Covered call writing is a low-risk cash-generating strategy. It is not a no-risk strategy. As we become educated and master the 3-required skills (stock selection, option selection and position management), it is understandable why BCI members try to figure out strategies that can convert low-risk to no-risk. Here is a common inquiry I receive from some participants of our sophisticated BCI community:

Can we create a no-risk strategy by selling an in-the-money strike that generates a time value return that meets our goal, say 2%, with substantial downside protection, say 4%. Then, if stock price drops by 4%, we close our position and keep the 2% profit without losing any money?

Real-life example using PayPal Holdings, Inc. (NASDAQ: PYPL)

On April 1, 2019, here is the option chain for 1-month expirations for PYPL with the stock trading at $103.84:

PYPL Option Chain 4-1-2019

The $100.00 in-the-money strike shows a bid price of $5.95. Let’s feed this information into the multiple tab of the Ellman Calculator:

The Ellman Calculator: PYPL Calculations

Note the following:

- Yellow field: Initial time value return is 2.1%

- Brown field: Downside protection of the initial time value profit (not breakeven) is 3.7%

- We are guaranteed a 2.1%, 1-month return as long as share value does not decline by more than 3.7% by expiration

Summarizing the “no-risk” hypothesis

The proposed strategy suggests that once the stock value declines by 3.7%, we immediately close our position for a (near) 2.1% profit.

Fallacies in the strategy…there is no free lunch

First, there is a rare, but possible chance of a price gap-down of more than 3.7%. I say rare because, if adhering to the BCI methodology, we are avoiding earnings reports, the most common reason for a gap-down. But unexpected bad news can rear its ugly head and result in such a drastic price decline.

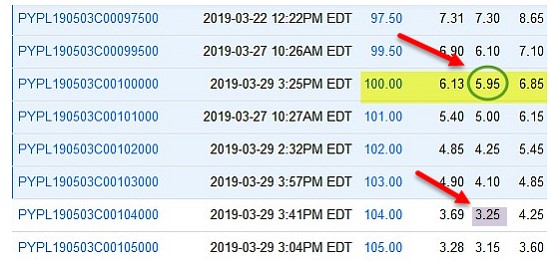

The main fact that is neglected in this theory is that we will incur a time value cost-to-close. When the trade was entered, the $100.00 strike was in-the-money compared to the $103.84 cost-basis. As share price declines, that $100.00 strike will move towards at-the-money (near-the-money). By definition, at-the-money strikes have a higher time value component than in-the-money strikes…just check any option chain on any stock. Let’s review the option chain for PYPL once again, this time comparing the time value component of the $100.00 in-the-money strike and the $104.00 near-the-money strike:

PYPL ITM and OTM strikes

Note the following:

- Yellow field: Shows a bid price of $5.95 for the in-the-money strike. After deducting the intrinsic value component ($3.84), we calculate the time value component to be $2.11 ($5.95 – $3.84)

- Brown field: The time value for the near-the-money $104.00 strike is $3.25, 54% higher than the in-the-money strike

Theta factor

The above strike comparison occurs at one point of time but the comparison would more accurately be evaluated at two points in time, trade initiation and when trade closure is being considered. This is because the time value will be eroded to some extent by Theta. However, Theta will not detract from the fact that we are incurring a time value cost-to-close and the trade will therefore not be no-risk. The actual risk can be quantified as follows:

Risk = [(Breakeven – lesser stock price) + time value cost-to-close)]

Let’s say share price drops to $96.89, a dollar below the breakeven ($103.84 – $5.95) and the cost-to-close is $1.50. Our loss would then be $1.00 + $1.50 = $2.50 per share + trading commissions. If share price drops to precisely breakeven, our loss would be the time value cost-to-close $1.50 in this hypothetical + small trading commissions.

Discussion

There is no such thing as a legal risk-free investment when our goal is to achieve higher than a risk-free return (Treasuries, for example). The reason we are receiving these higher returns is because we are willing to incur some degree of risk. By mastering the 3-required skills, we will become elite covered call writers and should beat the overall market on a consistent basis. In the above example, we will use our exit strategy to mitigate losses and, in many cases, turn losses into gains.

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to share some of these testimonials in our blog articles. We will never use a last name unless given permission:

Hi Alan,

I have spent the last few days going through your great video series on covered call writing, risks & opportunities.

Thanks for providing some great inspiration and content.

Kind regards,

Gitte

Upcoming events

September 14, 2019: Charlotte Chapter of The American Association for Individual Investors

“Converting Non-Dividend Stocks to Dividend-Like Securities”

Live webinar

Saturday from 10 AM – 12:PM ET

September 26 – 27, 2019: Philadelphia Money Show

September 26th: All Stars of Options

September 27th at 1:30 PM: “How to Select the Best Options in Bull and Bear Markets”

***********************************************************************************************************************

Market tone data is now located on page 1 of our premium member stock reports.

***********************************************************************************************************************

Alan,

In this article (thanks for doing these) the option chain shows bid/ask spreads of 5.95-6.85 and 3.25-4.25. Wouldn’t you say that we could have much better than the bid prices you used in the article by using the show or fill rule?

Thanks again,

Susan

Susan,

Most likely, yes we could have dome better than the published bid. I used worst case scenario.

In practical application when selling options, I would have set limit orders at $6.35 and $3.70, leveraging the “Show or Fill Rule” respectively.

The key point here is that at-the-money strikes have greater time-value components than in-the-money strikes.

Good observation.

Alan

In addition if PayPal suddenly drops from 103.84 to 96.89 ( 6.7% drop) most likely the option prices will increase due to the increase in volatility. Thus increasing the loss if one tried to close the covered call when the stocked dropped in price.

Hi Pete,

normally, when a stock drops, the options also drop.

Less than the stock, but they drop.

How much? Depends on the the time left until expiry.

That is the reason why we can buy back the option in the first half of the cycle (considering monthlies) at 20% of the original value, and at 10% in the beginnig of the second half, and wait a little for a rebound, to hit a double.

If there is no rebound, we have a paper loss, and must decide our next step: Sell a lower srike to mitigate the loss? Unwind and place the remaining cash on a new, more promising trade? and so on….

Roni

Hey Pete and Roni,

Pete, in your sell off scenario for PYPL the value of the put premiums will definitely increase. If you are still bullish PYPLand have a little available cash you can go further underneath it and sell a couple CSP’s for a nice premium and a chance to add to your position lower. I do that frequently on the down days when my orientation is still bullish on things I like.

If you own a stock and have a cc sold against it and the stock “out runs” it’s coverage going down, well, that will always be a paper loss until you either wait it out or do something with it. It’s a constant part of the game. But cc writers will always be ahead of those who just hold when times get tough.

Roni has this stuff nailed and uses the BCI methods masterfully! – Jay

Jay,

Thanks for your valuable insight. If we are still bullish on PYPL would it be better to buy more shares at the lower price and sell otm calls to get both premium + share appreciation up to the strike? With puts we just get premium. Or is it better to sell a put as a defensive move even though we are still bullish on the stock that has gone down in price. Interested in your take.

Thanks,

Marsha

Hey Marsha,

I always enjoy your contributions here. Thanks for your generous over rating of my comments as “insight” :)!

I have some skin in this game since I own 200 shares of PYPL. They were put to me after a CSP way back when it was about $60 a share.

To your question: first and foremost are you bullish the broader market and the tech sector from now to Oct expiry? If so do you still like PYPL? I am yes and yes on that since there is a Fed meeting on the 18th and Trump has trade talks set out there in October. I don’t see a lot of sell catalysts between those events other than the normal ebb and flow.

On PYPL you could sell the October 102 CSP for 1% plus cash return and about a 3% discount on today’s price if you want more shares lower. If it takes off you will wish you had added on this dip but that is all a part of the game :)! I am not overwriting my shares for October since I still like the stock and it’s bounce chance.

If you pick up more shares this week I can’t imagine you will regret it? If you buy please grab them on down days like today and if you decide to cover them wait for a bounce day when call prices are higher and even then give them OTM room.

That is my take and thank you for asking :)! – Jay

Hi Jay and Marsha,

we are all in the PYPL club, and I bought back my 3 PYPL 09/20/2019 110.00 calls last week for 17% of original premium.

Waiting for rebound, I broke my 2% limit loss rule yesterday, and am now losing $1282.00 (4%).

It’s not a big deal, but tomorrow we must decide the exit strategy: Either roll down to mitigate, or unwind, or whatever….

Maybe we get lucky, and it comes back, but it can also get worse. Who knows?

Roni

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 09/06/19.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Best,

Barry and The Blue Collar Investor Team

barry@thebluecollarinvestor.com

Hi all

Am I the only one thinking today’s price action is kinda weird?

Quality names as well as some low-volatility stocks sold off recently whilst we see a crap rally in cyclicals.

Strange market environment especially since markets have gone nowhere over the past year.

What are you guys doing when there’s a flight to volatile and risky assets?

Best

Hamish

I currently have no opinion on the market and that’s why I sold wide strangles on stocks that don’t see their volatility suddenly spike…

Hamish,

6 out of my 8 positions are in the red.

Only ULTA and QCOM are saving the day.

Roni

To all members; Stock migration:

We have noticed in the past few days, There appears to be a migration out of growth stocks into “value” stocks… lower beta, lower P.E, lower volatility. This has impacted many of our positions including mine. We have seen this in the past and is no reason for concern. It is important to remain non-emotional and manage our positions whenever exit strategy opportunities present themselves. Quality stocks will recover. I expect that these changes will be reflected in the next stock report if these securities don’t recover over the next few days.

Alan

Thanks Alan,

Great and instructive note as always! Like yourself and other friends here I have seen sector rotation play out many times over the years. Sometimes the money “leaves the house” entirely and goes to gold, treasuries or cash. But most of the time it just leaves one room and goes to another. Like from tech to utilities or staples and then back again.

That is why I keep at least half of my equity exposure in SPY. Unequaled liquidity, easily optionable and all the sectors are in there. I have lost count of how many times I have heard most mutual funds and money managers do not beat SPY. I know you do it every year! But if one starts with SPY and uses option selling to increase it’s yield it’s pretty hard to go wrong unless the world turns upside down and then everyone is screwed :)!

Higher up on my investing pyramid I have room for the sexier stocks out there. Anyway, for what it is worth… – Jay

Wendy”s (NASDAQ: WEN):

Several of our members wrote to me asking why the price decline for this stock. I found this article:

https://www.investors.com/news/wendys-stock-falls-amid-breakfast-investment/?src=A00220&yptr=yahoo

Alan