Option calculations help guide us to an accurate assessment of our covered call writing profits. It’s more meaningful to use percentages rather than dollar amounts when executing these calculations. For example, a $1000.00 profit on a $10,000.00 investment (10%) is much more significant than a $1000.00 return on a $100,000.00 investment (1%). That’s why percentages form the foundation for both versions of the Ellman Calculator (Basic and Elite). Our most recent spreadsheet, the Elite-Plus Calculator offers both dollar and percentile returns for each position as well as the entire portfolio.

Last year, one of our members shared me with one of his successful covered call writing trades and inquired about percentage returns month-to-month. In this article, I will breakdown that trade and use the Ellman Calculator to demonstrate the second leg of the trade which included rolling out-and-up.

The trade with Allergan (NYSE: AGN)

- 5/28/2019: Buy 100 x AGN @ $121.19

- 5/28/2019: Sell 1 x May 31 Weekly $120.00 call at $3.52

- 5/31/2019: Share value: $125.59

- 5/31/2019: Buy back May 31 $120.00 call at $6.20

- 5/31/2019: Roll out-and-up to the June 21 $125.00 call at $4.10

- 6/21/2019: Option expires in-the-money and shares are sold for $125.00

Initial calculations with the Ellman Calculator

You will note that the trade was established at the end of May with a Weekly contract. Here are the final returns from the first 4 days of the trade as shown in the multiple tab of the Ellman Calculator:

AGN: Weekly Contract Returns with the Ellman Calculator

A very significant short-term return (1.3% in 4 days). Note that the intrinsic-value component of the premium ($1.91) is not used as part of our initial time-value profit but rather to “buy-down our cost-basis to $120.00. This computation allows us to make the best trading decision at that point in time. Next, a decision was made to roll-out (next month) and up (higher strike price). For this computation we use the “what now tab” of the Ellman Calculator and first fill in the blue cells on the left side of the spreadsheet:

AGN: Roll Option Entry Information

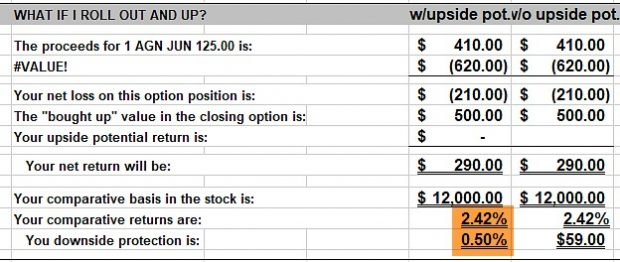

Calculating rolling out and up returns

The option was bought back at $6.20 and the next month’s higher strike was sold for $4.10. The key point here is that our cost basis is now $120.00, not $120.36 or $125.59. The reason is that we are deciding whether to roll the option or allow assignment. We must compare “apples-to-apples” If we permit assignment, we will receive $120.00/share as per our initial option obligation. If we roll the option, our cost basis must be the same so we can decide which approach is in our best interest. Once the blue cells on the left side of this tab our filled in as shown above, the white cells on the right side become populated with results: Once the shares were sold as a result of option exercise on 3/21/14, a 2.42%, 1-month return was realized and Jon had $12,500/contract in cash to use the following week for the April contracts.

Rolling Out-And-Up with AGN

This second set of calculations also represents a way of making the best trading decision at that point in time.

Final returns

In reality this is a 6-week return because the trade was initiated mid-contract in February:

We will now view this series of trades in totality:

- Stock side: ($125.00 – $121.19) = + $3.81

- Option side: (+$3.52 – $6.20 + $4.10) + $1.42

- Net gain = $3.81 + $1.42 = +$5.23

- 6-week % return = $5.23/$121.19 = 4.3%

Summary

Although calculations can be challenging for many of us, using percentages and the Ellman Calculator will make our covered call writing decisions more meaningful and help elevate our returns to the highest possible levels. Calculations can focus in on specific trades at any given point in time or on total returns for a series of trades. For a detailed discussion of covered call writing calculations see pages 99 – 152 in the classic edition of the Complete Encyclopedia for Covered Call Writing. Also, for a free version of the Basic Ellman Calculator see the “free resources” link on the black bar at the top of this page…just enter your email address and download this tool to your computer.

Investment club program board members

If you would like to schedule a private webinar with Alan and Barry, send an email to:

info@thebluecollarinvestor.com

Include:

- Contact email

- Contact phone #

- Club website URL

- Put “private webinar” in the header

Your generous testimonials

Over the years, the BCI community has been incredibly gracious by sending our BCI team email testimonials sharing stories as to what our educational content has meant to their families. Moving forward, we have decided to share some of these testimonials in our blog articles. We will never use a last name unless given permission:

Hi Alan,

I went through beginner’s lesson #2 today I’m happy to say and will be done with lesson 3 by the end of the day tomorrow. This is really good material, Alan. I never heard it explained so well before. Wish I would have known about you years ago. I’m on the right path now.

Thank you.

Denise.

Upcoming events

1. How to Set Up a Covered Call Writing Portfolio Using Stock Selection, Option Selection and Position Management

Step-by-step analysis using the Elite-Plus Calculator

Hosted by:

Dr. Alan Ellman, President of The Blue Collar Investor Corp.

Barry Bergman, BCI managing Director

The initial structuring of our covered call writing portfolios is critical to achieving the highest returns. Once established, we move to position management mode.

This class will start with option basics, define covered call writing and detail the 3-required skills that will allow us to become elite covered call writers… stock selection, option selection and position management.

Real-life examples will be analyzed describing how the stocks and options are selected as well as how to set up the overall portfolio based on cash available, strategy goals and personal risk-tolerance. Various spreadsheets will be used to simplify the process.

An introduction to the initial step in position management will also be addressed. This class is for beginners to sophisticated option traders. There will be something for everyone.

Time: Oct 15, 2020 08:00 PM Eastern Time (US and Canada)

Join Zoom Meeting

Meeting ID: 940 8782 0438

2. Wealth 365 Summit (free)

I was invited do host a 1-hour webinar on

Monday October 12th at 7 PM ET

***********************************************************************************************************************

Market tone data is now located on page 1 of our premium member stock reports and page 1 of our mid-week ETF reports.

****************************************************************************************************************

Alan,

Thanks for this article. With AGN moving up in price and such great returns, are there any reasons we would not consider rolling this option?

Thanks again,

Glenn

Glenn,

Since share price was rising and we avoided earnings reports, we can assume the technical chart and fundamentals remain bullish. There are 2 reasons we may decide not to roll:

1. The calculations do not meet our initial time-value return goal range.

2. There is an upcoming earnings report in the next contract month.

Alan

Alan;

A question for you about PMCC regarding the short call as you approach expiration. Would you incur risk by allowing the short call to expire worthless? The risk being that the underlying would spike in price in the afterhours trading causing assignment. If this were to happen, the long LEAP provides “protection” but not “coverage”. By that I mean that the LEAP would not be executed automatically. Your account would be debited the cost of 100 shares while still holding the long LEAP. You would be left to unwind/deal with this at the Monday opening.

To avoid the risk, either buy back the short call or roll the call.

Am I looking at this correctly?

Best regards;

Terry

Terry,

Yes you are.

We have 2 points of concern here. First, if the option short call strike is only slightly out-of-the-money as 4 PM RET approaches, there is a chance that it may end up exercised as a result of “pinning the strike” or after-hour news. Market-makers have until 5:30 PM ET to decide on exercise. Here is a link to an article I published several years ago on “pinning”:

https://www.thebluecollarinvestor.com/pinning-the-strike-a-covered-call-writing-consideration/

Here is a link to an article I published on after-hour exercise:

https://www.thebluecollarinvestor.com/expiration-dates-versus-expiration-times-important-clarifications/

2. Many brokers will automatically exercise the LEAPS to provide the shares for the short call obligations. Check with your broker prior to entering any PMCC trades regarding how they manage these scenarios.

Alan

Alan and Terry,

This is a very interesting topic. I trade with E*Trade, now a part of Morgan Stanley. I don’t know what changes are coming down the pike in this acquisition. Since they have been in two different segments of the financial world there probably will be less turnover than at TD Ameritrade and Schwab.

Anyway, E*Trade tells me that they do not actually do the settling of options themselves. They say OCC (Options Clearing Corporation) does it. They offered very little info without me pressing them. What I did manage to get from them was:

(1) PMCC being a diagonal spread nothing would happen on your LEAPS. You, the investor at E*Trade, would be responsible for providing the stock that had been assigned. Your account, on Monday, would show a minus position of those shares called. You would have to purchase them at market price if you had not instructed them to exercise your LEAPS on the Friday of your sold call(s) expiration. Obviously, having let you enter this trade they will work with you to get it settled. So, don’t panic. That means you could exercise your LEAPS and they would have to cover you for one day. They probably wouldn’t like it and might give you a hard time, depending on your account balance and trading activity. 😊

(2) The same issue exists for credit vertical spreads. If you hold to expiration and your short is ITM but your long is OTM and you are not closing out the position, you must call them if you wish to use your long to acquire or put the stock and have the settling transaction done simultaneously thus only realizing the max loss you were facing when you entered the trade. (I.e., the difference between the strikes minus credit received.) If you don’t call the broker your long will expire worthless and you will either have to acquire the stock for assignment or buy it when it is put to you. If you don’t call your broker you can potentially lose more than your max loss at position entry. Obviously, having let you enter this trade they will work with you to get it settled. So, don’t panic.

(3) Always remember if you short an option, it can be assigned against you at any time. This is usually not a problem as your cash is reserved to cover a CSP or you have a long position if you have done a vertical or diagonal spread.

(4) To be clear, when you call E*Trade with instructions about exercising of your long positions all they do is notify OCC.

I have had assignments in all of these scenarios. It’s not fun and has been stressful a few times with high priced equities. What it has taught me is to close or roll before expiration if it is close to ITM.

Alan, your suggestion to contact your broker on how they handle PMCC trades is excellent. Wouldn’t be a bad idea to discuss other strategies too.

Hoyt T

Hoyt;

Thanks for the response.

You raise an interesting point about vertical credit spreads. If you are assigned on your short and your long expires worthless, you are no longer in a “defined risk” trade.

Consequences:

1) You may not even know that you are assigned until the next day

2) If stock price spikes against you in after hours trading, losses are unlimited

3) You are left to deal with the fall out when the market reopens

I saw that this happened recently to a trader in TSLA and the losses blew up his account.

Best regards;

Terry

Terry,

Thanks for your reply.

Your “consequences” list is dead on.

I had two very significant experiences with exactly the scenario you described.

One, 400 shares of SHOP (part of a credit put spread) was put to me because the option went in ITM at 3:30 PM and back OTM by a few cents before the close but an investor had called and exercised the put. SHOP went up first thing Monday morning and I sold a one week OTM CC. The following Monday, after the CC had expired I sold SHOP. One of the biggest mistakes I have made. SHOP was trading around $500 then. That was in February of this year.

Two, 600 shares of ADBE (a part of a credit put spread) was put to me in a similar situation but with very different results. In that account I didn’t have enough cash to cover the cost. (I had several verticals expiring that day in two different accounts and totally missed closing the ADBE vertical.) I realized what had happened at 4:05 PM. I called my broker (E*Trade) and explained what had happened. We made some after-close trades to get me the cash for Saturday’s settlement. ABDE opened much lower on Monday so calls were too cheap. So I sold ADBE at a loss. Also in February of this year.

I would like to say that these two examples were lessons learned, but only time will time.

Most of my learning has come from personal experiences, that kind, at least, seems to stick. 🙂 But we don’t need to learn only from our experiences. We can learn from the experiences of others. That is one of the beauties of this blog that Alan so generously provides. I have learned so much from Alan, Barry, and others like you, Jay, Roni, and many more.

Good luck,

Hoyt

Hoyt,

Thank you for mentioning me among members from which you learned, but I believe it is actually the opposite. It is me learning from your experience.

Further, I was just now looking at a “repair” trade (not a LEAP) on my 10/16/20 MSFT trade, where I have that exact situation.

I mean one debit call spread 215.00 short/205.00 long, and I came to the same conclusion: The best action is closing out the position next Friday before it expires.

Your explanation helped me to gain confidence that my reasoning was correct.

I am not sure what Schwab would do in this situation, but better safe than sorry. Calling them is stressful.

Thanks – Roni

Premium Members,

This week’s Weekly Stock Screen And Watch List has been uploaded to The Blue Collar Investor premium member site and is available for download in the “Reports” section. Look for the report dated 10/02/20.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

On the front page of the Weekly Stock Report, we now display the Top 10 ETFs, the Top Performing SPDR Sector Funds, and the 4 single Inverse Index Funds. They are sorted using the 1-month performances from the Wednesday night ETF report and the prices from the weekend close.

Best,

Barry and The Blue Collar Investor Team

barry@thebluecollarinvestor.com

Hello Alan,

How is everything with you? Hope you and yours are all well, safe and sound. May I ask a few quick questions from the weekly stock screen and watch list?

The “@” symbol indicates the bar is on the 20 day EMA and OK for Watch List. Are we simply highlighting that the stock is finding support at the EMA and that the stock is still fine for writing covered calls on? I’m guessing yes because it says OK for Watch List which is the list itself from the report.

Next question is regarding slow stochastics. In general, if a stock is “over bought” that simply means too many traders have bought the stock? Referencing your book and looking at the illustrations I think I should just know that stocks above 80 on the stochastic could be a sell signal.

Do you personally avoid stocks with mixed technical data? When you review your own stock screen report is there any particular criteria that each stock must meet for you to select the stock for call writing? Such as no mixed indicators, MAR above a certain value etc? If that’s not a fair question no worries, I was just curious.

Lately I have been selling shorter term puts on JD. I like that stock and it’s holding up better than others lately. Anyway, it’s time to re-read your book. Thank you always for the education you have provided to your readers and your commitment to helping us learn.

Kind regards,

Patrick

Patrick,

Thank you for your kind words. My responses:

1. When share price is @ the 20-day EMA, it is still eligible regarding that specific parameter but let’s us know that it is near a possible red flag. This may lead us to consider ITM calls or deeper OTM puts should we select that security.

2. A stochastic oscillator reading > 80 is not a sell signal although it is termed “overbought” (in my opinion). I have seen stocks remain above 80 for months and we are undertaking weekly or monthly obligations. Now, if the oscillator dips below 80, we regard that as a mild bearish signal and if it double-dips below 80 we have a strong bear signal. The stochastic oscillator is important but only 1 of many parameters used in the BCI screening methodology.

3. Every month for more than 2 decades, my portfolios have stocks with mixed technicals. In bull or even normal market conditions I may still favor bullish positions for these stocks. In weaker conditions, I will take more defensive positions with mixed technical securities. In our weekly stock reports, consider all securities in the white cells that have adequate open interest.

Alan

Thank you Alan for always taking the time to respond and help clarify points and questions. Have a great week!

Premium members:

The BCI team has added another Blue Hour webinar to your member site:

“Examining a 7-Month Covered Call Trade Turning a 4.9% Loss into a 3.2% Gain”

Enjoy.

Alan

Alan,

I want to write a 10/9 put or two on BABA that premarket is at $289.60. Here’s my dilemma: Should I write a 280 and receive $1.91 premium with a delta of -0.209 or write 2 options at 272.5 with a premium of $1.00 with a delta of -0.129?

Cash in my account to cover is not an issue. Since I’m a relatively conservative investor, I was going to opt for the $1.00 premium.

Is there some calculation that can help with this decision?

Thanks,

Rudy

Rudy,

Use the BCI Put-Selling Calculator to determine initial time-value returns, annualized returns and percent discount should the put be exercised as shown in the screenshot below.

There is a free single-column version of this calculator located in the “Free Resources” link in the black bar at the top of our web pages.

The expanded 5-column version of the calculator can be purchased here:

https://thebluecollarinvestor.com/minimembership/elite-put-selling-calculator-2/

Our best calculator for both covered call writing and selling cash-secured puts can be found here:

https://thebluecollarinvestor.com/minimembership/calculator-elite-plus-calculator/

Our decisions are based on our strategy time-value return goals and personal risk-tolerance.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Alan

Good afternoon Alan!

Today is a very exciting day for me! I just executed my first mid contract unwind! The second ITM option I sold gave me an additional 2%! Very cool 😊.

Thank you for all your help!

-Nathan

Nathan,

Congratulations. I still get that same reaction after 20+ years of “hitting doubles”

You made my day.

Alan

Hi Alan,

Is there is a risk that call option be exercised because of ex-dividend date even if option is still OTM?

I have T 29 call expiring 10/16, the stock trades at $28.95 and 29 10/16 call is priced at $0.19. Ex-dividend date is 10/08 and dividend is $0.52.

I was assigned once in the past and as short position was created the amount of dividend was deducted from my account.

Regards,

Sunny

Forgot to mention that I’m talking about PMCC, not a regular covered call trade.

Sunny,

Whether we are using traditional covered call writing or the “Poor Man’s Covered Call”, there is always a slight chance of early exercise even for OTM calls.

Early exercise is extremely rare for ITM strikes and even more uncommon for OTM strikes, but possible.

The highest risk is when the call is ITM, the ex-date is near the contract expiration and the time-value remaining on the option is less than the dividend to be distributed.

It almost never makes financial sense for an option holder to exercise for a dividend but many retail investors are unaware of this.

Bottom line: Early exercise due to an ex-date is extremely rare and usually due to investor error that lands in our account.

Alan

Thanks, Alan. Everytime I go through ex-dividend dates I got confused, especially when trying to trade PMCC on high yielding stocks.

In my previous question to you regarding short call and LEAPS values after ex-dividend date you wrote that ex-dividend is already priced in options price months before ex-dividend date occurs. What I fail to understand is the dynamics of LEAPS price after ex-dividend date. T LEAPS basically has no time value. With T trading at $28.70 Jan 21 20 Call midpoint is $8.75, so time value is only $0.05. On 10/08 T will open roughly $0.50 lower because of ex-dividend. But if LEAPS has ex-dividend already priced in it must stay at the same price of $8.75, that means $0.50 will be added to time value. Is this correct? My concern is that I don’t know if I can hold T LEAPS through ex-dividend date. My logic says that I must sell LEAPS now and buy it back after ex-dividend date because it will be priced lower. If I’ll keep it through ex-dividend date I will incur loss on LEAPS side.

Sunny,

The price of the short call has the ex-date already factored in. Holders of LEAPS do not receive the dividend and share price does drop by $0.50 on the ex-date. We also have a long-term commitment to this trade. So, do we close the long LEAPS position because of this? No.

We enter a PMCC trade with the understanding that there are pros and cons to this strategy. Not receiving dividends is one of the cons. If we closed the long LEAPS, we would also have to close the short call to avoid a naked options position which our broker would, most likely, not allow anyway. We plan to hold the LEAPS for 1 – 2 years so closing the entire trade 4 times per year is not a practical application of the strategy. The $0.50 4 times per year pales in comparison to the decreased cost-basis enjoyed by using LEAPS instead of the stock.

Alan

Hi Alan,

I’ve been trading options for about 5 years. On your video (https://www.youtube.com/watch?v=BN9ywexV2Po&_=2) specifically the time frame of 2:15-2:36, where you talk about the compounding effect over time, it is ironic because I am doing the same thing, but using LEAPS about 2 years out and deep in the money.

I initially bought 8 leaps at .80 delta, but now they are closer to .90 because of stock appreciation. By using leaps I have about 3x the leverage. For this “experiment”, I am only using a broad market ETF. I am about 4 months in at this point, but have been able to purchase 2 additional LEAPS from the income sold on the weekly calls, for a total of 10 LEAPS now. I believe the exponential compounding effect will be like a snowball rolling down a mountain after a few years.

I do not plan on taking any money out of this account for at least 8 years. This way I will be able to truly gauge the returns. I am in uncharted waters a little here because I will eventually need to roll the current LEAPS further out. I made a point to wait at least 1 year from the purchase date to avoid short-term capital gains. However, I think it will be interesting as I roll the LEAPS that could be .90+ delta 1-2 years further out to a .80 delta again, even taking extrinsic value into effect that I could turn 1 LEAP into potentially 1.2 LEAPS, further compounding my LEAP positions.

Do you have any input on this strategy?

Thanks,

Jason

Jason,

I agree. The power of compounding is amazing.

The strategy you are using is the “Poor Man’s Covered Call (PMCC)” or long call diagonal debit spread. It is a large part of our latest book, “Covered call Writing Alternative Strategies”

We must first make sure that the initial structuring of our trade meets are formula requirement:

Difference between the strikes + 1st short call premium > cost of the LEAPS.

From there, the short call is the main management leg of the trade which is just as critical with this PMCC strategy as it is with traditional covered call writing.

Your Delta decisions are spot on as is your concern for rolling the LEAPS. I suggest rolling the LEAPS 90 days prior to contract expiration and anticipate a cost of $2.00 – $3.00 per share. All this information is detailed in our book and online video program:

BOOK:

https://thebluecollarinvestor.com/minimembership/covered-call-writing-alernative-strategies/

Online video:

https://thebluecollarinvestor.com/minimembership/video-poor-man-covered-call-program/

PMCC Calculator:

https://thebluecollarinvestor.com/minimembership/poor-mans-covered-call-calculator/

Alan

Premium members:

This week’s 4-page report of top-performing ETFs and analysis of the top-3 performing Select Sector SPDRs has been uploaded to your premium site. One and three-month analysis are included in the report. Weekly option and implied volatility stats are also incorporated.

The mid-week market tone is located on page 1 of the report.

For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

BCI Community:

I was asked to be one of the keynote speakers to kick off the Wealth365 Summit this Monday October 12th.

I am pleased to announce that I will be hosting 2 unique webinars that first day of the event, 10 AM ET and 7 PM ET.

Barry will be responding to your written question while I’m presenting.

Here is the link to reserve your free pass to this event:

https://summit.wealth365.com/alan-ellman/

Alan

Hi Alan,

I hope you doing well!

Thank you for your youtube videos, I really appreciate the informations you provided.

I have one question about selling covered call, lets say i’m just interested in the next day trade, only next day, and I wanna buy 100 shares of stock X and same time sell one covered call option before the market close, so scenario #1 the stock go up 2% in the next day I close all my positions and exit with profit, scenario #2 the stock fall 2% I close all my positions and exited with more softer lost. For this type of strategy which strike and expiration date is best for my situation?

Many thanks!

Kind regards,

Ahmed

Ahmed,

A 1-day covered call trade does not align with our BCI methodology. That said, strike selection in all covered call trades is based on our initial time-value return goal range and expiration date should be short-term in your strategy as this will allow for greatest benefit from Theta or time-value erosion.

I would strongly encourage paper-trading before embracing this approach.

Alan

Alan,

I just wanted to follow up regarding this article. Could you please let me know how we can proceed along with price.

Cheers

Nancy

Nancy,

If we decided to retain AGN for the next contract month and we rolled-out-and-up to the $125.00 strike, we enter a BTC limit order for $0.80 (20% guideline) and manage from there.

Alan