Put–call parity is a principle that defines the relationship between the price of European put options and European call options of the same stock, strike price, and expiration date. The formula can identify arbitrage opportunities where the simultaneous buying and selling of securities and options result in no-risk profit. I am writing this article in response to a number on inquiries why I have rarely addressed this topic in the past. The subject is a bit complicated and doesn’t directly impact our option-selling trades but, on the other hand, we can never receive too much education so here we go.

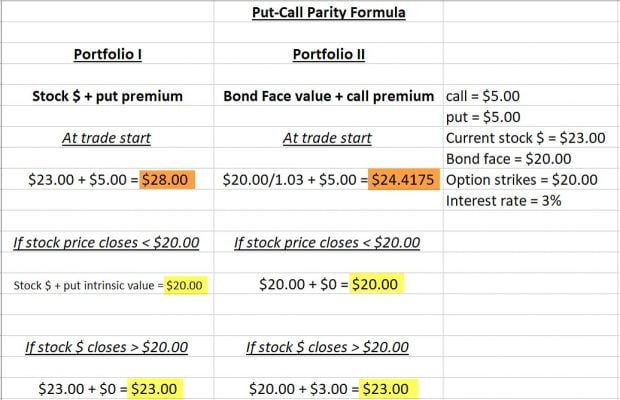

Put-Call Parity formula

Stock $ at expiration + put value at expiration = call value at expiration + face value of a bond that will pay for exercise of the call option at expiration

Think of each side of the equation as an individual portfolio and, if put-call parity is respected, both portfolios will be of equal value at contract expiration. If not, an arbitrage opportunity will exist.

Assumptions in this formula

Apply only to European style options that can be exercised only at contract expiration

- Transaction costs not included

- Dividends not included

- Adequate liquidity available

- Same stock

- Same expiration

Put-Call parity with no arbitrage opportunity (data for calculations in far right column)

Each side of the equation or portfolio expires with equal value

Put-Call parity with arbitrage opportunity

We used an interest rate of 3% just to complete the formula. The reason we use $20.00/1.03 for the bond value at the start of the trade is because the face value of $20.00 is not realized until contract expiration so the 3% interest rate must be accounted for. Note that in the brown cells the arbitrage opportunity was identified but in the yellow cells the inflows in both portfolios was the same whether share price moved up or down. The market immediately eliminates these arbitrage opportunities which apply only to institutional investors.

How do institutional traders make money when arbitrage opportunities are identified?

The more expensive portfolio is sold and the cheaper portfolio is purchased. In this scenario, a profit of $3.5825 per share will be a risk-free return. They manage their trades via shorting stocks and writing puts but this is not relevant to retail investors and is beyond the scope of this article.

Discussion

Arbitrage opportunities are not applicable to retail investors because we don’t have the tools to identify them fast enough when they occur. Since this was a topic of interest to many in our BCI community, I decided to publish this as one of the 52 articles I will author this year.

#1 Best-Selling Books

New webinar

PREMIUM MEMBERS: New Blue Hour Webinar

VIX Covered Call Writing

Now available on your member site. Scroll down on the left side.

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to share some of these testimonials in our blog articles. We will never use a last name unless given permission:

Dr. Ellman,

I bought Complete Encyclopedia for Covered Call Writing and Selling Cash-Secured Puts and think they are the best written and most useful books I have read on option trading.

Best regards,

Dan F.

Upcoming events

1. East Michigan AAII Chapter: Live Webinar

April 23 @ 7:00 pm – 9:00 pm

Covered Call Writing to Generate Monthly Cash-Flow

Option Basics and Practical Application

Thursday April 23rd

7 PM – 9 PM

Login information to be sent to premium members.

2. Money Show Vegas Online Virtual Webinar

Tuesday May 12th

3:20 PM – 3:50 PM

Details to follow.

***********************************************************************************************************************

Market tone data is now located on page 1 of our premium member stock reports and page 8 of our mid-week ETF reports.

*********************************************************************************************************************

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 04/17/20.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Since we are in Earnings Season, be sure to read Alan’s article, “Constructing Your Covered Call Portfolio During Earnings Season”. You can access it at:

https://www.thebluecollarinvestor.com/constructing-your-covered-call-portfolio-during-earnings-season/

Best,

Barry and The Blue Collar Investor Team

barry@thebluecollarinvestor.com

Premium Members,

There is a new Blue Hour Webinar available…“VIX Covered Call Writing”. You can view it by scrolling down on the left side of the Premium Member website.

Best,

Barry

Hi Alan,

I have the following questions.

1. The month of May, 2020 is a month with 5 Fridays.

According to BCI methodology, the 4 th Friday of the month , May 22nd , should be the expiration day.

However, when I checked today the Fidelity brokerage account , the expiration day for selling calls is May 15, then June 19 etc.

So, is it something I’m missing?

2. Regarding the Earnings report date:

-For JD stock , BCI report states ER date 6/1/2020. But when I tried to Google it , Tipranks.com states that it might be May 8th, which would be during the contract.

-For ZTO stock , BCI report states that ER day is 6/15 but Tipranks and Fidelity states is 5/20 . This would be good if the expiration is on 5/15.

My question regarding the earnings report date is: which is the most accurate source we can find this date? How long in advance the company set up this date?

Thanks much.

Mihaela

Hi Mihaela,

I found on http://www.earningswhispers.com 6/1/20 for JD and 6/15 for ZTO. I think these guys are recommended by BCI for ER information.

Best,

Hi Mihaela,

There are four times in the year that there are five-week options months…this month happens to be one of them. The remaining eight options months are four weeks in length.

As for your question about the Earnings Reporting dates…

This is an issue for us (and all other services)…there is no consistency in ER date data prior to a company announcing their upcoming ER date on their website. The dates in the report come from EarningsWhispers.com (EW). EW has been our most reliable source since it in one of the few ER Date services that can confirm the date of the ER announcements, providing well above 90% accuracy. Any other non-confirmed date is just an estimate. As a matter of fact, most financial websites provide a disclaimer when reporting ER dates. For example:

– Schwab: “…The data is gathered by Wall Street Horizon, but still considered tentative…”

– NASDAQ: “…The upcoming earnings date is derived from an algorithm based on a company’s historical reporting dates. Our vendor, Zacks Investment Research, might revise this date in the future, once the company announces the actual earnings date…”

In the case of the stocks you mention:

– JD:

– Earnings Whispers — 6/1

– Schwab — 5/8

– Yahoo — 5/8–>5/12

– CBOE: No information

– Company Website: No announced date as of 04/19/20 at

3:00 PM EDT

– Last ER Date: 03/02/20

– ZTO:

– Earnings Whispers — 6/15

– Schwab — 5/13

– Yahoo — 5/3–>5/18

– CBOE: No information

– Company Website: No announced date as of 04/19/20 at 3:00 PM EDT

– Last ER Date: 03/16/20

Since companies report approximately every 90 days, the Earnings Whispers appear to be the most reasonable.

I hope that this gives you a better picture of the issues surrounding ER dates. We make EVERY attempt to get our subscribers the most accurate data available at the time our reports are published.

Best,

Barry

Hi Alan,

I am new to selling Cash Secured Puts but am following you book’s guidelines on the at subject.

The one question I’m still unsure about is the scenarios where the Underlying Security Price Drops Dramatically.

The guidelines say one option is to accept assignment and then sell covered calls against the stock or ETF, at strikes above the current price, even if those strikes are lower than the original purchase price of the underlying.

What I’m unclear about is if the price rises to or beyond the strike of the short call, and it’s called away, won’t I lock in a loss between the original purchase price and the strike of the short call?

Any feedback you can provide will be appreciated.

Thanks!

Dave

Dave,

If our covered call trade is in-the-money as expiration approaches, we must decide if the underlying security is one we want to retain in our portfolio. We also must check to make sure there is no upcoming earnings report in the next contract cycle.

Based on these guidelines, if we decide retain the stock, we must check the “What Now” tab of the Ellman Calculator to make sure that rolling-out or rolling-out-and-up meets our initial time-value return goal range.

If it turns out that retaining the stock or rolling the option does not align with system guidelines and rules, we allow assignment and take the loss. Not every trade will be a winning trade. We don’t want to take a losing trade and make it worse.

It’s important to remember that it is the cash we invested in the stock, not the stock itself, that is what is important to us. We ask ourselves, as expiration approaches, where is that cash best placed… in the current stock or another?

Taking a non-emotional approach to investing based on sound fundamental, technical and common-sense principles will guide us to the highest returns in the long run.

Alan

Hi Alan

I hope you have a good weekend. I can’t help thinking about my option positions over the weekend. I probably moved too fast on option selling before mastering the strategies.

I have JNJ in my portfolio for a while and add more around at $110-138 recently. On 4/8/2020 I sold 6 JNJ 4/24/2020 $140 calls for 4.95 to generate some income. I made mistake on selling calls with the upcoming ER (4/14/2020) but did not know better back then before I read your books. JNJ recently has been up, especially after the positive earning/revenue beats. I have to decide among the 3 choices – taking no action, rolling out or rolling out and up. What you would do if you are in my shoes? I have read several of your books and just started to learn more as the premium member and practiced on your calculator “WhatNOW”.

My second question is whether we should write options in the current volatile market condition. We would miss out the upside appreciation in writing calls during the recent strong rally, while selling puts also carry risk if the market re-test March 23rd low. You mentioned about your 2008 experience in one of your videos. Your input would be greatly appreciated!

I have earned great returns from real estate investment in the past 16 years but am an option newbie who is eager to learn but desperately need some guidance!

Thanks

Lisa

Lisa,

Let’s start with this… you made a huge profit on those 6 contracts… reason to celebrate.

Now, as expiration is approaching, we must decide among the 3 choices you mentioned. The “What Now” tab of the Ellman Calculator (as of tonight) will probably show that rolling-out does not pay. Rolling out-and-up may make sense if our bullish assumption is still in place. These decisions can be made on Friday. Whatever you decide, remember you have a very nice result on the initial positions.

I believe that the current market environment is challenging for most retail investors, even for the pros. I am currently in 50% cash and taking unprecedented defensive positions in my portfolios.. Each of us must determine our comfort level based on our personal risk-tolerance.

If you decide to cut back on the capital in your stock portfolio, paper-trading is a useful replacement. If we can learn to trade in challenging market conditions imagine the possibilities in normal market scenarios.

Keep up the good work.

Alan

Good morning Alan

Thanks for your encouragement!

Somehow I felt horrible and regret about selling the calls because the appreciation miss out, when JNJ stock keeps going up. The higher it goes up, the worse I feel. Without the call writing, I would have been happy for the situation. Is this normal?

Today JNJ finally dropped, should I roll out and up when the price is lower today or wait till the expiration date 4/24 to do the roll out & up? My concern is the comparative return will be lower what if JNJ is up on 4/24. I guess it does not matter- as the premiums for buy to close and sell to open will go up or down as the underlying stocks – thus cancel out the effect by the stock price change? You mentioned to do roll on 4/24, because the time value for 4/24 call is the lowest? When is the best time to roll?

Thanks so much!

Hey Lisa,

Alan will give you a great answer to your questions as he always does.

But you raise a good point I would like to toss my two cents into the pond on: the frustration of selling covered calls on stocks that rise and the feeling of missed opportunity because you have them covered.

In better times I felt that way frequently. Yet I am the world’s third biggest proponent of selling options behind Alan and Barry :)!

But is a tool, not a way of life. The separate peace I made with it is over write half of each position and let the other half run. That requires you buy 200 shares of anything you like so you can sell one contract and leave the other shares untethered.

See how each half does for a while and the path will open about what works best for you. In sideways to bad times you will be glad you sold the calls. In good times you will be glad you didn’t. – Jay

Lisa,

I will typically start rolling options between 1 PM and 2 PM ET on expiration Friday. If I am traveling (not lately) on Friday, I roll options on Thursday, the day prior to expiration Friday.

Now, a philosophical look at covered call writing, adding to Jay’s meaningful thoughts:

When a strike moves deep in-the-money, we have maximized our trade results based on the initial structuring of the trade. If we sold an OTM strike and generated 2% on the option premium and another 3% on share appreciation from initial market value to the OTM strike, we have a 5% 1-month return. Now, if the trade would have made more than a 5% 1-month return had the call not been written, is that a reason to agonize? In my humble opinion…no.

Once we have made a decision on a strategy appropriate for our portfolio and achieved a successful trade based on that strategy, it is reason to celebrate.

Now, some, like Jay, may elect to use more than 1 strategy. Nothing wrong with that. I do too. As my portfolio wealth flourished over the years, I have several portfolios mainly dedicated to option-selling but a smaller one dedicated only to long stock positions. About 90% of the stock portion of my portfolio (includes real estate, bonds and cash-equivalents) is devoted to option-selling because that is where I’ve realized the greatest success…by far.

Alan

Hi Alan,

In our last blogs you were kind enough to share/explain your delta-neutral strategy using SH (the inverse of SPY) along with a paired amount of stocks and writing ITM on both sides due to the unknowns of the virus situation and the high volatility environment.

Are you doing that again for May expiry?

I have been using any weakness in SPY to unwind my SH position. I noted this weekend the Q’s are actually up YTD and are up again today! I suspect Amazon has helped there and why XLK is not keeping up with QQQ since the SPDR’s have AMZN over in the XLY.

Anyway, thanks for the insights as always and a great new May expiry to all. – Jay.

Jay,

Yes, I am staying in this highly defensive position with half better-performing stocks/ETFs and half inverse ETFs (SH). I entered all my positions yesterday along with my 20% BTC limit orders.

Alan

Thank you Alan, very helpful insight as always!

If you will pardon a lousy insurance analogy I bought my SH shares as portfolio insurance against further weakness. They are helping this week. I will not overwrite them since that seems like lessening my coverage :)!?

I will portfolio overwrite some longer term bullish holdings as extra precaution. Thanks again, – Jay

Premium members:

This week’s 8-page report of top-performing ETFs and analysis of ALL Select Sector Components has been uploaded to your premium site. The report also lists Top-performing ETFs with Weekly options as well as the implied volatility of all eligible candidates.

Also included is the mid-week market tone at the end of the report.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

Hi Alan

I have $9500 in my account. Is it enough Money to buy 200 shares of stock $30-$35 and sell 2 calls that cost $1?

Or buy 300 shares $22-$25 and sell 3 call that cost $0.65-0.8?

Thank you,

Gena

Gena,

For purposes of proper diversification along with a cash reserve for exit strategy trade executions, building up portfolio wealth should be considered. This is the exact approach I took before I started selling options. I address how to accomplish this in an automated way in one of my books:

https://www.thebluecollarinvestor.com/stock-investing-for-students/

In the interim, the education process along with paper-trading can continue.

The time and effort will pay off for years and decades/

Alan

Hi Alan !

Please can you provide me with the link about Etfs covered call when there is a split . ( I cannot find the dialogue where you gave me the link two weeks ago )

Thank you so much

Charles,

Here is a link to an article I published on stock (ETF) splits:

https://www.thebluecollarinvestor.com/covered-call-writing-and-contract-adjustments-our-premium-report-is-getting-even-better/

Alan

Thanks again Alan !

I will watch todays webinar at 7 Pm .

All the Best !

Is there a URL to today’s webinar? Or is it a premium members only event?

Pavel,

Yes, this was a premium member event.

Alan