“Selling cash-secured puts is the exact same strategy as covered call writing”. We hear that over and over…except that it’s not. These two strategies have the same risk/reward profiles and that is why the claim is made so frequently. On page 214 of my book, Selling Cash-Secured Puts, I highlight a comparison chart showing similarities and differences between the two strategies. In this article, I will add another distinction as it relates to position management in a bear market environment and specifically when our underlying security is declining in value. A declining stock is not our friend whether we are selling calls or puts.

How to we manage a declining underlying security?

All exit strategies start the same way…we buy back the option. In covered call writing, we have a series of “next-steps” based on several parameters including overall market assessment, chart technicals and time frame within a contract. All details are spelled out in my books and DVDs. When selling puts and our 3% guideline is reached, we generally use the cash freed up by closing the original short position to secure another put on a better-performing underlying. It’s the cost to close our short positions that will underscore another contrast between the two strategies.

Delta and option premiums

Delta is the amount an option premium value will change when share price moves up or down by $1.00. It is the likelihood a strike price will end up in-the-money by expiration. Since the moneyness of calls and puts are inversely related, option premiums take different roads when share prices declines…call value moves down while put value accelerates. therefore, the cost to close a short position will be greater for puts than for calls.

Real-life example

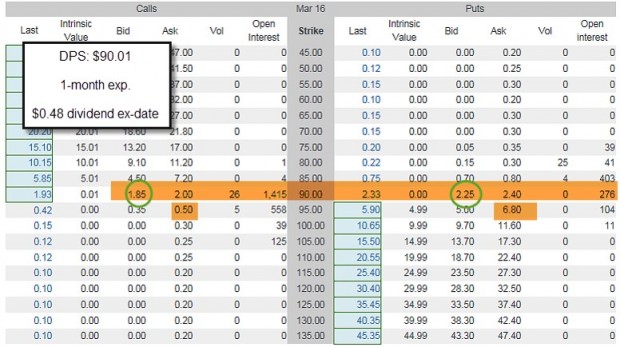

On 2/19/2016, Dr. Pepper Snapple Group (DPS) was trading at $90.01, right at a strike price and perfect for our analysis. Here is a screenshot of the options chain highlighting the $90.00 and $95.00 strikes for the March 18, 2016 1-month expirations:

DPS Options Chain On 2/19/2016

This is also a great learning tool because there is an ex-dividend date projected prior to contract expiration. This will reduce the call value and increase the put value but the call seller (share owner) will capture the $0.48 dividend. Without the ex-date, the two premiums are expected to be quite close. The call seller will generate the bid premium of $1.85 plus the dividend of $0.48 for a total credit of $2.33. The put-seller generates a bid premium of $2.25. The initial returns on both calculate to a 2.6% 1-month, initial return.

What if share price declines $5.00 to $85.00?

The $90.00 call strike moves deep out-of-the-money causing option value to decline. The current $95.00 call strike ($5.00 out-of-the-money) shows an “ask” premium of $0.50, much lower than the premium generated from the original call sale. As share value declines the cost to buy back the call option becomes less expensive. Of course, we must keep an eye on the debit created by share devaluation.

The $90.00 put strike moves deep in-the-money causing the premium value to accelerate substantially. The current $95.00 put strike ($5.00 in-the-money) shows an “ask” premium of $6.80, much higher than the premium generated from the original put sale. As share price declines, the cost to buy back the put option gets more expensive.

Closing our positions when share price is $85.00 for covered call writing

Let’s assume the “ask” prices are in play when we close. We have a share loss of $5.01 and an option and dividend credit of $2.33 ($1.85 + $0.48). This nets to a debit of $3.17 on a cost basis of $90.01 = a loss of 3.5%. This assumes no position management along the way, something that would never happen to us…right?

Closing our positions when share price is $85.00 for put-selling

We have an option debit of $4.55 ($6.80 – $2.25) on a cost basis of $87.75 ($90.00 – $2.25) = 5.2%, almost 50% worse than the covered call writing scenario (share value decline should also be factored in). This assumes no position management along the way, something that would never happen to us…right?

Discussion

In bear markets, we must be aware of the fact that the cost to buy back a put option on a declining stock will be more expensive than closing a short call. This does not eliminate put-selling from our arsenal in bear markets but does highlight the need to use deeper out-of-the-money puts for downside protection. In addition, we must be diligent about employing our 3% guideline and not allow share value to decline to the extent discussed in this article. In this scenario, we would have closed our short put when share value reached $87.30, cutting our losses approximately in half. We also must have a higher cash reserve to buy back options when share value decreases after selling puts.

Blue Hour webinar coming soon: No rate hike for current premium members

On July 28th at 9 PM ET we will be presenting our first Blue Hour webinar, free to Premium Members. My team is working hard to create a landing page to sign up and the first 50 premium members will have access to the live presentation. This webinar will be recorded and available to all Premium Members for free on the member page. The Blue Hour webinars will also be available for sale in the Blue Collar store. We plan to present at least six presentations per calendar year and they will include live Q&A, expert guest speakers, Barry Bergman, the BCI Director of Research and me. An email will be sent to Premium members once the web pages are ready for registration. There will be a member fee increase of $10 per month for all those who join after September 1st. Current members and those who sign up prior to September 1st will be grandfathered into the current low rates as long as membership remains uninterrupted.

Next live event- Workshop

July 16, 2016

American Association of Individual Investors

Washington DC Chapter

Northern Virginia Community College

9 AM – 12:30 PM

Seminar information and registration link

Market tone

I am devoting this week’s market tone segment entirely to Brexit.

On Thursday the United Kingdom voted to leave the European Union (EU). The UK is the world’s fifth largest economy representing 3% of the world’s economy. This decision was unexpected by most experts. The vote itself is not a binding decision and the full impact may not be clear for a few years. The results will be incorporated into an Act of Parliament in the UK which will be passed on to the EU. This will take place in a few months which is why Prime Minister Cameron has announced that he will resign in October so a new prime minister can take the lead from there. This will then start a two-year process of negotiating the UK exit from the EU. Suffice it to say that the period of uncertainty will last longer than a few days or even weeks or months.

Much of the concern relates to the favorable trade agreements the UK currently has with the EU which will change in context, the UK’s sovereign credit rating being downgraded and how changes in UK’s immigration policy will impact the job market in the EU…nobody knows for sure. Despite all the experts weighing in (and I don’t consider myself an expert in this area), as always, half will be right and half will be wrong. Remember, these are the same folks who predicted a “stay vote”

There is also concern of a domino effect with other countries currently in the EU expressing similar dissatisfaction with the globalization of their economies and politics.

When markets have days like we had on Friday or huge up days after unexpected positive news, we know from past history that the “real stock market” lies somewhere in between the two. So from all the ugliness that we experienced on Friday were there any positives to be gleaned?

To start, the central banks made it clear that they would work together to suppress volatility and provide liquidity to the financial institutions. A rate cut by the Bank of England in July is more likely and a rate increase by the US Federal Reserve has now become extremely unlikely for this calendar year. Friday’s market action was surely nothing to smile about but it could have been a lot worse and perhaps certain buying opportunities were created. Even in bearish and volatile markets there are always best-performers and it is our job to find them. For example, from our latest Premium Member ETF Report dated 6/22/2016, here are five exchange-traded funds results from yesterday’s market decline:

- GDX: +5.91%

- GDXJ: +4.98%

- XLU: +0.56%

- SLV: +2.43%

- TLT: +2.68%

From there, how we enter our positions can be crafted to an uncertain market environment (using in-the-money calls, out-of-the-money puts, low-implied volatility ETFs, low-beta stocks to name a few approaches). Not all investors are comfortable trading in volatile and uncertain markets and only you can make that decision but if we do, let’s do it smart, non-emotional and base our decisions on sound fundamental, technical and common sense principles. Many corporations are run by brilliant and experienced board members who seem to find ways to readjust and flourish even in challenging environments. My expectation is that Brexit will not be an exception to this observation…just one man’s opinion.

For the week, the S&P 500 declined by 1.64% for a year-to-date return of (-)0.32%.

Summary

IBD: Uptrend under pressure

GMI: 5/6- Buy signal since market close of May 25th (published prior to Brexit vote)

BCI: Not entering new positions or investing unused cash until the dust settles from the Brexit vote. Any new positions taken will be defensive in nature.

WHAT THE BROAD MARKET INDICATORS (S&P 500 AND VIX) ARE TELLING US

I love the videos so far. Two basic question though

1) what kinda strategy is this — bullish, bearish or neutral??

2) Also I watched the video “Ask Alan #23: Hitting a Double”. I got confused about what kinda strategy this was. This is where you sold a contract on VAL at 4.10 then BTC @ .85 when the price dipped? Then repeat the process @3.10. This why I wasn’t sure about this being a bullish strategy? Can you go into a more depth

Thanks

Ravi

Ravi,

1- Covered call writing can be crafted to be successful in all three market conditions. This is accomplished by the type of underlying security and option we select. For example, in a bullish market we would lean to stocks with higher implied volatility and out-of-the-money call options.

2- “Hitting a double” is a bullish exit strategy used in the first half of a contract. We also have an arsenal of exit strategies that reflect whether we are in a bullish or bearish environment. Being selective as to which stocks and options we choose and mastering the skill of position management is what allows us to become elite covered call writers and achieve the highest levels of returns.

Alan

Hi Alan,

Once again this technically challenged 72 year old has a question. I have the Ellman calculator all installed. Is the Unwind tab on that or a separate download?

The calculator is GREAT,

sorry to be a bother again,

thanks for your patience !!

John

John,

Glad to help.

The “Unwind Now” tab is located in the Elite version of the Ellman Calculator NOT in the Basic Ellman Calculator. As a premium member, you get a free copy of the Elite Calculator by logging into the premium site and scrolling down on the right side (“resources/downloads” section) to “E”. There you will find the Elite Calculator and its user guide.

The location of the “What Now” tab is shown in the screenshot below.

CLICK ON IMAGE TO ENLARGE & USE THE BACK ARROW TO RETURN TO BLOG.

Alan

Premium Members:

This week’s Weekly Stock Screen and Watch List has been uploaded to The Blue Collar Investor Premium Member site and is available for download in the “Reports” section. Look for the report dated 06/24/16.

Also, be sure to check out the latest BCI Training Videos and “Ask Alan” segments. You can view them at The Blue Collar YouTube Channel. For your convenience, the link to the BCI YouTube Channel is:

http://www.youtube.com/user/BlueCollarInvestor

Best,

Barry and the BCI Team

Hey Alan,

Thanks for devoting recent ink to Brexit. Those events don’t come along every day.

Please let us know when you feel the dust has settled enough to re-open shop. And why….

I’ll be looking for the following:

– S&P back above 50 day MA for at least two closed days with rising volume

– Oil holding above $45

– Fed signals rate hike delayed

– ECB easy money reaction to Brexit

– Friday’s job report

– Continued bearish slant in the financial press

I would much rather buy when the media is bearish than bullish. They are wrong more often than not.

Last week was a great example. These were sample headlines from Wednesday and Thursday

MarketWatch: Bollinger Bands Suggest Stocks Could Break Out in a Big Way

Wall Street Journal: U.S. Stocks Rally as Markets Bet on ‘Bremain’

Forbes: Stocks Rally with Brexit Looking Unlikely

MarketWatch: Stocks close higher as Wall Street bets U.K. Will Vote to Stay in EU

I would like my metrics above to happen accompanied by these headlines:

“Summer Gloom Just Around the Corner”

“Why the Market Can Only Go Down”

“Seasonality Turns Negative: Buyers Beware

“Gold and Bonds: Off to the Moon?”

Happy weekend! – Jay

Good Morning from hot and balmy south Louisiana !

I have read 3 of your books, purchased the DVD Series and was a premium member at one time. I took a break and am leaning hard to rejoining again. I was wondering if you could give some insight on one question pertaining to a strategy that myself and my “club” are using..

Using the Covered Call strategy, we have been purchasing the SLV ETF,(no earning reports to deal with) writing calls and using the premium to purchase more shares. Basically FREE shares, to build from 1000 to 2500 to 5000 to 10,000 shares . Once 10,000 shares is reached..CC’s @ .20 premium would bring in $2000/week…not a bad deal..

My question is this: Since we want to KEEP our shares, whats the best way to approach when SLV rises and we will most certainly get called away…this happened a few weeks ago..SLV shot up? What page in what book (or DVD section) covers this.

Thanks…I have learned so much from BCI…

Billy

Billy,

The sections of my books and DVDs that apply to your strategy are “Portfolio Overwriting” and “rollling options” Ex-dividend dates and earnings reports are not obstacles in your strategy.

Alan

Hi Jay,

I am waiting eagerly to see Alan’s respone to your post.

Uncertainty is gone, and I hope the market will settle one way or the other in a few days.

I noticed that the only bold ticker on this week’s list is SWHC, which rose more than 2% on Friday, ignoring Brexit.

Investors are betting on gun sales growth, on fears of new restrictions.

Roni

Hello Roni, happy Sunday!

The only sector winner Friday was XLU and, of course, TLT and GLD related ETF’s had a great day. We are now 2% below the 50 day MA on SPY and negative for the year. That always gets the attention of Technical Analysts.

SWHC is ironically often a great stock when the gun debate is in the spotlight. I have reached a separate peace with that debate. I don’t own guns and do not begrudge those who do. It just bugs me they are easier to get than a first time driver’s liscense :). – Jay

Happy Sunday to you too Jay

I have a small (22) pistol stashed away since 1966.

At the time I bought it, I needed some protection when spending weekends in a remote cabin.

It must be totally rusted and ruined by now, as I never looked at it since.

I am like you, and I’m not against people owning a gun, but I feel that an army rifle which shoots like a machine gun, and can kill hundreds of inocents, should not be easily accessible to civilians, and totally forbiden to dubious characters.

Well, Roni, I guess our positions on reasonable gun control put us on the NRA black list. They will be tapping our phones for fear we may incite a riot of sensibility.

But they are hell bent on making SWHC stock go up so let’s be smart and not fight it. And let’s not write calls against it until gun fever subsides.

Next mass shoting lets buy SWHC calls as soon as we get the news knowing the NRA will have our back. – Jay

Alan:

You advise selling cash covered puts at the bid price. I use the ask price as my guide since I’m selling. I figure since I’m selling, the ask price is what I’m asking for the put. I put in a limit order at the ask price or a price somewhere between the bid and ask. What am I missing?

Peter,

The market-makers profit is the bid-ask spread. If we sell at the “ask” (call or put), they make no money. That will not happen. So we sell at the “bid”, the lower price and buy at the “ask” the higher price. Now we can negotiate with these market makers when the spreads are not tight by placing limit order slightly away from the midpoint of the spread in favor of the market makers. This is discussed in detail in both versions of the Complete Encyclopedias.

Alan

Alan:

Thanks for your prompt reply. Now I know why the quoted ask price has to go up before I get a fill at the old ask price. I have been successful in getting the ask price, but not always. This practice does tend to increase my rate of return.

I’ve been trading covered calls and cash secured options for about seven years. Which of your books would recommend I read first?

Thanks again.

Peter

Peter,

Thanks for sharing your trading style.

The best book to get started:

https://www.thebluecollarinvestor.com/alan-ellmans-complete-encyclopedia-for-covered-call-writing-scover/

Alan

Premium Members,

The Premium Weekly Report has been revised and uploaded to the Premium Member site. Due to the current market situation, The Blue Collar Investor Team thought it would be prudent to provide this special update to the report that was published over the weekend. The revisions made are:

– Only the “Running List” (the second section) was revised

– The columns of the “Running List” that were rescanned are

highlighted in yellow

– The stocks that failed in this revision are the “shaded” rows in

the “Passed Previous Weeks & Failed Current Week” (pink)

section

Look for the report dated 06/27/16.

Best,

Barry and The Blue Collar Investor Team

Hi Alan,

Thanks for all the work here! I have read your books, watched your DVD’s and paper traded for several months. Despite the market right now I have been making 2-3% every month! Thank you!

Dustin

Dustin,

You made my day!

Alan

Alan,

I was at your Raleigh talk a few weeks ago. I purchased your 3rd book and I finished it last week. I’m now going back to re read the chapter on Exit Strategies. I’m planning on subscribing to your news letter this week and start paper trading. I’ve watched a number of your videos on your website. I’ve also searched the Itunes podcasts and listened to your interview on 52 Traders. I feel like I have a fairly good beginners understanding of what you are teaching and I now need to practice with paper trading.

I see that you also have DVD’s. Is there additional training in the DVD’s that is not in your 3rd book?

Is there anything else I should read, study, or watch before I start paper trading the BCI system?

If you ever decide to do a podcast please let us know. Also if you are interviewed on a podcast please let us know.

Thanks so much for sharing your knowledge and experience with me through your talk and book.

Thanks,

Nelson

Nelson,

You are approaching this in the perfect manner…education, paper trade and then go. To respond to your questions:

1- For covered call writing, consider Encyclopedia Volume 2

2- CCW DVD Program…similar to classic version of Encyclopedia + 3 45 minute Q&A sessions with audience that may approach peripheral issues.

3- Webinars and podcasts: I’ve done many over the years and post on the “Events” section of our website (blog page-top right) future events. Check the Options Industry Council (OIC) website where I’ve been interviewed and been part of panel discussions.

4- Make sure you receive our free weekly newsletter if you are not already…subscribe on our blog page right side.

5- On July 28th we are starting a “Blue Hour”, a series of 6 webinars per year, free to premium Members and at a minimal cost to non-members. Look for info on these to follow.

Alan

The newsletter said to wait until Brexit vote was over to start trading again. When are you going to resume?

Thanks

Jeff

Brexit: When to re-enter the market:

Since I posted that I was reserving 1/3 of my cash holdings on the sidelines until after the Brexit vote dozens of members have asked me when to re-enter the market, some posting on this blog. As always, I will never give specific financial recommendations because that will differ from investor to investor but I’m always happen to share my approach and what I’m currently doing.

Let’s start with stating the obvious… no one out there (despite the claims of some) can accurately time and predict the market short-term. That includes me. However, we can definitely throw the odds dramatically in our favor. That’s what the BCI methodology is all about. We do know that the market historically goes up long-term with many whipsaws along the way. That volatility is what gives options value.

I have taken no covered call positions this contract month and will probably not do so until the August contracts begin upon July expirations. However, I have been waiting for the market overreaction (my opinion) to subside before investing my cash on the sidelines. Thus far, today appears that the market has absorbed the shock of the surprise vote but we don’t know for sure. My plan is to dollar-cost-average into the broad market over the remaining days this week and will consider two approaches both using the SelectSector SPDR ETFs:

1- Dollar-cost-average into the top 3 performing SelectSector SPDRs until I am fully invested by Fridays market close.

2- Selling out-of-the-money cash secured puts leveraging the top 3 Select Sector SPDRs

This will accomplish:

1- Take advantage of anticipated market recovery

2- Allow for possible turbulence during the week by not investing all the available cash on the first positive day

3- Have 2 available plans, the first more aggressive than the second so decisions can be made based on personal risk tolerance

It is important to realize that not all investors are comfortable investing in this environment and personal decisions should factor this in. This is one of the reasons why I don’t give specific financial advice. However, this is my plan.

Alan

Alan,

Thank you for taking the time to post this characteristically well thought out answer to the Brexit re-entry question.

I am among your guilty friends who prodded you for it :).

It was an encouraging day reclaiming the 200 day MA on SPY. I would have liked to see more volume but it is summer and the “Swim at your own risk” signs are up at the beach :).

Layering back into positions makes all the sense in the world.

Thanks again for your timely update. – Jay

Premium members:

This week’s 8-page report of top-performing ETFs and analysis of ALL Select Sector Components has been uploaded to your premium site. The report also lists Top-performing ETFs with Weekly options as well as the implied volatility of all eligible candidates. For your convenience, here is the link to login to the premium site:

https://www.thebluecollarinvestor.com/member/login.php

NOT A PREMIUM MEMBER? Check out this link:

https://www.thebluecollarinvestor.com/membership.shtml

Alan and the BCI team

Alan,

Isn’t it interesting how swiftly the landscape changes?

Maybe more countries should leave the EU if it will produce a counter rally like this one :)!

Proof positive of your statement that none of us can predict the market in the short term. – Jay