Covered call writing calculations should be as accurate as possible so that we can assess the success and feasibility of our trades. When we roll in-the-money (ITM) options out-and-up there is frequently an option debit which, on first glance, may make the trade appear to be a losing one. However, by factoring in the impact that rolling out-and-up has on our stock value will frequently shed a whole new light on these calculations.

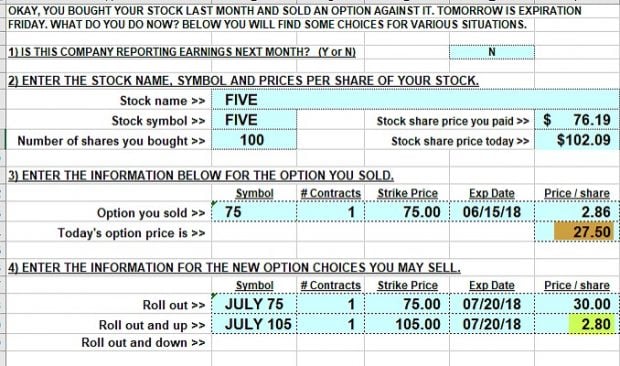

Real-life example with Five Below, Inc. (NASDAQ: FIVE)

- 5/21/2018: Buy 100 x FIVE at $76.19

- 5/21/2018: Sell 1 x June 15th $75.00 call at $2.86

- 6/15/2018: FIVE trading at $102.09

- 6/15/2018: Buy-to-close the June $75.00 call at $27.50

- 6/15/2018: Sell-to-open the July 20th $105.00 call at $2.80

Since an ITM option was sold for the June contracts, the maximum return was realized and now we must decide if rolling is a good choice. We will focus specifically on rolling out-and-up. On first glance, we see a huge option debit of $24.70 per-share ($27.50 – $2.80) … no way!

But what if we also factored in the impact rolling has on share value. Once we close the June short call, our share value moves from $75.00 (our option obligation to sell) to $102.09 (current market value). That represents a credit of $27.09 putting the rolling decision back into consideration.

Entering the information into the “What Now” tab of the Ellman Calculator

Rolling Calculations with The Ellman Calculator

- The brown cell shows the cost-to-close the June short call

- The green cell shows the premium generated from selling the July short call

Factoring in both the short call and long stock positions after rolling out-and-up

FIVE: Final Rolling Calculations

- Brown cells: Option credit

- Yellow cells: Option debit

- Purple cells: “Bought-up value of FIVE by closing the June short call

- Red arrows: Net initial time value + share appreciation initial profit

If the initial return on option + share appreciation of 3.14% with an upside potential and possible total return of 6.96% meets our goals, rolling-out-and-up should be given serious consideration.

Discussion

When we roll ITM options out-and-up, we must factor in the unrealized share appreciation resulting from closing the initial short call. This will give us a more realistic overview as to how the trade will impact our portfolio net worth. Once the position is rolled, we immediately enter position management mode.

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to share some of these testimonials in our blog articles. We will never use a last name unless given permission:

Alan,

I have taken your books out of the library and have listened to your videos. I am beginning a journey with you. Scary and exciting as it is all new. I love your clarity.

Alison

Upcoming event

July 22: Chicago Traders Expo

1:30 – 2:15

Hyatt Regency McCormick Place

August 15, 2019:San Francisco Money Show

9:15 AM – 12:15 PM

6 PM – 6:45 PM (subject to time change)

***********************************************************************************************************************

Market tone data is now located on page 1 of our premium member stock reports.

***********************************************************************************************************************

Alan,

How would you have handled this one.

I bot VEEV @ 165.99 on 6/17 and STO 165C 7/19 @ 7.10

On 6/26 with VEEV @ 157.68, I BTC @ 3.30 for 3.80 profit on call. ( I know, I know, I violated your 20% rule).

On 7/1, I resold option (165C 7/19) @ 4.01 Cr. (VEEV @ 163.78). Caught the bounce here.

Friday, expiration Friday, VEEV trades @ 172.06 with mixed technicals (20/100 EMAs positive, MACD negative). STC 165C 7/19 looks like 6.70/7.30 (I normally limit order at mid bid/ask with Schwab and get it most of time).

I was looking at either rollout or rollout/up to 8/16 (eps due 8/24) to either 165C @ 9.75 or 170C @ 6.65. The technicals suggest staying ITM.

What’s your inclination on this one?

Larry

Larry,

When we are considering rolling-out versus rolling out-and-up, we turn to the “What Now” tab of the Ellman Calculator (see screenshot below). Based on the information you provided, we have the following rolling choices:

1. $165.00: 1.67% 1-month return with 4.1% protection of that profit

2. $170.00 strike: 2.82% 1-month return with 1.2% protection of that profit

We evaluate our initial time-value return goals, personal risk-tolerance and make a call. It will vary from investor-to-investor. If neither return is appealing, we “allow” assignment and use the cash in a new position with a different underlying on Monday.

Great job using our exit strategy arsenal!

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Alan

Alan,

the June/July option cycle expired yesterday, and nine out of my ten positions were ITM, or deep ITM. (very happy).

Before expiration, I looked at the possibility of rolling out the tickers which will have earnings reports after August 16.

I noticed that, even though the time value of my options was nearly zero, the bid/ask spreads were fairly stiff — therefore I decided to let them be assigned, and realized some very nice gains.

Next week, if these tickers are still looking good, I can buy them back again, and write the 08/16 calls, no sweat.

I do not see the advantage of rolling when my short options are ITM.

Maybe I am missing something here? Please clarify.

Roni

Hi Roni,

9 out of 10… you’re leading the league in hitting! And you made my day.

Reasons an investor would opt for rolling rather than assignment:

1. If the “deal” is there, take it… prices can change.

2. One less trading commission.

3. In certain circumstances, tax considerations.

Reason #1 is the most significant.

Keep up the good work.

Alan

Thank you Alan.

Roni

Hey Roni,

All the regulars know you and I have been friends here a long time. So I think it is only prudent I warn you that if you keep having 9 out of 10 winning trades you will find it increasingly difficult to go broke. So please be careful with that :).

As far as your presenting question on whether to buy back and roll ITM covered calls I am on the fence on that one. Alan and Barry have crafted a masterful way to turn covered call writing into a flexible multi-dimensional strategy. I still regard it as a mostly bearish strategy. For grins if you had not sold a single call on your nine winning positions would your account be higher or lower? I suspect higher. But the puzzle is we never know so selling OTM calls every month evens out our returns.

This is where our psyche and knowing ourselves comes in. I can take loses but I hate leaving money on the table. So I almost never overwrite a full position, I don’t use ITM calls very often and I sell a lot of CSP’s on the things I like. But that’s just me.

The idea I suggest to anyone who listens to me is find, trust and be just you. – Jay

Thank you Jay,

I believe that my post was misleading.

When I said ITM calls, I meant that they were in the money on expiration Friday.

Actually, they were all OTM calls at the time when I sold them.

I always aim at good tickers, and buy/write OTM calls with ROO at 2% or better.

Sometimes, the CCs are ATM or near the money.

Then, I watch them very closely, and will unwind any trade that shows a loss of more than 2%, regardless.

This month was really exceptional, and I averaged 3.6%, which is fantastic, and rare.

You are right; If I had not sold any CCs, I would have certainly made much more money, but nobody knows what the market will do tomorrow, and therefore, the risk is huge when you just buy and wait. ( I can’t sleep when I do it: –When the stocks go down, I worry, and when they go up I get exited — so, no sleep either way).

In my opinion, money left on the table is worthless to me.

Roni

Hey Roni,

Your post was not misleading at all. Congratulations on a fantastic month using BCI methodology! You were up 3.6% which is 43% annualized and show me any mutual fund manager who claims that :)? We agree none of us can see the future, my comment had the gift of hindsight, I don’t fault anyone here who covers all positions systematically every month and I suspect those that do beat the S&P regularly. There is a lot of sleep at night value knowing that your stocks are creating monthly cash flow. Some months that is loss protection and other months it is income but it always helps.

In your case 9 of 10 stocks went up, you got income from your options and appreciation from your called stocks. Which was exactly your plan a month ago. Great job! – Jay

Thank you again Jay, you are a good and dear friend.

Roni 🙂

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 07/19/19.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are in Earnings Season, be sure to read Alan’s article, “Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The Blue Collar Investor Team

barry@thebluecollarinvestor.com

Alan,

What are your thoughts on having a protective put on PMCC LEAPS option? I plan to initiate trade on GLD buying Jan 20 $120 Call for a long leg. At GLD trading at $134.47 this will cost me $16.10 and Jan 20 $120 Put ask price is $0.32. So it would be a $16.42 total. I made some calculations and they show that the maximum possible loss when having a protective put in place will be limited to 40-60% of the LEAPS option value. And it will be realized around the strike price of $120, when both call and put options will consist of time value only.

My biggest concern is how to protect LEAPS option if GLD will go down. Paying only $0.32 per contract to hedge the possible losses looks like a good deal…

Sunny

Sunny,

I see no downside outside of a slightly lower return as long as the initial trade meets our required formula:

(Difference between strikes + short call premium)] > (Cost of LEAPS + Protective put)

In the PMCC Calculator include the cost of the protective put in our cost-basis. You should find a few strikes choices.

Good idea for a blog article or Ask Alan video… what would I do without members like you!

Keep up the good work.

Alan

Hi Sunny,

I am intrigued by your planned trade.

I have been thinking about a similar strategy.

Some thoughts:

GLD is at a height not reached since August of 2013. GLD has under performed the S&P since that time(Aug 2013). Typically GLD goes up when the S&P goes down, but not always. GLD really ran up in 2011 & 2012($177 & $172).

If Dr. Jay is right(see immediately previous blog), and I suspect he is, then we could easily see a 5% correction in the S&P in the month of August. Such a move would normally create a similar rise in GLD putting it at around $140.

In my opinion a bullish bet on GLD is a bearish bet on the S&P. If my assumptions are near true then I think the short call should be Aug 30 where strike premiums more than cover the PMCC formula. I would probably close all legs when the short call became ITM.

Here again, this is just one man’s opinion and, of course as with all positions this one would should be closely monitored. But you have set up what I think is a highly probable profitable trade.

To paraphrase Paul Kangas, “Here’s wishing you the best of good buys.”

Hoyt

Thanks for the honorary Doctorate, Hoyt, though I have done nothing to deserve it :)!

Should Alan’s comment from Chicago below play out and we get a rate cut next month I suspect it will disrupt the “normal” seasonal patterns. This time of year being short SPY and long GLD and TLT usually works.

But rate cuts are like rocket fuel for stocks so perhaps not this year? TLT might still work. Buying October calls at maybe $132 strike today then selling monthly calls for Aug, then Sept and finally Oct above it OTM to offset theta decay and recoup a little of the call cost would be a decent trade requiring no more option clearance than a PMCC. Sort of a hybrid on a PMCC.

It might be a nice way to gain if Treasury prices go up in the months ahead without paying full price for TLT. – Jay

Jay,

Getting ready to go to the Biergarten. Had TV on CNBC. Tony Dwyer was predicting a 5% drop in S&P with a snap back towards mid September.

I was really surprised by up market today. Breaking news: debt ceiling raised for two years.What that will mean? I have no idea.

On another front I took a flyer on Sunny’s proposed trade at about 11:00 – 11:15.

Bought GLD Jan 17 ’20 $120 Call @ 15.96

Bought GLD Jan 17 ’20 $120 Put @ 0.28

Sold GLD Aug 30 ’19 $137 Call @ 1.75

Will let everyone know how it goes.

Hoyt

Hoyt,

Please enjoy a nice time at the Biergarten with the folks and solve all the world’s problems in a sitting while you are there :).

I see what you and Sunny are doing with GLD and I like it. You are hedged long, your hoped for outcome is higher gold prices and you are selling shorter dated calls over top of it to bring down cost basis of the trade. Smart.

Tony Dwyer was just taking a page out of the seasonal play book. I was there with him a couple weeks ago. But I think Powell may rain on his bear parade. If he doesn’t I will be buying any big dips next month because Trump won’t let that last long into next year with his re-election on the line.

I wish I was smart enough to come up with a better answer to the can kicking ritual on the debt ceiling that would fly politically.

But it’s just not reasonable to think anyone in Congress whose career is up for vote every two years will ever bite the bullet and make tough choices to fix it. – Jay

Hoyt T,

Personally I don’t try to predict markets, I use GLD and TLT for portfolio diversification as historically both, GLD and TLT, has negative correlation with stocks (even if they all move the same direction the recent months).

I’m interested in further research of protective puts on PMCC, I find this idea worth consideration, just need to experiment more with different strikes selection to better understand the mechanics behind this strategy.

I think GLD and TLT are perfect candidates for PMCC. They are less volatile than SPY or QQQ, so are better suitable for leverage. Also both are very liquid and bid/ask spreads are very narrow, so we don’t lose much when buying and selling LEAPS.

Hope your trade will go well, I setup mine yesterday too, but I chose much shorter expiration date (Aug 02) and the lower strike ($135). Long call/put are the same as yours.

Sunny

Sunny,

Thanks for your reply.

You are right in not predicting the markets. For decades I did not. I was always 100% invested in equities. I was able to set up my 401-K where I could self direct, something that was near impossible at the time. The great recession of 2007-2009 cut my seven figure account in half. I was 65-66 at the time. I thought I was too old to recover from that. Fortunately that was not true.

I count my Social Security and fairly substantial real estate holdings as my “Bonds” thus I have been 100% in the stock market with equities and options. I have 7 core holdings, 5 of which I overwrite from time to time.

At my present age, 77, I only stay active in the market because I love it and it keeps me sharper that the crossword puzzle or Solitaire.:)

I also don’t want to go through 2007-2009 again and this has been a long bull market. Tariffs help bring on the Great Depression, see Smoot-Hawley, so I have gone to 10% cash and I am slowly building that to 25% as I close out various LEAPS. I have used LEAPS as stock substitutes and in this bull market they have given me a better return than owning the stocks. I might add that I only trade in my tax qualified accounts.

Overwriting them with covered calls is something I have only done in the last two years. Never thought of it. It works well too. I also am intrigued by the idea of protective Puts. As a matter of fact, Puts in general. I have always been a Call guy but have taken some courses at CBOE on Puts and better appreciate their utility than I did before.

As many have said before me, this blog is fantastic. Not only do we learn from Alan, Barry and others, there is something psychologically rewarding, or re-enforcing, by being a part of a community of fellow travelers. Shakespeare understood this.

Again, thanks for your input and I, for one, would appreciate and look forward to more from you.

“Wishing you the best of good buys.”

Hoyt

Alan,

I know ITM calls offer downside protection and as you say in your books and ask Alan series, our return is guaranteed as long as the stock stays above our ITM call. Also, we manage declines using the 20/10 rules. In a response to someone on FB you said most get out with 10% loss to manage risk.

My question: is it a good strategy to put in a closing order on a position should the stock decline to the ITM call strike?

Obviously your gain would be reduced as there is still time value remaining but you wouldn’t lose anything much. However, stocks can cycle during the month and still end up in a good position so you might get stopped out unnecessarily. I would be interested in your thoughts on this.

JD

JD,

I firmly believe in the 20%/10% guidelines as when to close the short call… not the price of the stock. The caveat, of course, is when egregious news comes out, a position can be closed at any time.

When a stock declines to the (formerly ITM strike) now ATM strike, we are at a breakeven in the stock side of the trade (using the intrinsic value of the initial premium to “buy-down the cost-basis of the stock). However, we still have an unrealized profit on the option side. Since ATM strikes have a higher time-value component than ITM strikes, we may lock in a losing overall trade depending on the time to expiration.

After buying back the short call with the 20%/10% guidelines, we can make a decision to wait to “hit a double”, roll-down or sell the stock using the guidelines detailed in my books & DVDs.

Alan

To the BCI community:

I’m in Chicago for a seminar I’ll be presenting at the Trader’s Expo this afternoon. A speaker here alluded to a tool developed by the Chicago Mercantile Exchange (CME Group) that calculates future Fed actions based on Fed funds futures contracts. As of today:

70% chance of a 25-basis point decrease

30% of a 50-basis point decrease

0% chance of nether

Time will tell.

Alan

Back home from the windy city.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Hello Dr. Allman.

I have a question about Covered Calls. Why do a Covered Call? Why not do a Call Or Put?

Thanks

Oren

Oren,

Covered call writing is a lower-risk strategy than buying or selling (naked- without first buying the stock) calls. Selling calls lowers our cost-basis (breakeven). Buying calls raises our BE but provides the opportunities for big winners.

Conservative investors will migrate to covered call writing over buying calls. More aggressive investors may buy calls for the opportunity to “hit it big” I would advise against selling “naked” calls. Our brokers will not allow it in most retail investor portfolios.

Alan

Everyone,

Is it just me or my computer or is everyone fining the BCI website, particularly the blog, to very slow and erratic?

I don’t seem to have this problem anywhere else.

Hoyt

Hoyt,

I noticed a little glitch earlier this morning but seems ok now.

Marsha

Marsha,

Thanks.

My problem is typing in a reply. The copy doesn’t show as I type. Fills in later, much later sometimes.

Hope the market treats you well.

Hoyt

Premium members:

This week’s 8-page report of top-performing ETFs and analysis of ALL Select Sector Components has been uploaded to your premium site. The report also lists Top-performing ETFs with Weekly options as well as the implied volatility of all eligible candidates.

New members check out the video user guide located above the recent reports.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

Hi Alan,

I made it through your Encyclopedia and thought to start my membership in August. Unfortunately I am so busy making cheese these days, that I only have a few spare minutes to dedicate to the subject before I fall asleep. By September I should be able to dedicate more time to covered call writing. In the meantime I would play around with it on the paper trading account.

I saw that capital gains on stocks held less than one year Italy wants more than 30% on the gains. Therefore I would need to figure out a way to not have stocks called away by accident.

I would appreciate any kind of advice you could give me on this issue.

The other thing I am a bit worried about is the economy in general. My understanding is that the cheap money pinned out by the central banks over the last decade and the rest, most likely coming down the pipe in the near future, set the stock market on steroids. How long can this last? What options do we have once this whole thing goes South? Eventually it has to, doesn’t it?

Thanks for your thoughts.

Dietmar

Dietmar,

You are addressing 2 main concerns: tax and bear market concerns:

1. Tax: First, check with your tax advisor and factor that in to a much greater extent than any comments I make. In the US, some of us have opportunities to trade in sheltered accounts which defers or eliminates tax concerns. How about in Italy? That said, I would suggest reading all the “portfolio overwriting” information disseminated in my books and DVDs:

Best book:

https://thebluecollarinvestor.com/minimembership/covered-call-writing-alernative-strategies/

Best calculator:

https://thebluecollarinvestor.com/minimembership/portfolio-overwriting-calculator/

We use only out-of-the-money strikes that meet our initial time-value return goals. Ex-dividend dates must be factored in.

2. Bear market concerns:

Some economists feel that the increase in the deficit created by the recent US tax plan will ultimately lead to a recession. Interest rates are historically low and probably getting lower before they are restored closer to higher historical levels. Rising interest rates will impact the stock market negatively as other investment vehicles become more attractive. This may or may not result in a bear market. Even if we enter a bear market cycle, we can still craft our strategies for success based on current market conditions. Here are links that address this matter:

https://www.thebluecollarinvestor.com/how-to-generate-10-per-year-in-bear-markets-by-selling-stock-options/

https://www.thebluecollarinvestor.com/comparing-covered-call-writing-and-put-selling-in-bear-markets/

There is nobody who can time the market accurately 100% of the time. However, we are taking on short-term obligations which allows us to re-evaluate our bullish security assessments every month (or week) as well as appraising the current market outlook.

Alan

Deitmar,

Tax concerns :

We have simillar concerns here in Brazil (25%) on one year gains.

But there is no way to avoid it.

You must think that if you are lucky and successful, and make 15% on your portfolio in one full year, 30% x 15% = 4.5% for your government, and 11.5% for yourself.

Not bad when you consider the banks, which will give you less than 2%.

Roni

Hi Alan,

Instead of rolling-out to $75 or rolling-out-and-up to $105, what is your opinion in rolling-out-and-partially-up to, let’s say $90 or $95 (or any strike price in between)? It would cost less to move up, and particularly if I think the stock might have topped and would move side-way in the foreseeable future.

Van

Van,

Absolutely. The 2 strikes presented in the article are examples of scenarios, one that probably does not meet and another that probably does meet a typical investor’s option-selling goals.

We use the “What Now” tab of the Elite version of the Ellman Calculator to check other strikes to determine which best suits our individual time-value return goals.

Alan