When we write covered calls or cash-secured puts, we are selling volatility. The time value component of a short-term option premium reflects the amount of time until expiration plus the volatility of the underlying security. Since most of us are comparing options with similar expirations, the volatility of the stock or exchange-traded fund represents the distinguishing factor in our option sales. In this article, we will review all aspects of volatility and bring this information into our world of option-selling.

What is volatility?

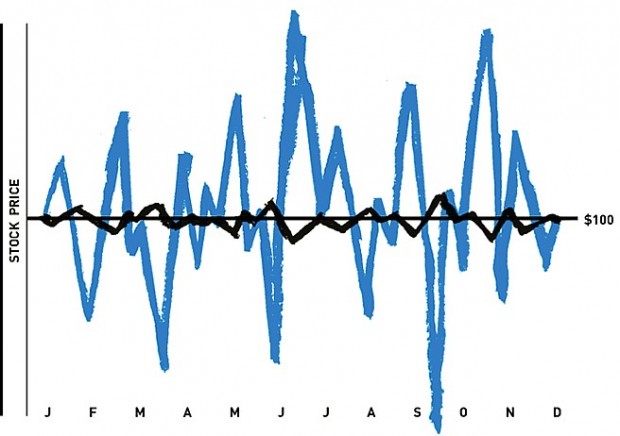

Volatility represents the price movement of the underlying security with no predilection to direction. It is an annualized statistic quantified as one standard deviation price change. This tells us that the statistic is projected to be accurate 68% of the time. This means that if a $60.00 stock has a volatility of 25%, it is expected to fall in the price range of $45.00 to $75.00 over one year 68% of the time. Two stocks that start and end with the same price over a one-year time frame can have very different volatilities as shown in the chart below:

Comparing volatility of two stocks

Although both securities started and ended the year at $100.00, the “blue” stock has much greater volatility and will generate higher option premiums at the expense of being a riskier underlying security. Each investor must determine the amount of volatility appropriate for their personal risk tolerance. For me, I have a goal of 2 -4% for a near-the-money one month expiration. In bull markets, I’ll go a bit higher. The question we should ask ourselves is “how much volatility should I sell?”

Types of volatility

Historical volatility: The actual price fluctuation as observed over a period of time, usually one year.

Expected volatility: This is a prediction of future price movement in either direction and is totally subjective. This is the least significant of the three types of volatility.

Implied volatility: This is a prediction of the underlying security’s future price movement based on the option’s price in the marketplace. For short-term option-sellers, this is the most significant of the three types of volatility. An event like an upcoming earnings report can render the implied volatility much higher than the security’s historical volatility.

Impact of volatility on our option premiums

An increase in volatility will increase the value of both call and put options and a decrease in volatility will cause a decline in both call and put premiums.

The role of Vega

Vega is the amount an option price will change given a 1% change in implied volatility. Let’s say that company BCI has an option value of $4.00 and a Vega of 0.06. The current value of one contract is $400.00. If the implied volatility increases by 1%, the option value for the contract will be $406.00. If the implied volatility decreases by 2%, the value of the contract will become $388.00, all other factors remaining the same.

Impact of Vega and the “moneyness” of options (for every 1% change in volatility)

In-the-money options: Have the least amount of time value and therefore the smallest dollar and percentage changes.

At-the-money options: Have the greatest time value and the largest dollar changes.

Out-of-the-money options: These are all time value and therefore the highest percentage changes.

Discussion on incorporating volatility into our option-selling strategies

As covered call writers and sellers of cash-secured puts, we are selling volatility. For our short-term positions, implied volatility is the most most significant of the three types of volatility because it reflects the current market assessment of future price movement of our underlying security. A great starting point for incorporating volatility into our trading decisions is to set return goals based on personal risk tolerance. A conservative starting point may be 2-4% per month for near-the-money strikes. Extremely high or low implied volatilities will not meet this standard. Goals can be tweaked based on your objectives and risk tolerance. Once size does not fit all!

Blue Collar Scholar Competition: Great prizes and a worthy charity

We’re trying something new thanks to Jay’s idea. Here are the parameters we are using: Two contests running simultaneously with six prizes:

Contest #1: What will be the value of the S&P 500 by year’s end?

Contest #2: In five sentences or less, give your reason(s) for your response (subjective, voted on by the BCI team)

Prizes in each category (total of 6).

Donation to the USO (United Services Organization) of $5000.00 worth of books.

Click on this link for our contest video and entry form.

Contest results to date

Outlook

% bearish: 8%

% neutral: 41%

% bullish: 51%

Sample Commentary from Arturo S:

Because in a 100 day chart there was a “W” formation and it hit that amount 3 times already. Knowing it’s about the end of the year, people will be cashing in on this bullish scenario.

Thanks for the great response we’ve had to this event. Keep those entry forms coming. We allow two per email address and the deadline is November 30th.

I’ve been remiss in not saying this in a while

A special thanks from me the entire BCI team to our premium subscribers for making these reports and tools a success beyond our wildest dreams.

Next live appearance

American Association of Individual Investors National Conference

Bally’s Hotel

Las Vegas, Nevada

November 7th – November 9th

Sunday November 8th @ 8:30 AM – 9:45 AM (Alan’s seminar in Bronze Room)

Exhibit Hall # 313

***Event is sold out

Market tone

Major global stock markets were neutral this week on mixed economic data. Growth in Europe offset weakness in China, while US data was generally bullish especially Friday’s jobs report. Asian stocks rose, with the Shanghai Composite Index gaining 20% since its August low, signifying a bull market. This week’s reports:

- US nonfarm payrolls grew by 271,000 in October, exceeding the median consensus of 180,000

- The unemployment rate fell to 5.0%, the lowest since April 2008

- Average hourly earnings rose by 0.4% from September and were 2.5% higher than a year earlier. It was the highest year-over-year wage increase since 2008

- The U-6 rate, which measures underemployment fell to 9.8%, a seven-year low. After the stellar payrolls report and comments by US Federal Reserve Chair Janet Yellen on Wednesday, a December rate hike is now more probable

- The US trade gap narrowed to a seven-month low in September as US oil imports fell to their lowest level in more than 11 years. The deficit narrowed to $40.8 billion in September from $48 billion in August

- US light vehicle sales increased 13.6% in October from a year earlier. For a second consecutive month, the annualized sales pace exceeded 18 million, the best two-month stretch in 15 years. The auto market is on pace for its strongest annual results ever

The Institute for Supply Management’s non-manufacturing index rose to 59.1 in October from 56.9 in September. The US service sector has expanded for 69 straight months- The ISM manufacturing index fell from 50.2 in September to 50.1 in October, the weakest reading since May 2013

- US labor productivity unexpectedly rose at a 1.6% annualized rate in the third quarter

- Initial jobless claims increased 16,000 to 276,000 for the week ending October 31st

- Continuing claims increased 17,000 to 2.16 million for the week ending October 24th

For the week, the S&P 500 rose by 0.95% for a year to date return of 1.96%.

Summary

IBD: Confirmed uptrend

GMI: 6/6- Buy signal since market close of October 19, 2015

BCI: Cautiously bullish using an equal number of in-the-money and out-of-the-money strikes. I will remain cautious but fully invested until after the December Fed meeting.

Wishing you the best in investing,

Hi Alan

I know that your news letter services goes a long way to finding the suitable candidates for CC & CSP.

using this list as a primary CC and CSP stocks , does the bluecollar then further analys this list using high IV stocks?

Also, does the list take into consideration the IV rank ( percentile)?

Many thanks

Sean

Sean,

We provide IV stats for the eligible ETFs. For the stocks you can use the column titled “beta” to locate stocks with high betas and those are more likely to also have higher IVs. Options chains must ne checked to get precise premium returns which are based primarily on IV.

Alan

Alan,

I always try to follow your indication in the summary, where you say if you are bullish, or bearish, or cautiously bullish, and you are favoring ITM or OTM strikes.

But most of the time, when I am not frankly bullish or bearish, I find the ATM or slightly OTM strikes very atractive, and I noticed that you do not mention them in the summary. Why is that?

Roni

Roni,

I view ATM and OTM strikes as bullish approaches to covered call writing. When I write that I am favoring ITM strikes 2-to-1 that means that in my portfolio I am selling 2 ITM strikes to every 1 either ATM or OTM. Stated differently, I am assigning percentiles to strikes that have or don’t have intrinsic value.

This mix may or may not coincide with the assessment of others.

Alan

Alan,

As a build on Roni’s question do you apply your ratio within securities, between them or perhaps both?

Meaning, in the reply above if you had 300 shares of BCI would you sell 2 contracts ITM and 1 ATM/OTM? Or if you had 3 stocks would you cover 2 ITM and 1 ATM/OTM?

If the later how do you decide between them? Not that you would ever cover BCI ITM :). – Jay

Great question Jay.

It never ocurred to me.

I always took for granted that Alan meant different stocks.

From now on I will look at it in both ways.

It’s curious how each individual has a different approach to the same situation.

🙂 – Roni

Thanks Roni,

The beauty of building positions in stocks or ETF’s you like in 100 share increments is you can then write ITM, ATM. OTM or not at all on any portion of the holding depending on your market view. – Jay

Jay, Roni,

I give total percentiles in my current portfolio. Here’s how I handle these matters:

I favor OTM strikes for stocks with the strongest technicals and ITM for those with mixed technicals. These are guidelines so we shoot for approximations…same as cash allocation per position.

Here’s an example:

Stock A: Bold on our “running list”

Stocks B&C mixed technicals but eligible

We are selling 5 contracts of each

Bearish market assessment favoring ITM 2-to-1

Possible portfolio mix OTM/ITM:

Stock A: 3/2

Stock B: 1/4

Stock C: 1/4

ITM contracts: 10

OTM contracts: 5

There’s our 2-to-1 ratio…again it’s a guideline.

Alan

Understood.

Thanks – Roni

Roni and Jay,

Just to add two minor foot notes to this thread…

[1] The technique that Alan discussed is called “Laddering” and this has been used for decades in the fixed income world to maintain a flow of interest payments to the bond holders. Options traders have picked up the methodology and have added it to their trading tool kit.

[2] As Alan reminds us all, diversification is critical. By laddering strike prices in our trades, we are adding an additional element of diversification.

Best,

Barry

Barry,

It is nice to hear your voice on the blog since I suspect you are the “Man behind the Curtain” in this band :)!

Alan is the lead singer but I doubt he could do it without you!

Please continue to be a voice :). Best regards, – Jay

Jay,

You are 100% correct. Barry is an amazing talent and a vital part of the BCI team. He is responsible for producing our weekly stock reports and does so with incredible accuracy and reliability. I am blessed with a skilled and dedicated team which, along with our members, have put BCI on the financial map and yes, I could not have done this alone.

Alan

Thank you Barry,

your clarifications opened my eyes and helped me to better understand the full strategy of diversification.

Now I have an extra valuable tool in my quest for low risk management of my portfolio. 🙂

I really do need all the help and protection I can get. – Roni

Premium Members:

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 11/06/15.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Best,

Barry and the BCI Team

To the BCI community:

Several members of the BCI team and I just returned from a 3-day event in Las Vegas where I hosted a presentation for the American Association of Individual Investor’s (AAII) national conference. It was especially rewarding for us to meet so many of our members in person. I hope you enjoyed my presentation and thank you for filling every seat in the seminar room making me look good!

I will be catching up with member emails and comments by the end of the week and will be making announcements of additional seminar invitations I will be accepting for 2016.

Alan

AAII National Conference seminar photo:

Click on image to enlarge & use the back arrow to return to the blog.

Alan

I would be interested to view the recording of your LV presentation, if one was made.

Sean

Sean,

The good news is that the presentation was recorded. The maybe-not-such-good-news is that as an invited speaker I have no control as to when the seminar will be made available and what the cost will be to view. When it does become available it will be on the AAII site (www.aaii.com). I will publish information about the recording to our members when I get updates from the organization.

This was a new seminar I wrote specifically for the event so I’m discussing with my team the possibility of hosting a webinar for our members and sharing this new presentation with the BCI community.

All the information is found either on our site or in my books/DVDs but packaged as “5 actionable ways to generate income or buy a stock at a discount using 2 conservative option-selling strategies”

Alan

I’ve asked my team to ‘tone down” this pop-up screen on the blog. We’re having a great response to our contest but don’t want you to navigate through so many pop-ups reading a blog article or commentary…Alan

Premium members:

This week’s 8-page report of top-performing ETFs and analysis of ALL Select Sector Components has been uploaded to your premium site. The report also lists Top-performing ETFs with Weekly options.

Note how all the high implied volatility (IV) securities from last week’s list were “bumped” this week confirming that high IV means higher option premiums but also greater risk. All ETFs on this week’s report have IVs under 24.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team