Covered call writers and put-sellers are always looking for an edge. Some may wonder which option Delta would make the best option-selling candidate. Intuitively or from experience we know that at-the-money strikes (Deltas near 0.50) generate the highest initial returns. I’ve stated that over-and-over again in my books and DVDs. Can this be demonstrated mathematically (look out folks, I’m at it again!)? Today’s article will be an exercise, not a scientific study, to demonstrate the relationship between Delta and our time value initial profit generated when selling options. Our goal is to calculate the time value per unit of Delta for in-the-money, at-the-money and out-of-the-money strikes.

Exercise set-up

- Select a stock from our Premium Watch List: Smith & Wesson Hldg. (SWHC)

- View an options chain for in-the-money, near-the-money and out-of-the-money strikes

- Use the time value premium of each strike and a Greek Calculator to quantify the Delta for each strike

- Divide the time value by the Delta to calculate time value per unit of Delta

- The proposed formula is TV/Delta

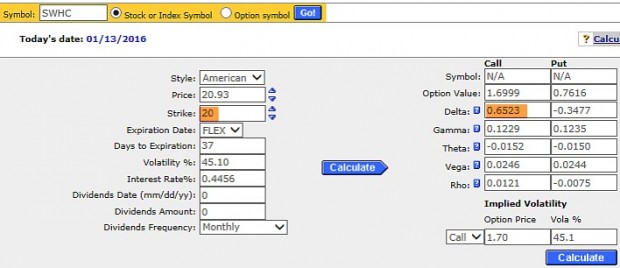

Options chain for SWHC as of 1/13/2016

Options Chain for SWHC

With SWHC trading at $20.93, we select the $20.00, $21.00 and $22.00 strikes which generate premiums of $1.70, $1.20 and $0.75 respectively. Now the $1.70 premium for the $20.00 strike consists of intrinsic and time value so we deduct the $0.93 of intrinsic value to get a time value of $0.77 for the $20.00 in-the-money strike (are we having fun so far?). The other two strikes are all time value.

Calculating Delta for the $20.00 in-the-money call

Calculating Delta for the $20.00 Call

Delta = 0.6523

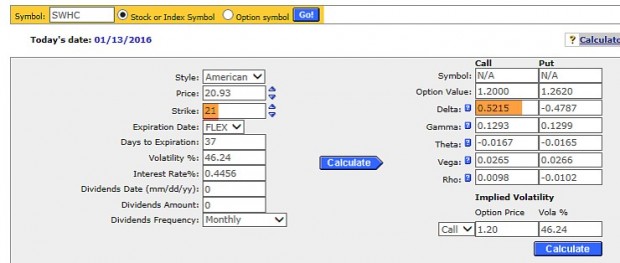

Calculating Delta for the $21.00 near-the-money call

Calculating Delta for the $21.00 Call

Delta = 0.5215

Calculating Delta for the $22.00 out-of-the-money call

Calculating Delta for the $22.00 Call

Delta = 0.3899

TV/Delta

$20.00 strike: $0.77/0.6523 = $1.18 per unit of Delta

$21.00 strike: $1.20/0.5215 = $2.30 per unit of Delta

$22.00 strike: $0.75/0.3899 = $1.92 per unit of Delta

Observation

The $21.00 near-the-money strike generated the highest time value per unit of Delta while the in-the-money and out-of-the-money strikes were both lower. Deltas near 0.50 will generate the highest time values and that figure will decline as Delta moves to 0 or to 1.0. Although this exercise is not in the galaxy of a scientific experiment, I would expect, based on our knowledge of Delta and option premiums that this could be duplicated over-and-over again.

Discussion

Lower Delta options should be favored in bear (in-the-money calls) and bull (out-of-the-money calls) markets based on the moneyness of the options. In these two scenarios we can take advantage of upside potential and downside protection afforded by these strikes. If we were convinced that the market is consolidating and trading sideways, high-Delta options may be more appropriate.

Blue Hour Webinar registration is now open to Premium Members

Registration for the July 28th Blue Hour webinar is now open to Premium Members only. This event is free to members. Once you are registered, you will receive instructions regarding how to attend this event and will be given an opportunity to submit a question.

To register, login to the member’s site and scroll down on the left side below the store discount link. Then click on the Blue Hour sign-up link and fill out the short registration form. For members who cannot attend the event live, my team will be recording the webinar and it will be posted on the member site the following week.

The BCI team and I are looking forward to providing this new educational tool to our members and happy to make this a free resource for our loyal members. On September 1st, there will be a rate increase for new members but you will be grandfathered into the current lower rates as long as membership remains uninterrupted.

Thank you for your loyal support over the years.

Alan and the BCI team

____________________________________________________________________

Next live event- Workshop

July 16, 2016

American Association of Individual Investors

Washington DC Chapter

Northern Virginia Community College

9 AM – 12:30 PM

Seminar information and registration link

___________________________________________________________________

2 Florida seminars just added

| Delray | 3/21/2017 |

| Ft Lauderdale | 3/22/2017 |

1 New York seminar just added

Long Island, NY 5/9/2017

Market tone

Global were generally flat this week with continued Brexit fallout and concerns over the state of the Italian banking sector. Oil prices fell and The Chicago Board Options Exchange Volatility Index (VIX) declined to 13.23 from 15.16 last week. This week’s reports and international news of importance:

- May payrolls were revised lower, to 11,000 from 38,000 while June payrolls were far stronger than projected, rising 287,000, over 100,000 more than expected

- The economy averaged 149,000 new jobs per month in May and June, a figure that will give the FOMC more incentive to raising rates later this year

- With the Bank of England indicating last week that it will likely ease monetary policy over the summer, the pound extended its decline on the foreign exchange markets this week, falling to a 31-year low of $1.2780 on Wednesday and ending the week slightly below $1.3000

- Several open-ended funds investing in UK commercial real estate have been forced to halt redemptions and dramatically mark down their holdings as investors seek to withdraw funds

- Minutes of the June Federal Open Market Committee meeting released this week show that rate setters were in no rush to hike rates

- The committee also cited the uncertainty surrounding the Brexit referendum, which took place a week after the meeting, as a reason to hold rates steady

- Many Italian banks are saddled with crippling amounts of bad loans, but bailing them out with government money is not an option until bond holders first take a hit, according to European Union rules

THE WEEK AHEAD

- The Bank of Canada holds a rate-setting meeting on Wednesday, July 13th

- The US Federal Reserve releases its Beige Book on Wednesday, July 13th

- The Bank of England Monetary Policy Committee meets to set rates on Thursday, July 14th

- China releases gross domestic product and retail sales data on Friday, July 15th

- The US releases retail sales data and it’s Consumer Price Index on Friday, July 15th

For the 4-day week, the S&P 500 rose by 1.83% for a year-to-date return of +4.21%.

Summary

IBD: Market in confirmed uptrend

GMI: 6/6- Buy signal since market close of July 1, 2016

BCI: Moderately bullish. Currently hold no short option positions due to the Brexit situation but fully invested in stocks and ETFs. Pending market action this coming week, my plan is to favor out-of-the-money strikes for the August contracts.

WHAT THE BROAD MARKET INDICATORS (S&P 500 AND VIX) ARE TELLING US

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 07/08/16.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are in Earnings Season, be sure to read Alan’s article,

“Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The Blue Collar Investor Team

Alan,

Do you have a rule as to how far in the money or out of the money we choose when bullish or bearish?

Thanks for your help.

Dara

Dara,

Yes but I prefer to categorize these as “guidelines” rather than hard-and-fast rules. The protocol is to set our goals first. For example, in normal market conditions, my goal for initial, 1-month time value returns (ROO) is 2-4%. When selling ITM strikes, I look for strikes that generate these returns and give the greatest amount of downside protection. When selling OTM strikes, I look for strikes that meet my ROO goals and offer the greatest amount of upside potential. In consolidating (sideways) markets I move closer to ATM strikes.

Alan

Just getting back into covered call writing and looking over IBD top 50 was it not 100 at one time? thanks Peter S

Peter,

Yes, absolutely. A few years ago IBD changed the long-time IBD 100 to the IBD 50. Their rationale was that by including only the top 50, the list will consist of higher-quality candidates. As a result it became even more important to consider other resources in addition to the IBD 50 to generate eligible option-selling candidates. The BCI team has a database of over 3000 stocks we screen for our premium members in addition to the IBD 50. Another (free) resource is http://www.finviz.com.

Alan

Peter,

A managed ETF on the market since April of ’15 is FFTY which trades the IBD 50. It’s expense ratio is .8 and higher than you would expect for an ETF but it is managed and does not equal weight the IBD 50.

It’s too new/ small to be optionable, had a rocky intro but it has beaten SPY since Brexit. It may warrant a spot on your watch list if you follow IBD 50 and want a one-stop exposure to that group of stocks which evolves constantly. -Jay

Jay,

Very interesting. Thank you for the heads up.

Best,

Barry

Well, thanks Barry. Any time I can give you an idea I feel great because I am still deep in the hole compared to ideas you have given me :). – Jay

Jay,

Definitely worth keeping an eye on this security as the IBD 50 is a mainstay in the BCI screening process. If management consistently beats the market, options will come. We need to keep an eye on daily trading volume which currently is about 16,000 shares per day below our 250,000 requirement. This, too, should be overcome if management beats market benchmarks.

Thank you Jay.

Alan

Hi Alan

I very much enjoy your writings,and have read all of your books. I also enjoy our occasional correspondence.

I am very interested in both of your 3/17 Florida seminars.

I assume they will essentially be the same?

How can I obtain more info, and sign up?

Thanks so much for all of your great work and many courtesies.

Ron,

These are both chapters of “The American Association of Individual Investors” I was invited to speak at both venues in 2014 and presented my basic covered call writing seminar. In next years seminars, I anticipate covering both covered call writing and put-selling. I do anticipate both seminars will be the same. I will post the registration links when I receive them from the clubs (managed by the investment clubs, not BCI). That will be in January-February, 2017.

I hope to see you there and thanks for your interest.

Alan

Alan and Barry,

Thank you both for all of the work that you do. My premium membership has been worth every penny, I’m up 17% in my IRA since January by trading the BCI system.

I am interested in learning how to use in-the-money Bull Debit and out-of-the-money Bull Credit spreads. It seems that the bullish nature and higher option premiums for most of the stocks on the premium watch list would make them good candidates for these trade types.

Do you know a good resource for learning the target RoO’s, exit strategies, and general rules of thumb for spreads? If your group ever offers a book or class on Bull spreads then I’ll be the first one in line to buy it.

Thank you again for the work that you do.

Caleb,

Trading credit and debit spreads is definitely on our (long) list of things-to-do but not at the top of that list. We are currently working on The Blue Hour webinar series and developing additional trading tools (trade planners, expanded calculators etc.) to facilitate the efficiency and success of option-selling trades for our members. I am also 200 pages into my 7th book (Encyclopedia 3) which I hope to publish in about 2 years. We base our priorities on feedback we receive from our members. In the interim, check out http://www.optionseducation.org for information on spread trading.

So glad to learn of your recent success and thank you for your generous comments.

Alan

Alan,

I’m glad to hear that spreads are on the list, but very sad that they’re farther from the top. It’ll be great to see what you have planned to help facilitate trading.

You’re very welcome for the comments. I’ve been amazed at how well you have broken down your covered call methodology. It has been very easy to follow.

Caleb,

Anyone who is up 17% YTD in an IRA using the conservative strategies Alan and Barry research and teach is to be congratulated: great job!

I too have asked Alan about spreads and understand the same reasonable answer he gave you: they are on the work list but the barn is not exactly on fire :).

I use them all the time. They were a natural outgrowth of my interest in options income once comfortable with covered calls and cash secured puts.

You may be a mile ahead of me on the learning path regarding spreads. So please take this as just sharing from another traveler on the road. We likely have other friends who read this blog interested in this subject who are new to the strategy.

First, I understand Alan’s polite reluctance to engage this topic. It is complex. It is laden with land mines. It requires higher level option clearance in your IRA. I have Level 3 to do my spreads.

And it will break your spirit if not your heart and your account if you approach it emotionally without a thorough examination of your new love before risking money :).

Many of the unsolicited e-mails I delete each morning without opening are from services trying to sell me subscriptions promising weekly income. It is like the Siren’s call in Homer to lure ships onto the rocks!

Interest rates are near zero. Who does not want more income? Look at the rise in the XLP, XLU and anywhere else dividends are prominent.

The every morning e-mail solicitors are selling credit spread services. Many with the best of intentions and documented track records. I subscribe to one so I cast no stones!

My point is anyone interested in supplementing their covered call cash flow with credit spreads should please first remember Alan’s methods are already income oriented and less risky than spread trading.

Then do your homework and paper trade the heck out of credit spreads first! – Jay

Jay,

Thank you for the congratulations. It’s very exciting to have found success. The hard part is remembering that this has been a relatively bullish year, so I have to prepare to react accordingly to a bear market.

I certainly am not ahead of you in spread trading. What kind of success have you had? There must be a spread trading strategy that combines a few strong rules of thumbs and “common sense” ideas.

As Blue Collar Investors, we already use the best stocks in the world and combine them with strong technical analysis and market trends. It should be possible to take a stock from the watch list with strong technical indicators and create an in-the-money call debit spread for a 6%-8% return and a 5-10% cushion.

Caleb,

I would say my spread trading is a work in progress with good weeks and not so good weeks!

The biggest mistakes I made early on were taking excess risk, selling spreads on too many different under lying and not using exit strategies soon enough.

Now I take smaller positions, I focus on the S&P using SPY or SPX, I take early profits and I close and roll when my sold strike is touched. Those steps have improved my results.

Your idea about using stocks off the list should work. It is best to use ones with high liquidity/volume and ones you have some history with so you have as good a sense as possible of their patterns given none of us know what the future holds! – Jay

Caleb,

You have done wonderful !! 17% is glory, and you did it using Alan’s low risk method, aiming at 2% – 4% consistent gains.

So, why take greater risk with spreads, trying to get 6% – 8% gains ??

I believe we have plenty risk as it is.

We have the European mess, China, Islamic terror, the US economy, the FED, Donald Trump, the strong Dollar, oil prices volatility, banks beeing punjshed for 2008 crash, technology replacing workers, etc., etc. etc…..

The beauty of Alan´s covered call method, is exactly the risk/reward equation, which gives you a small edge over any other type of trade.

Beware, there are no magic rules of thumb

Roni 🙂

If one were to make covered call writing/buy-writes an income strategy, what discount online broker do you recommend? I would imagine it would be one that has a low or zero assignment fee. Please advise. Thanks.

Mai,

There is a free file of online discount brokers located by clicking the “Free Resources” link on top black bar of this web page (asks for your email address).

I do agree that I would research for brokers that do not charge an additional assignment fee over and above the normal commission for selling a stock.

Alan

Alan,

If I understand you correctly only the stocks on this week’s list with September option expirations, or later, would be eligible. It doesn’t seem to make sense to sell covered calls on stocks that will go gold (gold cells) next week. Am I understanding this correctly?

Thanks,

Peter

Peter,

That is correct but let me add:

1- Stocks ELS through T report in the 1s week of the August contracts and will become eligible after the reports pass.

2- All EFTs are eligible

3- All stocks that report after August 19th are eligible for the August contracts

4- I would wait for the new report to be published this coming weekend before entering August contract trades so we have the most up-to-date information.

Alan

Alan,

Your website is really informative and I am grateful for the site. I would like to ask if you can do split stocks on covered calls and cash secured puts and how that can be done.

Thank you in advance.

Best wishes,

Loise

Loise,

Yes, you can dedicate a portion of your portfolio to each strategy (although it may be simpler to select one or the other)or even better use put-selling to enter a covered call trade by starting with selling out-of-the-money cash-secured puts. I’ve given this strategy the name “The PCP Strategy” or “Put-Call-Put. For detailed information see Chapter 16 in my book, “Selling Cash-Secured Puts”

Alan

Hi Alan!

Thanks for the article. Question: in your TV/Delta comparison above, it looks like there is an error? According to your example chain, shouldn’t the $20.00 strike price result look like this:

$20.00 strike: $1.6999/0.6523 = $2.60 per unit of Delta

(instead of the “$0.77/0.6523 = $1.18 per unit of Delta” that you wrote… where does the $0.77 figure come from in your $20.00 strike price chart?)

Thanks in advance!

Bobby

Bobby,

The stats in the article are correct. The $0.77 comes from calculating the time value component in the $1.70 premium for the in-the-money $20.00 strike. Since that strike is $0.93 in-the-money (lower than current market value of $21.93), the intrinsic value of $0.93 is deducted from the total $1.70 premium = $0.87.

Alan