI community in the form of blog articles, “Ask Alan” videos and soon-to-be-launched podcasts. I obviously can’t evaluate entire portfolios for our thousands of members (thanks to all for that) but want to share all trades with educational value… we learn from each other.

4. If you feel that you would benefit from 1-on-1 mentoring, we do have an online coaching program run by Barry Bergman, BCI Managing Director:

https://www.thebluecollarinvestor.com/investment-coach/

Keep up the good work.

Alan

Hey Friends,

Well, between current events, market seasonality favoring metals over stocks, an election year, an impeachment “trial” and anything else you want to throw into the stew is everyone ready for an interesting year :)?

I have long advocated even in more “normal” times that from a position management perspective we enhance our flexibility greatly as options sellers if we choose stocks and ETF’s at price levels that allow us to diversify and still have budget space for 200 shares in each position.

Here is why: with each report Alan says what his ratio of ITM vs OTM strikes is for new covered calls. Tough to do with just 100 shares! Unless you spread it out over for 4 or 5 100 share positions. But if you can split it per position your flexibility goes way up in my opinion. If you have 200 shares of ABC you can write one contract ITM and one OTM. Or overwrite one and let the other 100 shares run free. How many times have you been left at the station holding a covered call when the train took off?

And if earnings are coming NEVER hold a stock covered in that week but what if you sold 100 to reduce risk of a bad report and kept 100 for a good one uncovered if nothing had changed news or fundamentally since you bought it? Your cash stock pile grows but you don’t miss a great report and a bad one hurts you half as much.

So you get where I am going with this: being able to flex tactics is valuable. It’s enhanced if you have 200 shares of any one position. I think positions are easier to manage one at a time than as an aggregate portfolio unless it is a one ETF portfolio like SPY or QQQ – which makes sense too, ironic as that sounds 🙂 If we are diversified outside a single ETF the dynamics of each holding will change often uncorrelated month to month. So it is helpful to look at them independently.

If they did not rotate one against the other the BCI lists would never change :)?! – Jay

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 01/03/20.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Best,

Barry and The Blue Collar Investor Team

barry@thebluecollarinvestor.com

Hi Alan,

I have a question about how to think about managing positions in a large account.

Thinking long term, I’d like to understand how I might manage a portfolio of $300,000-400,000.

Here are the basic questions I have.

– should I allocate an equal amount ($100,000) each week?

– what is the minimum/maximum days to expiration I should be using?

– how should I be thinking about managing the risk/reward for this size of a portfolio?

Thanks,

Patrick

Patrick,

My responses:

1. We must each determine the number of positions we are comfortable managing. For me, It’s between 15 and 25 per month. Let’s use 20 for my response with $400k available. That computes to $20k per position. We divide price-per-share into $20k and round the nearest 100 and that dictates how many shares to buy and contracts to sell. We make sure to leave at least 2% available for exit strategy opportunities.

2. I prefer monthly contracts and enter my positions on Monday or Tuesday after expiration Friday to avoid time-value erosion (Theta) of our premiums. We have some members that use Weeklys.

3. Risk can be managed in many ways. Setting our initial time-value return goal range is critical in that it will be directly related to the implied volatility of the underlying securities. For me, it’s 2% -4% per month. Go lower if more conservative or higher if more aggressive.

We can also manage risk by the “moneyness” of the options sold and by adding protective puts.

Detailed information on all these topics with examples are found in our BCI books and DVD programs.

Alan

Alan,

Great outline of your methodology.

Mario

Thanks Mario. I am extremely fortunate to have members (like Larry) who provide me with comments and questions that have fueled weekly blog articles like this one for over 12 years.

Alan

Alan,

thanks again for a perfect article.

This subject always mystifies me.

Rolling out makes perfect sense when your CC options went worthless on expiration Friday.

But, when the stock has gone above your strike, why not let the option be assigned (exercised), and realize your profit?

If you roll out, or out and up, you are losing threefold: First because you lose in the spread, second you will probably get a debit, and third, you take on a lot of risk, especially when the stock went a lot higher, which means there is a big chance that it may go down soon.

On the other hand, if you like it so much, and there is no ER before the next expiration, you can always buy it back in the following week (with the advantage of the new watch list on Sunday, and insight of the market trend), and sell the next cycle best CC option in accordance to your risk level.

Sorry if my comment is a bit rude.

Roni

Roni,

You make some important points (I would never use the word “rude” associated with you). Let me offer some points that offer another perspective:

1. There is no need to roll the option if the strike is OTM at expiration. We know that the stock will be in our portfolio on Monday and there is no need for an exit strategy in the current contract month. We can wait until Monday, evaluate the stock and the returns to make a decision whether to keep that security in our portfolio for the upcoming month.

2. When looking at the cost-to-close for an ITM strike, it is the time-value that we focus in on, not the total premium. Let’s say we bought a stock for $29.00 and sold the $30.00 call for $1.00 and the stock price is $32.00 at expiration and the cost-to-close is $2.05. Let’s also assume, we have concluded that we want to include this stock in the next contract month portfolio. Are we losing threefold?

– Spread: The time-value at expiration will decline to pennies ($0.05 in this hypothetical). The time-value for the next month option will be at a 1-month maximum. We benefit due to the logarithmic time-value erosion of near-the-money strikes (lowest at the start of the contract and greatest at the end).

– Probable debit- Yes, if viewing the total cost-to-close and comparing to the previous month’s premium rather the next month premium. In the above example, if we rolled-out, of the $2.05 total cost-to-close, $2.00 is intrinsic-value (bringing our share value from $30.00 (previous strike) to $32.00 (current market value)… that is a “wash” Let’s also hypothesize that the next month $30.00 call generates $3.00 ($2.00 intrinsic-value + $1.00 time-value). This means, we actually have an exit strategy time-value credit of $0.95 ($1.00 – $0.05) on a cost-basis of $30.00 (share value at the time of rolling decision) = 3.2% time-value initial return. So…. compare the time-value cost-to-close to the next contract month time-value premium, not the previous one as the intrinsic-value component is compensated for by share value increase.

– Risk from an appreciated stock- This is the purpose of the “What Now” tab of the Ellman Calculator. If we want to keep the stock (whether we roll near expiration or buy it back on Monday) and have concern regarding profit-taking, we can roll-out rather than out-and-up to capture the downside protection provided by ITM strikes. If we are still bullish on additional share appreciation, we can roll out-and-up to another OTM strike. We can tailor our exit strategy execution to the specific circumstances of this stock and its price chart.

– Allow our shares to be sold and buy back on Monday- If the strike is ITM at expiration, there is little chance that there was a a technical chart breakdown. Also, since there was or will be no earnings release prior to the next contract expiration, fundamentals are still bullish (barring unexpected negative guidance). So, rolling will be based on the calculations… once again we turn to the “What Now” tab. Waiting for the market to open on Monday, shares are purchased at the new price ($32.00?, higher?, lower?). If the calculations meet our initial time-value return goal range and we still want to use this security prior to expiration … if the deal is there… take it.

I would never tell others what to do. I have too much respect for our members to do so. Rolling exit strategies are available to us and we each must make decisions on which ones we utilize and how and when we use them. I hope I provided some food for thought related to this topic.

Roni, thanks so much for this excellent post. I plan to use it for a blog article or “Ask Alan” video in the future.

Alan

Thank you Alan for the prompt and detailed explanation.

This is a very important issue for me, and I do have difficukty in understanding the details.

Great lesson, and very apreciated.

Roni

Hey Roni,

I can’t add a thing to Alan’s comprehensive reply!

But I can second his comment that the last word I would ever use to describe your comments here is “rude” :)!

I have been in comment groups about investing like Seeking Alpha and others. Please, let me tell you, there can be people on those sites who are rude and beyond! But never here. Without exception this is the nicest group of people I have chatted with in this type forum and I am certain it will always be that way….

I think your strategy of letting ITM calls expire and having the stocks called is working for you. You get a fresh cash infusion for new buy/writes and you hit your trade target so stick with it! If they finish OTM you keep your shares, the loss protection or income if the stock went sideways worked and then decide what is next with due consideration for earnings reports and ex-div dates.

Best regards, – Jay

Thank you Jay,

maybe I chose the wrong word, and should have said “inconvenient” instead.

You are right about all the members who post in this forum, and that is why I love to participate here.

Thank you also for the positive advice.

Roni

Hi Alan

Happy New Year to you.

I bought your encyclopedia and enjoying working through it. Thank you!

I’m also trading now for real in covered calls after 2 months of paper trading.

I belong to various trading forums and this morning I saw this post from another trader stating that for covered calls, you don’t collect any premium at all unless you let the contract expire and that premiums are paid upon contract expiry.

I used TC2000 for paper trading and the above was not the case.

For real trading I am using Interactive Brokers – as I am only 2 weeks in, I have not yet rolled out/down etc or seen a contract expiry yet. Are you able to comment on the above please? Have you seen this remark before?

Many thanks,

Justin

Justin,

When we sell an option, the cash is generated into our account immediately and is ours to keep. The comment may have alluded to the fact that when we sell-to-open, the final outcome of the overall trade is yet to be determined. The 3 possible outcomes with the sold option are:

1. We close the short call by buying back the option

2. The option expires worthless (out-of-the-money)

3. The option is exercised and our shares are sold at the strike price

For beginners, it may appear a bit confusing on our brokerage statements in that the contracts sold appear in brackets appearing as a debit (yellow field in the screenshot below) and that is because these positions are “open” The cash, however, appears as a credit (brown field in the screenshot below).

Bottom line: When we sell an option and undertake a contract obligation, we are paid a cash premium that is ours to keep. The final outcome of the overall trade is yet to be determined.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Alan

Hi Allen

I like Disney, Microsoft and JPM stocks but i don’t have enough money to purchase 100 shares. Should i just start cost averaging in every month or just keep saving?

Eric

Eric,

Building up portfolio net worth is a topic I address in my book, “Stock Investing for Students” (used in 4 universities in the US as part of their finance curriculums). Once we reach a threshold $10 – $15k for ETFs or $35 – $50k for stocks, we can then turn to option-selling.

The process involves dollar-cost-averaging into broad-market, low expense-ratio mutual funds. Start with Chapter 6, “The Game Plan” and then read the entire book.

While capital is building, the educational process for option-selling can begin so that we can “hit the ground running” once we have adequate capital. Then we will have years and decades to benefit.

Alan

Hi Eric;

You can use LEAPS as a proxy for the stocks. This is not a conservative approach.

Regards;

Terry

Terry is spot on with both points:

1. Using LEAPS as stock surrogates is less expensive and requires less cash than traditional covered call writing.

2. The strategy, technically known as the “Long Call Diagonal Debit Spread” or, more commonly, the “Poor Man’s Covered Call” (PMCC) is definitely not a conservative strategy.

I would take Terry’s second point a step further. The PMCC is a strategy that should considered only by sophisticated and experienced investors who understand the pros and cons of all the moving parts of the strategy and have concluded that it is the right strategy for the investor based on personal risk-tolerance and trading style.

The PMCC strategy is detailed in our book, “Covered Call Writing Alternative Strategies” We also created a calculator geared specifically to this strategy.

Terry, thanks for your excellent points.

Alan

Alan,

Does it makes sense to roll ‘Weeklies’ on expiration Friday even if it’s clear that they will expire OTM? In the past I used to let the calls to expire worthless and sell new weeklies the following Monday. But if cost to close is only $0.01-0.02 (+ commissions) and we roll them in early trading hours on Friday the time value of the next week’s call will be higher than if we’ll sell it on Monday because it will have additional day (Friday) + weekend, and this additional time value will probably be higher than the cost to close OTM option. So in this situation rolling might be more profitable than just let the calls to expire worthless.

Sunny

Sunny,

I have spoken to market-makers about this very subject. Time-value erosion is based on calendar days but weekend erosion is factored in on late Thursday or early Friday. Therefore, the time-value loss by waiting until Monday is negligible, if anything at all.

Alan

Hi Sunny,

Alan’s answer is right on. Most market makers believe there is no decay over the weekend. I think that they mainly feel this way because it appears that no one has made real money by selling options on Friday and buying them back on Monday. If there were weekend time decay this strategy should be very profitable. If this kind of trading were taking place it would be obvious to the market.

I deal in a good many high probability weekly Credit Put Spreads. This strategy is basically bullish to neutral. Since the market seems to be more sensitive to bad news than good news I prefer to open my positions on Monday to expire on Friday. I can enter them as “saved” orders on Friday and then make changes if needed on Monday. Usually no changes are made.

Here is a link to an article on weekend decay that I believe to be pretty through.

https://sixfigureinvesting.com/2014/10/option-weekend-decay-and-volatility-annualizing/

Discussions like this are very relevant and educational, particularly in how we, our community, choose to make our decisions and adjust our strategies based on results.

By the way, the weekly Credit Put Spreads leave little time for exit strategies and I honestly haven’t figured that out yet.:)

I am working on formulas to see if I can automate the closing of the short leg, if necessary, by placing BTC orders simultaneously with the opening orders. If the short legs appreciates rapidly then the long leg generally rises although not so rapidly as it is further out of the money. I am trying to find the point where I experience the least amount of loss should the trade go against me.:)

Many thanks for your thought provoking post.

Hoyt